Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:WHR

Is It Time to Take a Fresh Look at Whirlpool After Its Strategic Partnerships?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Whirlpool stock is a hidden gem or just another value trap? Let us break down whether now is the right time to take a closer look.

- After losing 31.6% year-to-date, Whirlpool has recently bounced back with a 7.3% gain in the last week and 5.6% over the last month. This has sparked fresh interest from investors debating its comeback potential.

- Recent headlines highlight that Whirlpool’s strategic divestments and partnerships have been drawing attention, as the company reshapes its business to adapt to market shifts. These moves have fueled speculation about long-term growth prospects and altered risk perceptions for shareholders.

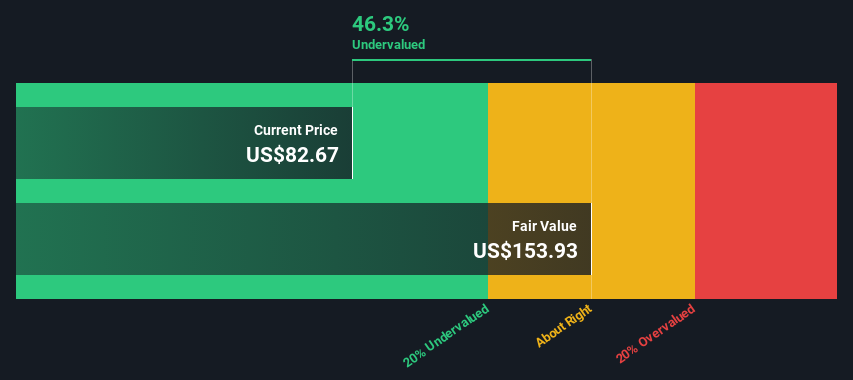

- On a fundamental level, Whirlpool scores a solid 5 out of 6 on our undervaluation checks, putting it ahead of many peers. Next, we will explore the classic approaches to valuing Whirlpool. Later, we will reveal a smarter way to judge whether the stock is truly undervalued.

Find out why Whirlpool's -24.9% return over the last year is lagging behind its peers.

Approach 1: Whirlpool Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future free cash flows and discounting them back to today's dollars. This approach gives investors a sense of what the business is really worth, based on its ability to generate cash over time.

Looking at Whirlpool, the most recent reported Free Cash Flow sits at negative $0.96 million. However, projections show rapid recovery and growth, reaching approximately $388 million in 2026 and rising to $821 million by 2035. Analysts provide estimates for up to five years, with further yearly growth extrapolated by Simply Wall St. All figures are in U.S. dollars.

Once these future cash flows are discounted to the present, Whirlpool's intrinsic value comes to $108.85 per share. Compared to the current share price, the DCF analysis suggests the stock is 27.7% undervalued. This may indicate potential opportunities if these forecasts are realized.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Whirlpool is undervalued by 27.7%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

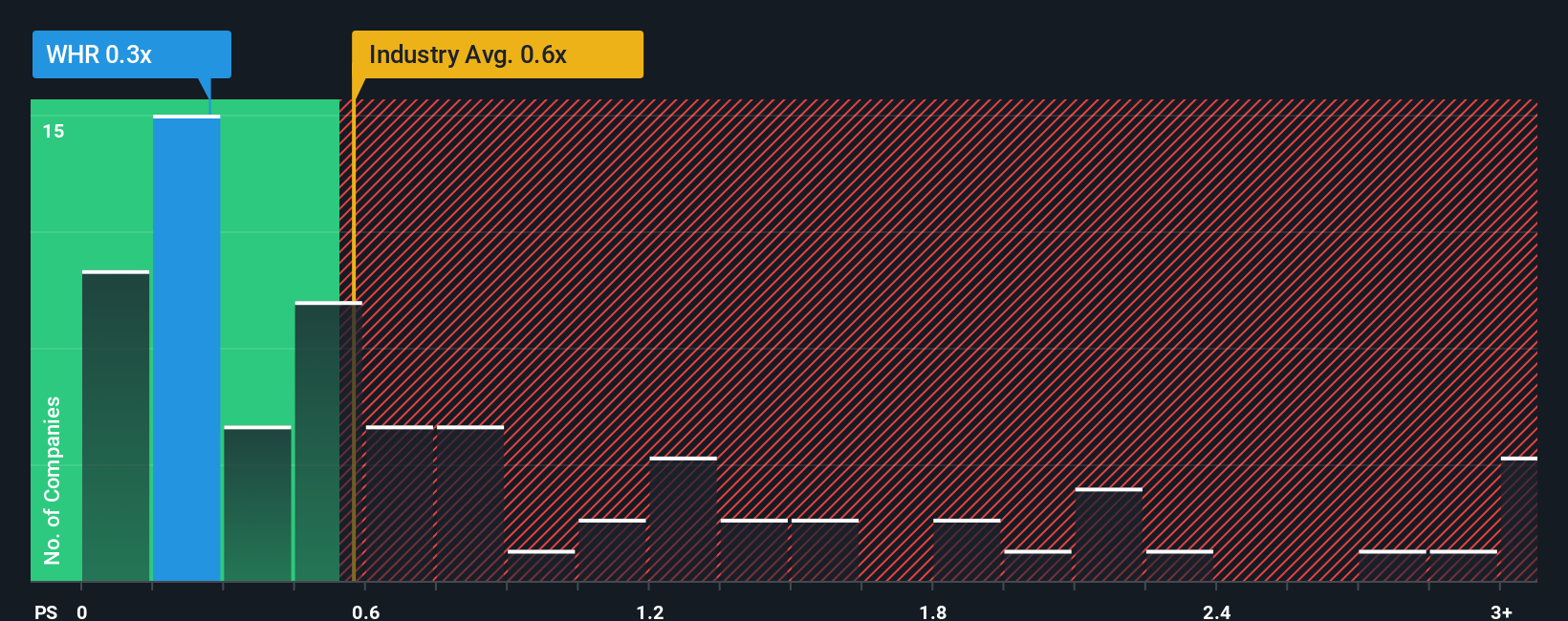

Approach 2: Whirlpool Price vs Sales (P/S) Ratio

The Price-to-Sales (P/S) ratio is a widely used valuation tool, especially useful for companies where earnings might be volatile or temporarily negative, but where revenue remains steady or predictable. For profitable companies like Whirlpool, the P/S multiple helps investors compare how much they are paying for each dollar of sales, providing a consistent benchmark regardless of short-term fluctuations in profitability.

Growth expectations and perceived risks play a significant role in determining what constitutes a “normal” or “fair” P/S ratio for any stock. Companies expected to grow revenue quickly or with lower risk typically trade at higher multiples, while those with slower growth prospects or more uncertainty tend to see lower ratios.

Currently, Whirlpool’s P/S ratio stands at just 0.28x. That figure is far below both the industry average of 0.65x and the peer group average of 1.06x, suggesting Whirlpool trades at a meaningful discount to other Consumer Durables companies. However, rather than just stopping there, Simply Wall St introduces the “Fair Ratio,” a proprietary metric that considers a company’s tangible growth expectations, profit margins, size, industry, and specific risks. For Whirlpool, this fair P/S multiple is calculated at 0.57x. Because the Fair Ratio incorporates factors that crude peer or industry averages miss, it provides a better guide to what the market should reasonably pay for the stock now and over time.

Compared to this Fair Ratio, Whirlpool’s actual P/S is still significantly lower, indicating that shares are likely undervalued based on where sales multiples should trade given its own fundamentals and risks.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Whirlpool Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives, a smart, user-driven approach that connects Whirlpool’s story to its projected financial outcomes and ultimately to a fair value per share.

A Narrative is your opportunity to tell the story behind the numbers, based on your own perspective of what will shape Whirlpool’s future, whether that is innovation, global expansion, or headwinds from competition and shifting demand. Instead of just plugging numbers into a formula, you lay out your expectations for revenue, margins, and key risks, tying them together to estimate what the company is truly worth.

On Simply Wall St, Narratives are an easy-to-use tool available within the Community page, where millions of investors share and compare their views on Whirlpool and other companies. Narratives help you decide when to buy or sell by linking your assumptions to a calculated Fair Value, and making it easy to see how this compares to the current market price.

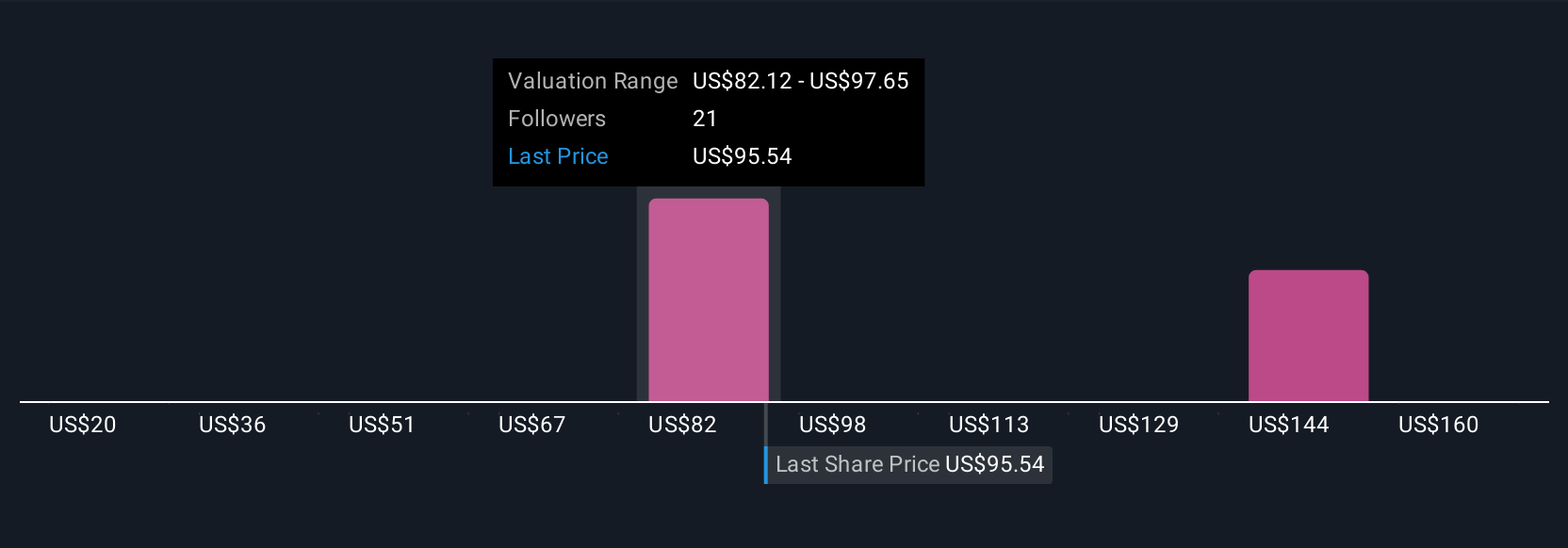

Best of all, Narratives update dynamically when news, financials, or new data arrive, ensuring your outlook remains relevant. For example, one investor might see Whirlpool’s future fair value at $145 based on a strong turnaround and successful innovation, while another sets it at just $63, focusing on persistent competition and slow demand recovery. This highlights the real-world variety of perspectives possible with this tool.

Do you think there's more to the story for Whirlpool? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Whirlpool might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WHR

Whirlpool

Manufactures and markets home appliances and related products and services in the North America, Latin America, Asia, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative