Advertisement

- United States

- /

- Luxury

- /

- NYSE:DECK

Does Stifel’s Upgrade on Hoka’s Strength Shift the Deckers Outdoor (DECK) Growth Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, Stifel upgraded Deckers Outdoor to Buy from Hold, highlighting robust growth in the Hoka brand and a constructive outlook for UGG, especially in international markets.

- Despite management’s optimistic growth outlook and strong brand performance, the company anticipates ongoing tariff pressures impacting the US market through fiscal year 2027.

- We'll evaluate how Stifel's increased confidence, especially regarding Hoka's international strength, may shift the investment narrative for Deckers Outdoor.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Deckers Outdoor Investment Narrative Recap

To own shares in Deckers Outdoor, you need to believe in the ongoing international momentum of its key brands, Hoka and UGG, and trust the company's ability to weather sector headwinds. Stifel’s recent upgrade reflects increased optimism about Hoka’s strength abroad, but this does not materially change the biggest near-term risk: the impact of tariffs and price sensitivity in the US, nor does it alter the main short-term catalyst, which is the sustained growth of Hoka internationally.

Among recent announcements, Deckers’ October share buyback update stands out. The company repurchased nearly 2.9 million shares worth US$317 million, a signal of management's confidence and a move that could offer some support to per-share results. For investors, this is aligned with the view that international strength and margin management remain key to the short-term story.

Yet, with US tariffs expected to pressure profit margins through 2027, investors must also bear in mind the risk that...

Read the full narrative on Deckers Outdoor (it's free!)

Deckers Outdoor's outlook anticipates $6.5 billion in revenue and $1.1 billion in earnings by 2028. This forecast is based on an annual revenue growth rate of 8.5% and represents an increase in earnings of about $110 million from the current $989.7 million.

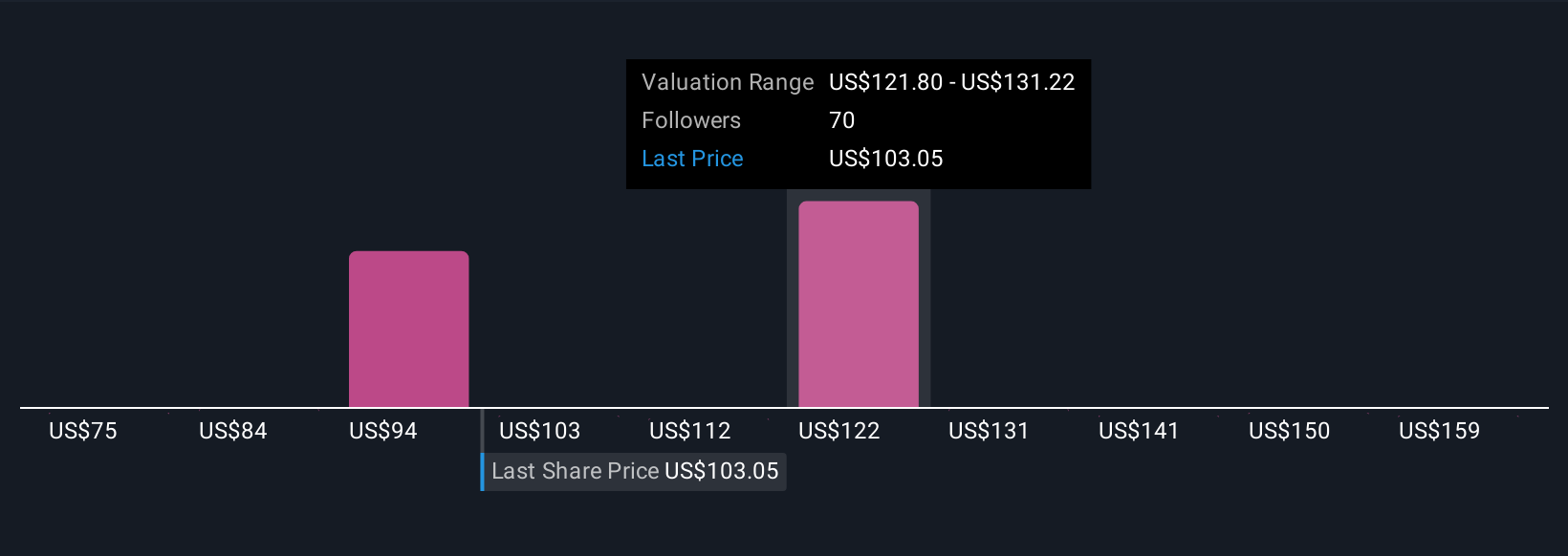

Uncover how Deckers Outdoor's forecasts yield a $111.97 fair value, a 28% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community produced 20 fair value estimates for Deckers, ranging from US$75.82 to US$158 per share. While many see significant upside, tariff-related risks and fluctuating brand performance remain key factors shaping future outcomes.

Explore 20 other fair value estimates on Deckers Outdoor - why the stock might be worth 13% less than the current price!

Build Your Own Deckers Outdoor Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Deckers Outdoor research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Deckers Outdoor research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deckers Outdoor's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DECK

Deckers Outdoor

Designs, markets, and distributes footwear, apparel, and accessories for casual lifestyle use and high-performance activities in the United States and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

98 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative