Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:WMT

Walmart (WMT) Valuation: Assessing Shares After Strong Q3 Results and Raised Full-Year Outlook

Simply Wall St

Reviewed by Simply Wall St

Walmart (WMT) shares gained momentum after the company delivered better-than-expected third-quarter results and boosted its full-year sales and operating income outlook. Management’s optimism, along with strong e-commerce and advertising growth, fueled the stock’s recent climb.

See our latest analysis for Walmart.

Momentum is clearly building for Walmart. After upbeat Q3 results and an improved outlook, the company’s share price has rallied sharply, up 8.4% over the past week and now sitting at $109.10. Looking at the bigger picture, Walmart’s one-year total shareholder return of nearly 20% and a robust 133% total return over five years show that recent gains are part of a steady upward trend, with investors responding to sustained growth in new business lines and continued operational strength.

If Walmart’s latest surge has you wondering what else is outperforming, now’s a perfect time to broaden your view and discover fast growing stocks with high insider ownership

But after such a swift run-up and higher expectations, is Walmart’s stock still trading at an attractive valuation, or has the market already priced in all of the company’s future growth prospects? This raises the question of whether there is still a real buying opportunity here.

Most Popular Narrative: 4.1% Undervalued

Walmart’s most widely watched narrative points to a current stock price just below its fair value estimate, signaling a small margin of opportunity for investors. The battleground for this view is where digital transformation and margin expansion intersect, underpinning the retailer's future profit mix.

Expansion of high-margin business streams such as Walmart Connect (advertising, up 31-46% globally), marketplace, and Walmart+ memberships (global advertising up 46%, membership income up 15%) is diversifying Walmart's income base beyond retail. This is gradually transforming the company's profit mix and has resulted in structurally higher net margins and earnings over time.

Curious what’s driving up the narrative’s fair value? The story is built on unconventional growth levers, boosted profit assumptions, and a bold bet that Walmart’s margins will look very different. Want to see the secrets behind these bullish projections? Explore the numbers and discover what underpins this calculated optimism in the full narrative.

Result: Fair Value of $113.78 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent cost pressures and ongoing international challenges could quickly undermine Walmart’s recent margin gains and force a rethink of bullish forecasts.

Find out about the key risks to this Walmart narrative.

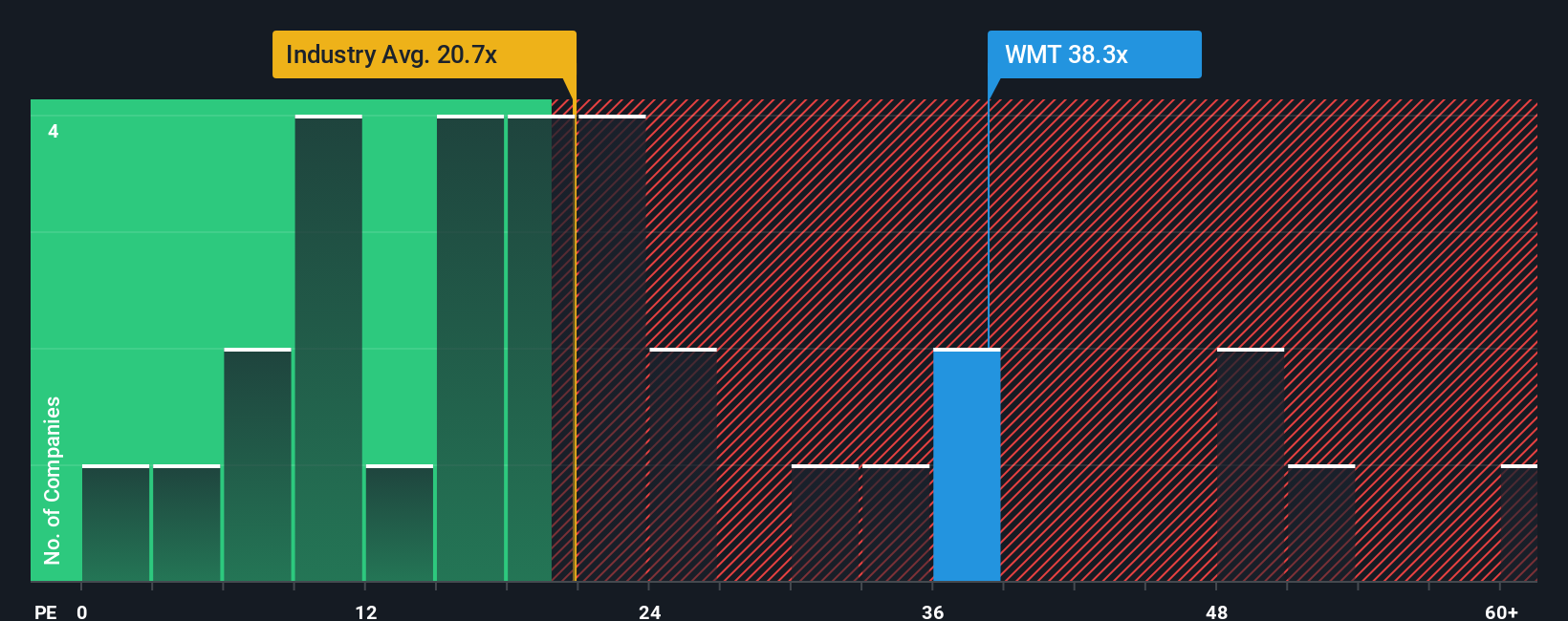

Another View: Multiples Suggest Full Pricing

Looking at things another way, Walmart’s shares trade at 38 times earnings. That is significantly higher than the Consumer Retailing industry average of 20.1 times, the peer average of 25.3 times, and the fair ratio of 34.4 times earnings. This gap could mean less upside if Walmart’s growth falls short, or present a valuation risk if market optimism fades. Does this premium reflect real advantages, or is it just optimism running ahead of fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Walmart Narrative

If you think a different story is unfolding or want to see what your own analysis reveals, why not put together your own perspective in just a few minutes? Do it your way

A great starting point for your Walmart research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Want to stay ahead of the market? Unlock new opportunities with our smart screeners and discover what you might be missing by only focusing on the most obvious choices.

- Start targeting tomorrow’s disruptors by tracking these 25 AI penny stocks that are changing everything from automation to analytics and setting the pace for the next wave of technology.

- Amplify your income strategy by checking out these 15 dividend stocks with yields > 3% with robust yields and a record of generating consistent cash returns for shareholders.

- Embrace bold possibilities by reviewing these 81 cryptocurrency and blockchain stocks capturing market attention with blockchain advancements and the growing adoption of digital currency.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Walmart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WMT

Walmart

Engages in the operation of retail and wholesale stores and clubs, eCommerce websites, and mobile applications worldwide.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative