Advertisement

- United States

- /

- Luxury

- /

- NasdaqGS:LULU

What lululemon athletica (LULU)'s Slowing U.S. Sales and Tariff Pressures Mean For Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent months, lululemon athletica reported mixed results, with strong international growth but sluggish U.S. sales, prompting management to lower full-year revenue guidance while also facing higher tariffs and the removal of the de minimis duty exemption that threaten profit margins.

- These pressures, combined with elevated inventory levels and shifting consumer demand, have created a split view among analysts and options traders, who now see lululemon as a quality brand in transition rather than a straightforward growth story.

- We’ll now examine how stalled U.S. revenue and tariff-driven margin pressure may reshape lululemon’s previously optimistic investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

lululemon athletica Investment Narrative Recap

To stay invested in lululemon today, you have to believe the brand can reinvigorate its core U.S. business while using international growth and product innovation to offset tariff pressure on margins. The latest guidance cut and tariff headwinds directly affect the near term catalyst of a U.S. sales recovery, while also sharpening the main risk that discounting and slower demand could weigh on profitability if new products do not land quickly enough.

The most relevant recent update is lululemon’s reduced FY2025 revenue guidance to US$10.85 billion to US$11.00 billion, which explicitly builds in about US$240 million of net gross profit impact from tariffs and sourcing changes. This reinforces how central margin management has become to the story and sets a clearer bar for whether product resets, cost actions, and international expansion can collectively stabilize earnings in the next few quarters.

But behind the brand strength, investors should be aware of how higher tariffs and the lost de minimis relief could...

Read the full narrative on lululemon athletica (it's free!)

lululemon athletica's narrative projects $12.8 billion revenue and $1.9 billion earnings by 2028.

Uncover how lululemon athletica's forecasts yield a $190.19 fair value, in line with its current price.

Exploring Other Perspectives

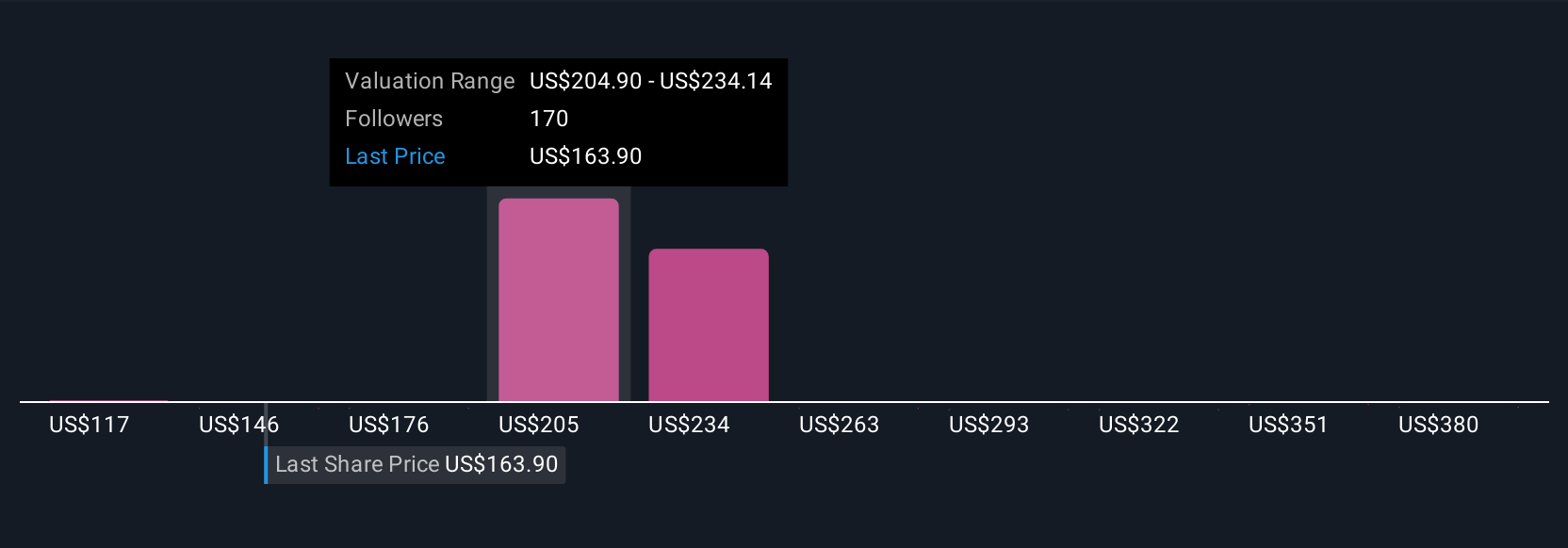

Simply Wall St Community members see lululemon’s fair value anywhere from about US$117 to over US$410 across 46 different views, highlighting very different expectations. Many of these investors are weighing that wide valuation spread against the same near term pressure points around U.S. softness and tariff driven margin risks, which could shape how the company performs relative to those expectations over time.

Explore 46 other fair value estimates on lululemon athletica - why the stock might be worth 38% less than the current price!

Build Your Own lululemon athletica Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if lululemon athletica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LULU

lululemon athletica

Designs, distributes, and retails technical athletic apparel, footwear, and accessories for women and men under the lululemon brand in the United States, Canada, Mexico, China Mainland, Hong Kong, Taiwan, Macau, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

68 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3925.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

68 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative