Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:BKNG

A Look at Booking Holdings (BKNG) Valuation Following Strong Q3 Earnings, Upbeat Guidance, and Wedbush Upgrade

Simply Wall St

Reviewed by Simply Wall St

Booking Holdings (BKNG) delivered third-quarter earnings that topped expectations, supported by its Connected Trip strategy, expanding loyalty programs, and AI features. The company also raised its revenue and profit guidance for the rest of the year.

See our latest analysis for Booking Holdings.

After a year marked by ambitious tech rollouts and upbeat financials, Booking Holdings’ share price sits at $4,914.69. While the 1-year total shareholder return is down 4.8%, longer-term investors have still seen outstanding gains. A 139% total return over three years highlights the company’s growth runway and resilient business model. Recent news, such as its Wedbush upgrade and continued momentum in loyalty and AI initiatives, indicates that investors are considering both near-term volatility and the company’s ability to build lasting value.

If Booking’s evolving digital strategy has you watching the travel sector, this could be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With Booking Holdings delivering strong results and offering impressive guidance for the year ahead, investors are left to wonder whether the current share price still reflects untapped value or if future growth is now fully priced in.

Most Popular Narrative: 20.8% Undervalued

Market watchers are taking note as the most widely followed narrative values Booking Holdings at $6,207 per share. This stands well above the last close at $4,914.69 and suggests there may be meaningful upside if the key drivers of future growth play out as expected.

The company’s focus on increasing alternative accommodations and expanding its Genius loyalty program aims to strengthen customer retention and capture a broader market, potentially boosting revenue and net margins. Initiatives like the Connected Trip vision and strategic partnerships (for example, with Uber and AI organizations) are designed to offer enhanced, integrated travel experiences, likely leading to increased customer engagement and higher earnings growth.

Want to know what powers this bullish fair value? This narrative leans on blockbuster profit projections, margin lift, and a daring growth outlook. Discover which forecasts sparked this high target and the numbers that could surprise even seasoned investors.

Result: Fair Value of $6,207 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifting travel behaviors and increased competition from AI-driven platforms remain real risks that could test the strength of Booking Holdings' growth story.

Find out about the key risks to this Booking Holdings narrative.

Another View: A Multiples-Based Perspective

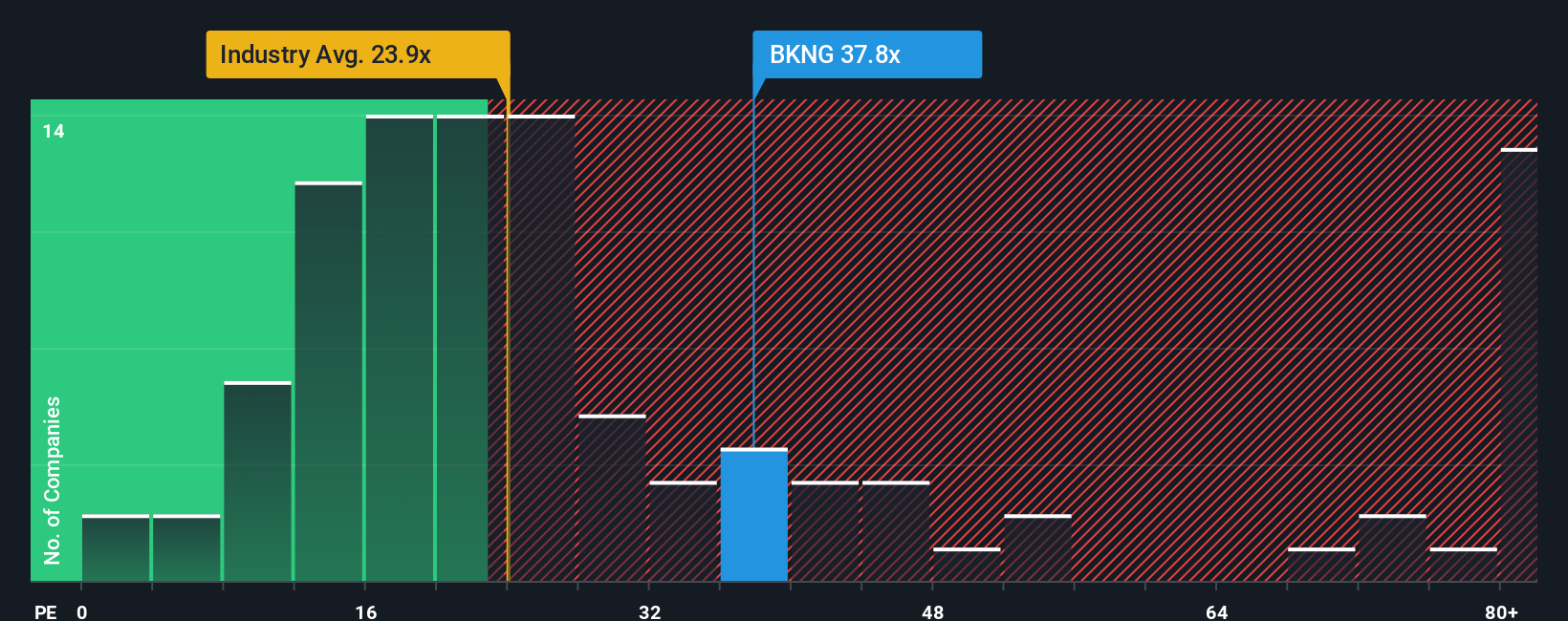

While the fair value narrative points to significant upside, a look at Booking Holdings' price-to-earnings ratio tells a more cautious story. The current ratio sits at 31.4x, noticeably higher than both peer average at 29x and the US Hospitality industry’s 21.4x. However, it remains below the fair ratio of 37.1x. This suggests the stock commands a premium, possibly reflecting optimism around its future growth, but it could also signal valuation risk if expectations are not met.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Booking Holdings Narrative

If you have your own take on Booking Holdings or want to dig into the data yourself, it only takes a few minutes to analyze and tell your own story. Do it your way

A great starting point for your Booking Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Take your investing game to the next level with hand-picked opportunities that balance high reward potential and smart diversification. Your portfolio deserves a fresh look at what’s working right now. Don’t miss out on these targeted ideas:

- Unlock growth potential by checking out these 25 AI penny stocks, harnessing artificial intelligence to change the way businesses compete and innovate across industries.

- Find strong income opportunities with these 15 dividend stocks with yields > 3%, offering robust yields to help secure your cash flow in any market environment.

- Stay ahead of tomorrow’s breakthroughs and browse these 28 quantum computing stocks, driving innovation with cutting-edge advances in computing power and technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Booking Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BKNG

Booking Holdings

Provides online and traditional travel and restaurant reservations and related services in the United States, the Netherlands, and internationally.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative