- United States

- /

- Hospitality

- /

- NasdaqGS:BLMN

3 US Stocks Trading At An Estimated 16.4% To 35.6% Below Intrinsic Value

Reviewed by Simply Wall St

As the U.S. market continues to show resilience with major indices like the Dow Jones and S&P 500 on track for a winning month, investors are keenly observing how these trends impact stock valuations. In this environment, identifying undervalued stocks—those trading below their intrinsic value—can be a strategic move for those looking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Victory Capital Holdings (NasdaqGS:VCTR) | $72.03 | $142.32 | 49.4% |

| NBT Bancorp (NasdaqGS:NBTB) | $50.08 | $99.93 | 49.9% |

| UMB Financial (NasdaqGS:UMBF) | $126.05 | $243.22 | 48.2% |

| West Bancorporation (NasdaqGS:WTBA) | $23.99 | $46.83 | 48.8% |

| Five Star Bancorp (NasdaqGS:FSBC) | $33.16 | $63.88 | 48.1% |

| Symbotic (NasdaqGM:SYM) | $23.995 | $47.28 | 49.3% |

| Privia Health Group (NasdaqGS:PRVA) | $21.66 | $43.17 | 49.8% |

| South Atlantic Bancshares (OTCPK:SABK) | $15.50 | $30.26 | 48.8% |

| Intuitive Machines (NasdaqGM:LUNR) | $14.45 | $28.66 | 49.6% |

| Snap (NYSE:SNAP) | $11.61 | $22.76 | 49% |

Let's dive into some prime choices out of the screener.

Establishment Labs Holdings (NasdaqCM:ESTA)

Overview: Establishment Labs Holdings Inc. is a medical technology company that manufactures and markets medical devices for aesthetic and reconstructive plastic surgery, with a market cap of approximately $1.29 billion.

Operations: The company generates revenue primarily from its medical products segment, totaling $153.07 million.

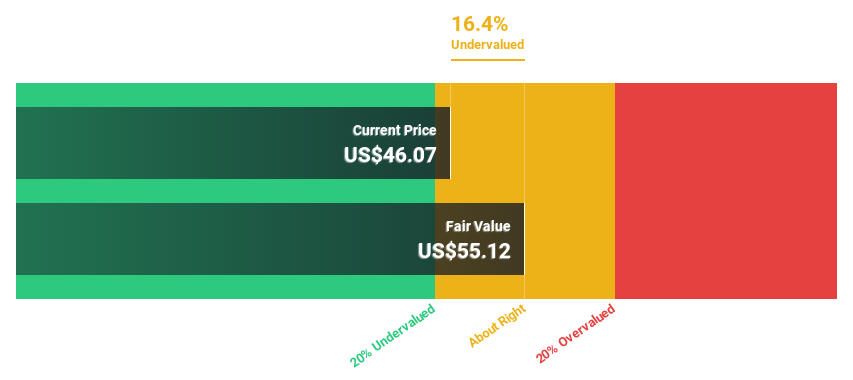

Estimated Discount To Fair Value: 16.4%

Establishment Labs Holdings shows potential as an undervalued stock based on cash flows, trading at US$46.07, 16.4% below its estimated fair value of US$55.12. Despite recent volatility and shareholder dilution, the company's revenue is projected to grow significantly faster than the market at 23.6% annually, with earnings expected to rise sharply by over 49% per year. Recent FDA approval for innovative Motiva Implants could enhance future cash flow prospects despite current unprofitability forecasts over three years.

- Insights from our recent growth report point to a promising forecast for Establishment Labs Holdings' business outlook.

- Dive into the specifics of Establishment Labs Holdings here with our thorough financial health report.

Bloomin' Brands (NasdaqGS:BLMN)

Overview: Bloomin' Brands, Inc. owns and operates a variety of dining restaurants ranging from casual to fine dining both in the United States and internationally, with a market cap of approximately $1.21 billion.

Operations: The company's revenue segments consist of $3.95 billion from the United States and $600.16 million from international operations.

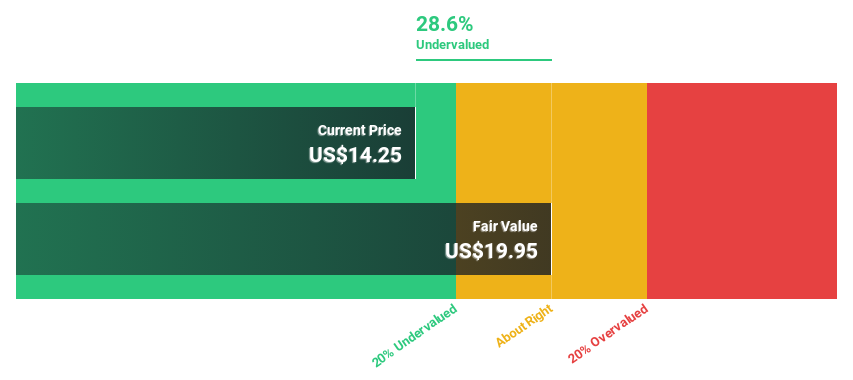

Estimated Discount To Fair Value: 28.6%

Bloomin' Brands is trading at US$14.25, more than 20% below its estimated fair value of US$19.95, indicating potential undervaluation based on cash flows. Despite high debt levels and a dividend not well covered by earnings or free cash flows, the company is expected to become profitable within three years with above-average market growth in profits. However, revenue is forecasted to decline by 2.7% annually over the same period.

- Upon reviewing our latest growth report, Bloomin' Brands' projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in Bloomin' Brands' balance sheet health report.

Curbline Properties (NYSE:CURB)

Overview: Curbline Properties Corp. is involved in owning, managing, leasing, acquiring, and developing a portfolio of convenience retail properties in the United States with a market cap of approximately $2.57 billion.

Operations: The company generates revenue of $111.43 million from its operations in convenience retail properties across the United States.

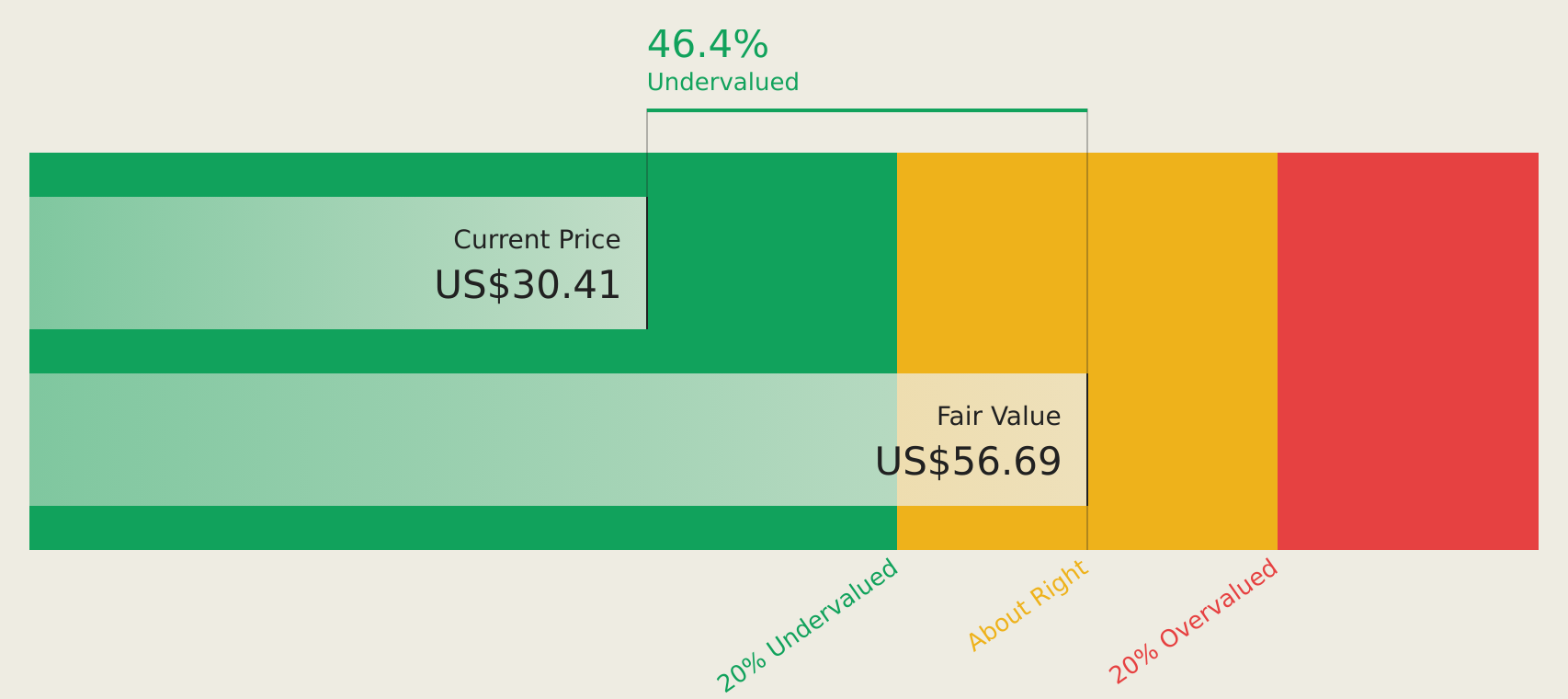

Estimated Discount To Fair Value: 35.6%

Curbline Properties, trading at US$24.43, is significantly undervalued compared to its estimated fair value of US$37.92. Despite a recent drop in profit margins from 33.5% to 5.8%, the company shows strong potential with revenue expected to grow annually by 23.7%, outpacing the market average of 8.9%. However, it faces challenges as it's forecasted to remain unprofitable for the next three years despite high earnings growth projections.

- Our earnings growth report unveils the potential for significant increases in Curbline Properties' future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Curbline Properties.

Seize The Opportunity

- Gain an insight into the universe of 187 Undervalued US Stocks Based On Cash Flows by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bloomin' Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BLMN

Bloomin' Brands

Bloomin’ Brands, Inc., through its subsidiaries, owns and operates casual, upscale casual, and fine dining restaurants in the United States and internationally.

Undervalued with reasonable growth potential.