Advertisement

- United States

- /

- Professional Services

- /

- NYSE:TRU

TransUnion (TRU): Valuation Insights Following New Partnership to Enhance Resident Screening

Simply Wall St

Reviewed by Simply Wall St

TransUnion (TRU) unveiled a new partnership with Snappt that brings Snappt’s Applicant Trust Platform into the company’s TruVision Resident Screening. This unified approach combines advanced income verification and fraud detection with robust tenant screening tools, targeting the needs of today’s property managers.

See our latest analysis for TransUnion.

TransUnion’s collaboration with Snappt follows a string of recent product launches, including innovative fraud detection solutions and a steady dividend affirmation earlier this month. Even as new tools roll out, recent momentum has yet to translate into stock gains. TransUnion’s 1-year total shareholder return currently sits at -17%, though the 3-year figure still shows a healthy 35% total return. Investors appear to be weighing growth potential against shifting risk perceptions in the sector.

If this kind of strategic move has you curious about what else is gaining traction, it’s a great time to broaden your investing lens and discover fast growing stocks with high insider ownership

Yet with the stock trading at a notable discount to analyst targets and a healthy revenue outlook, investors may be wondering if the recent dip signals an undervalued entry or if the market is already factoring in future growth.

Most Popular Narrative: 25% Undervalued

With TransUnion's fair value estimated at $106.95 and a recent closing price of $80.17, the most followed narrative puts the share price at a substantial discount versus forward-looking expectations. The narrative draws on pivotal innovations, operational upgrades, and market momentum to arrive at this view.

Strategic innovation investments, including AI, machine learning, and the roll-out of the global cloud-native OneTru platform, are driving efficiency, faster product launches, better cross-sell opportunities, and improved customer retention. These factors are positioning TransUnion to grow earnings with higher operating leverage and net margins as technology transformation costs subside post-2025.

Want to see which bold forecasts underpin that $100+ price target? The narrative hints at aggressive profit improvement and a future multiple rarely seen outside high-growth sectors. What did the analysts bet on to justify their upside view? Find out which precise business drivers and financial projections are setting this valuation apart.

Result: Fair Value of $106.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing regulatory changes and rising cyber threats could still disrupt the bullish case and put pressure on TransUnion's long-term profitability.

Find out about the key risks to this TransUnion narrative.

Another View: Multiples Raise a Different Flag

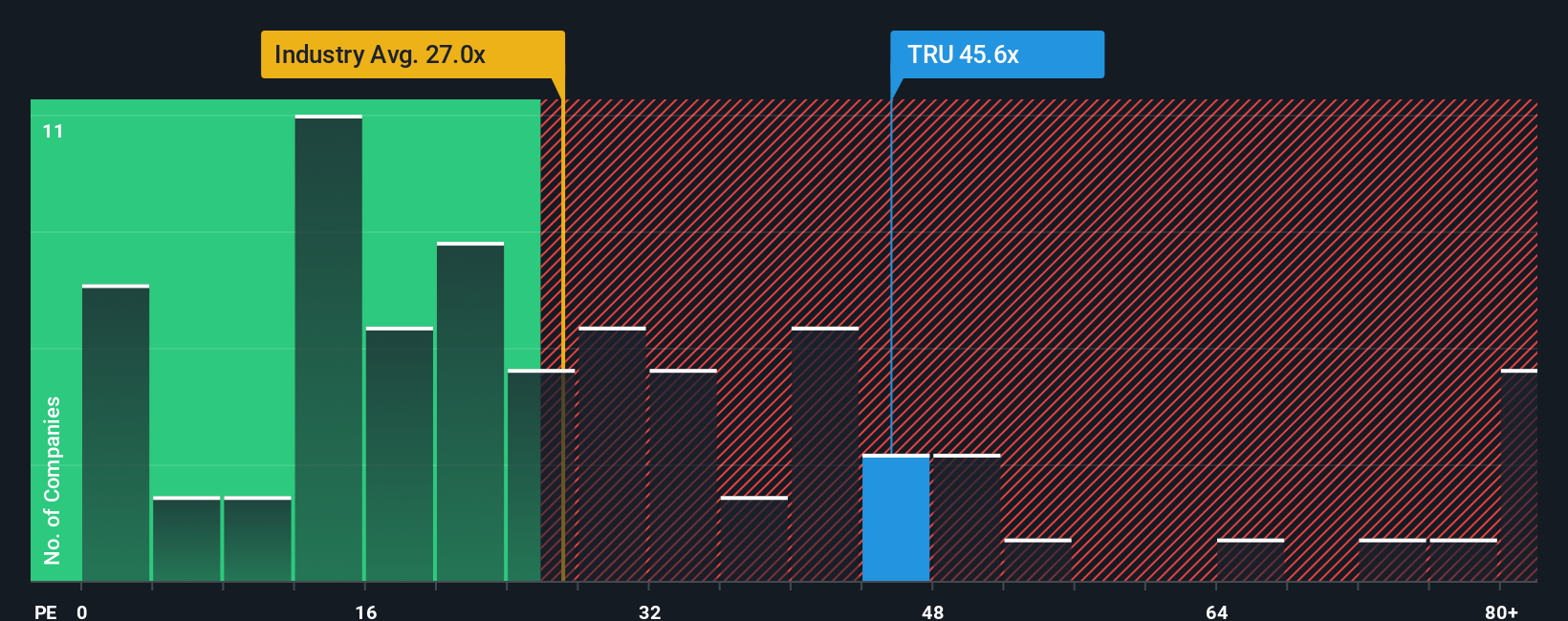

While discounted cash flow points to a hefty discount, looking at TransUnion's price-to-earnings ratio offers a different lens. The shares are trading at 37 times earnings, noticeably above both the industry average (23.2x) and peer average (33.3x). Even compared to its fair ratio of 31.5x, the current price hints at a valuation risk if market sentiment shifts. Are investors paying a premium for future growth or overlooking crucial red flags?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own TransUnion Narrative

If you’re the type who likes to dig into the numbers or craft your own investment thesis, you can uncover your perspective in just a few minutes and Do it your way

A great starting point for your TransUnion research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Step ahead of the market and seize opportunities others might overlook by targeting top-performing stocks that fit your personal strategy using the Simply Wall Street Screener.

- Build on high-yield potential by checking out these 18 dividend stocks with yields > 3%, where dependable returns and strong yields are the main focus.

- Tap into the next tech revolution by finding your favorites among these 27 AI penny stocks, which includes companies leading the charge in artificial intelligence breakthroughs.

- Stay ahead of value trends by reviewing these 905 undervalued stocks based on cash flows, highlighting quality stocks trading below their intrinsic worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransUnion might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TRU

TransUnion

Operates as a global consumer credit reporting agency that provides risk and information solutions.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative