Advertisement

- United States

- /

- Leisure

- /

- NYSE:MODG

Does Topgolf Callaway Brands Still Offer Value After 27% Jump on New Partnerships?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have ever wondered whether Topgolf Callaway Brands is a bargain, overpriced, or somewhere in between, you are not alone. This article is for you.

- The stock has been on a tear lately, jumping 27.6% in the past week, 35.7% over the past month, and an eye-catching 53.3% in the last year. This has put growth potential front and center.

- Much of this momentum can be attributed to a wave of optimism after the company announced new strategic partnerships and high-profile product launches, which have energized investor confidence. Headlines about industry expansion and consumer engagement have added extra fuel to the rally.

- On our valuation checks, Topgolf Callaway Brands scores a solid 5 out of 6. This makes it an intriguing case for further analysis. Let’s break down the numbers, compare the usual methods, and share a perspective you may not have considered by the end of this article.

Approach 1: Topgolf Callaway Brands Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the intrinsic value of a company by forecasting its future cash flows and discounting them back to the present to account for time and risk. This method helps investors understand what the company is fundamentally worth today, given expectations about its performance over time.

For Topgolf Callaway Brands, the current Free Cash Flow stands at -68 Million $. The projections are striking, as analysts estimate free cash flow could rise to 342 Million $ by 2027 based on analyst data. Simply Wall St’s further extrapolated estimates reach nearly 2.7 Billion $ in 2035. These figures reflect expectations of substantial business growth, especially over the next decade.

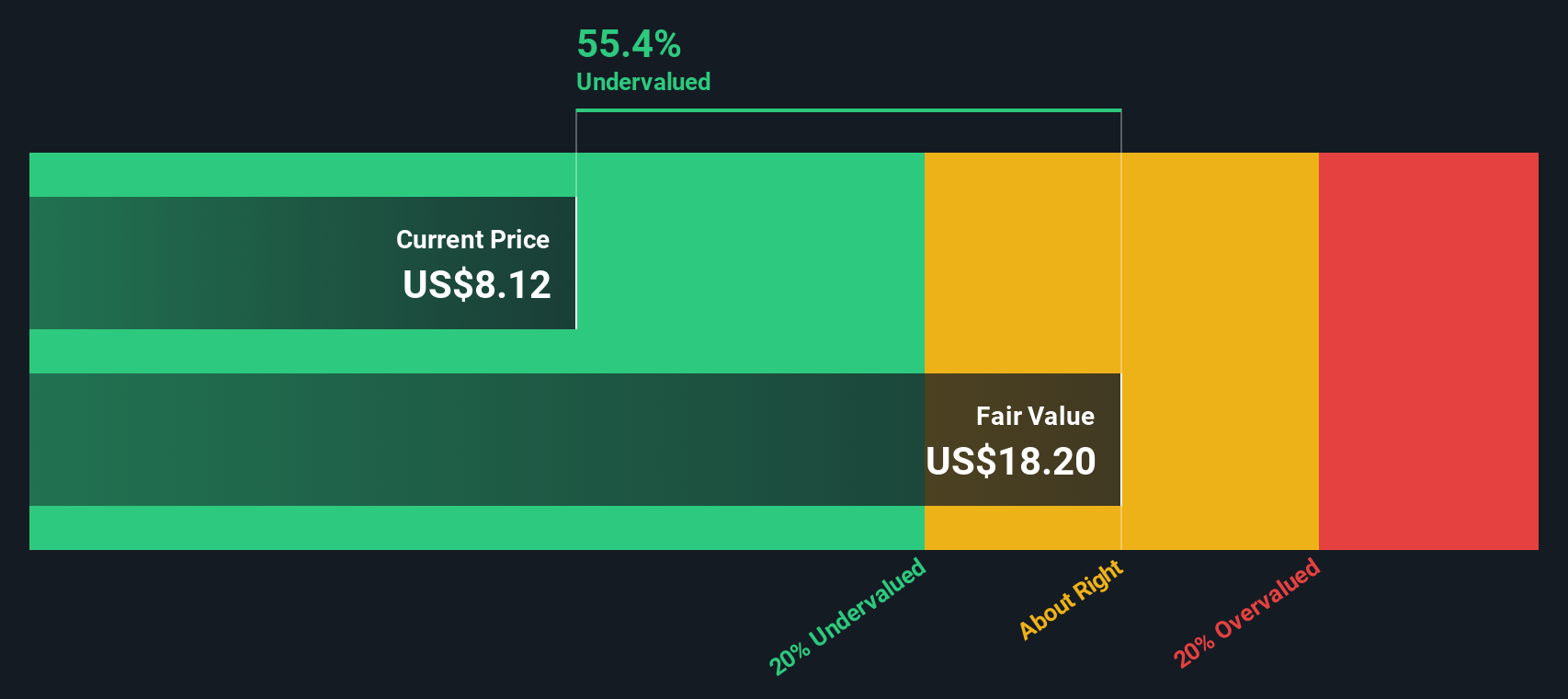

Using these forecasts in a 2 Stage Free Cash Flow to Equity DCF model, the estimated fair value for the company is 113.14 $ per share. This means the current share price is 88.6% below its estimated intrinsic value, which suggests the stock may be trading at a significant discount relative to projected value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Topgolf Callaway Brands is undervalued by 88.6%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Topgolf Callaway Brands Price vs Sales

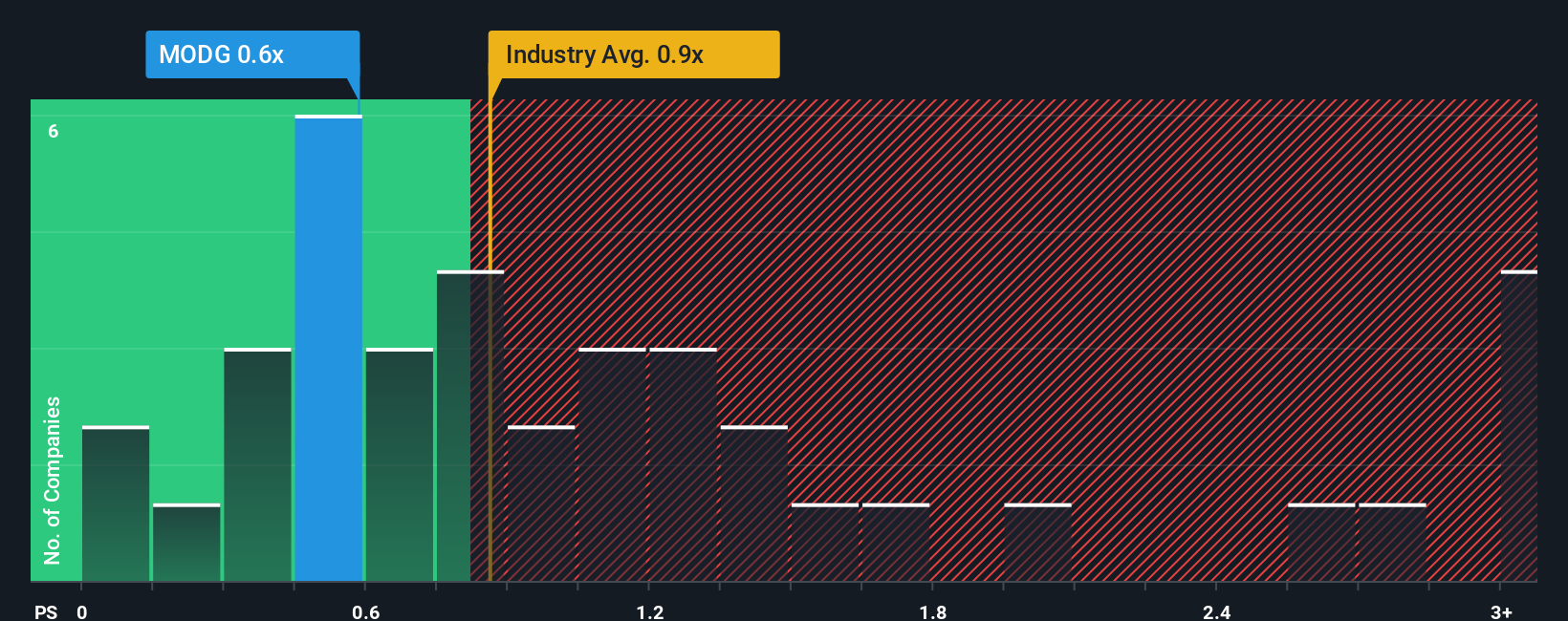

For companies where earnings may be volatile or not yet consistently positive, the Price-to-Sales (P/S) ratio is often the most useful valuation metric. This is particularly true for growth-focused companies like Topgolf Callaway Brands, as sales figures are generally more stable and harder to manipulate than earnings.

Generally, the higher the company’s growth prospects and the lower its risks, the higher a “normal” or “fair” P/S ratio is justified. Conversely, if future growth is unclear or the risk profile is heightened, investors usually pay a lower multiple for each dollar of sales.

Currently, Topgolf Callaway Brands trades at a P/S ratio of 0.58x. This is below the industry average for the Leisure sector, which sits at 0.86x, and well under the peer average of 1.35x. Simply Wall St’s proprietary Fair Ratio for the company is 0.63x, which takes into account not just sales and growth, but also factors like profit margins, risk, company size, and industry dynamics.

The Fair Ratio is a more rounded benchmark because, unlike simple peer or industry comparisons, it adjusts for the full financial and strategic context unique to Topgolf Callaway Brands. This makes it a more tailored tool for spotting potential mispricings.

Comparing the Fair Ratio (0.63x) to the actual P/S ratio (0.58x), Topgolf Callaway Brands appears undervalued on this basis. The discount suggests the market may not be fully appreciating its sales growth and overall positioning.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Topgolf Callaway Brands Narrative

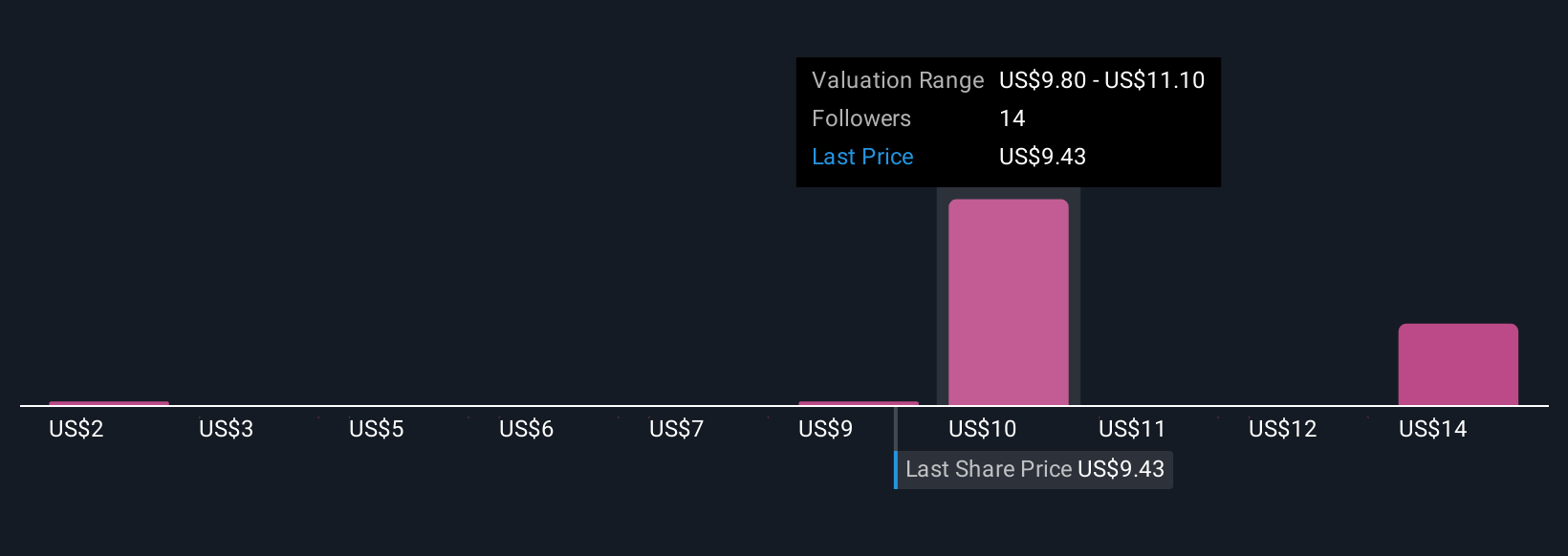

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a concise view of a company’s story. It combines your unique perspective with assumptions about future revenues, margins, and risks, tying them directly to a fair value estimate. Narratives link the “why” behind a stock’s numbers with a forward-looking forecast, adding critical context that raw data alone cannot provide.

On Simply Wall St’s Community page, Narratives are available to everyone, forming an easy-to-use tool trusted by millions of investors. Narratives allow you to visualize each user’s forecasts, compare fair values to share price in real time, and understand whether the stock is a buy or sell under different viewpoints. These are not static opinions. When new information, like news or results, is published, Narratives and their fair values update dynamically, so you are never left behind.

Take Topgolf Callaway Brands as an example: bullish investors see business simplification and global expansion boosting margins and setting a fair value as high as $13.00 per share, while bearish observers highlight ongoing risks and assign a fair value as low as $9.00. Narratives put these perspectives side by side, helping you track whose assumptions are playing out and which story you believe.

Do you think there's more to the story for Topgolf Callaway Brands? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Topgolf Callaway Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MODG

Topgolf Callaway Brands

Designs, manufactures, and sells golf equipment, golf and lifestyle apparel, and other accessories in the United States, Europe, Asia, and Internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative