Advertisement

- United States

- /

- Professional Services

- /

- NYSE:MAN

Does ManpowerGroup’s 50% Stock Drop Signal a Hidden Opportunity for Investors in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if ManpowerGroup's beaten-down stock could actually be a hidden bargain? Let's dive into what matters most for value-seeking investors.

- The share price recently edged up 1.3% over the last week, but it is still down a steep 50.1% year-to-date and almost 54% lower than this time last year. This has caught the attention of both bargain hunters and risk-watchers.

- Much of this dramatic price swing has unfolded against a backdrop of shifting market sentiment and evolving trends in the broader staffing industry. Rising competition and changing labor market dynamics have played a role, while news of ongoing workforce transitions and new government policies impacting labor suppliers has further spurred volatility and investor debate.

- Interestingly, ManpowerGroup scores a perfect 6 out of 6 on our core valuation checks, which may appeal to anyone focused on underlying value. Let’s look at the numbers from multiple valuation angles to see if conventional wisdom stacks up and stick around for an alternative, potentially even more insightful approach at the end.

Find out why ManpowerGroup's -53.9% return over the last year is lagging behind its peers.

Approach 1: ManpowerGroup Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by projecting ManpowerGroup's future cash flows and then discounting them back to their present value. This approach provides investors with an estimate of the company's current worth based on its expected financial performance.

According to this model, ManpowerGroup's most recent twelve months of Free Cash Flow are approximately -$98.3 million. Analysts anticipate a turnaround, with projections suggesting steady recovery and growth over the next decade, culminating in a Free Cash Flow of $298.9 million by 2035. While analyst estimates guide only the next five years, Simply Wall St extrapolates for the remaining years using conservative growth assumptions to produce a ten-year outlook in US dollars.

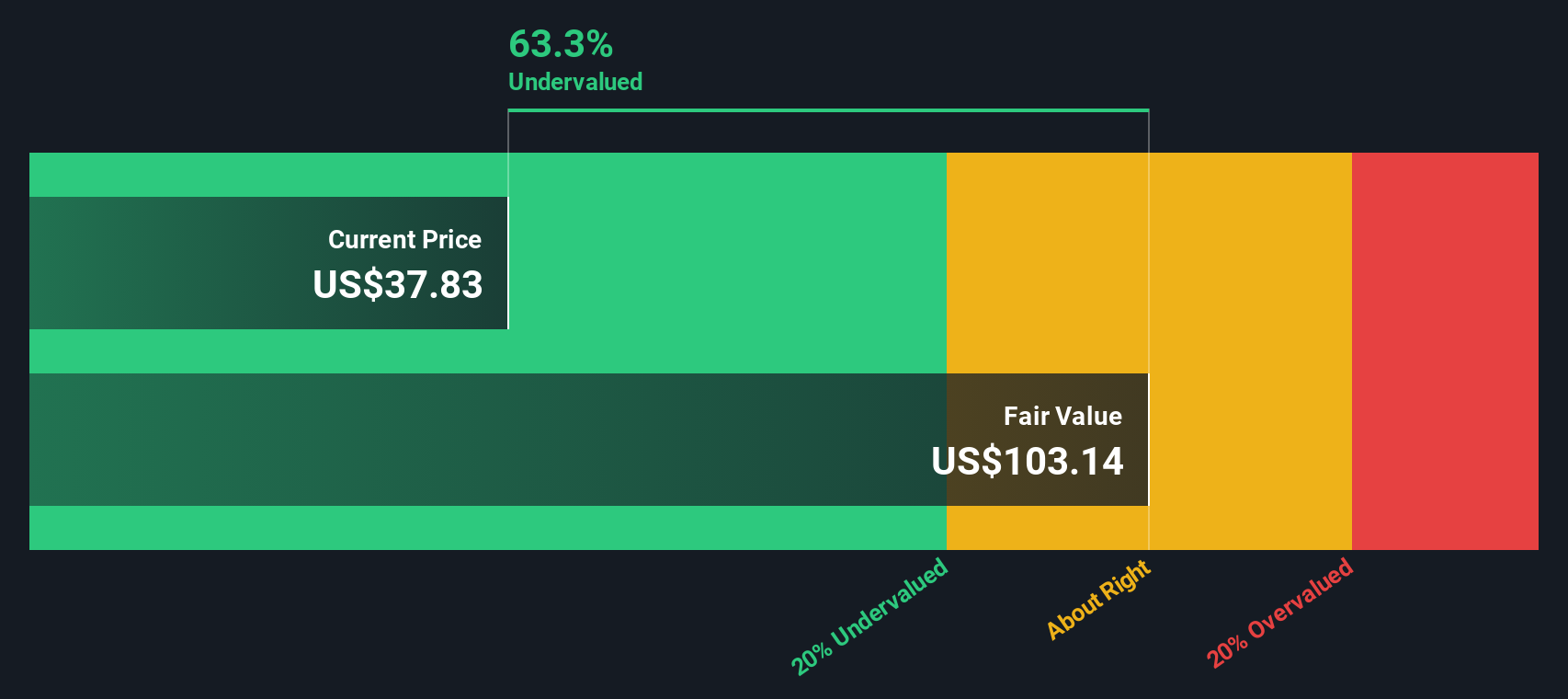

By summing all the discounted future cash flows, the DCF analysis results in an estimated fair value for ManpowerGroup of $78.06 per share. Compared to the current market price, this calculation suggests the stock is trading at a 63.5% discount to its intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ManpowerGroup is undervalued by 63.5%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

Approach 2: ManpowerGroup Price vs Sales

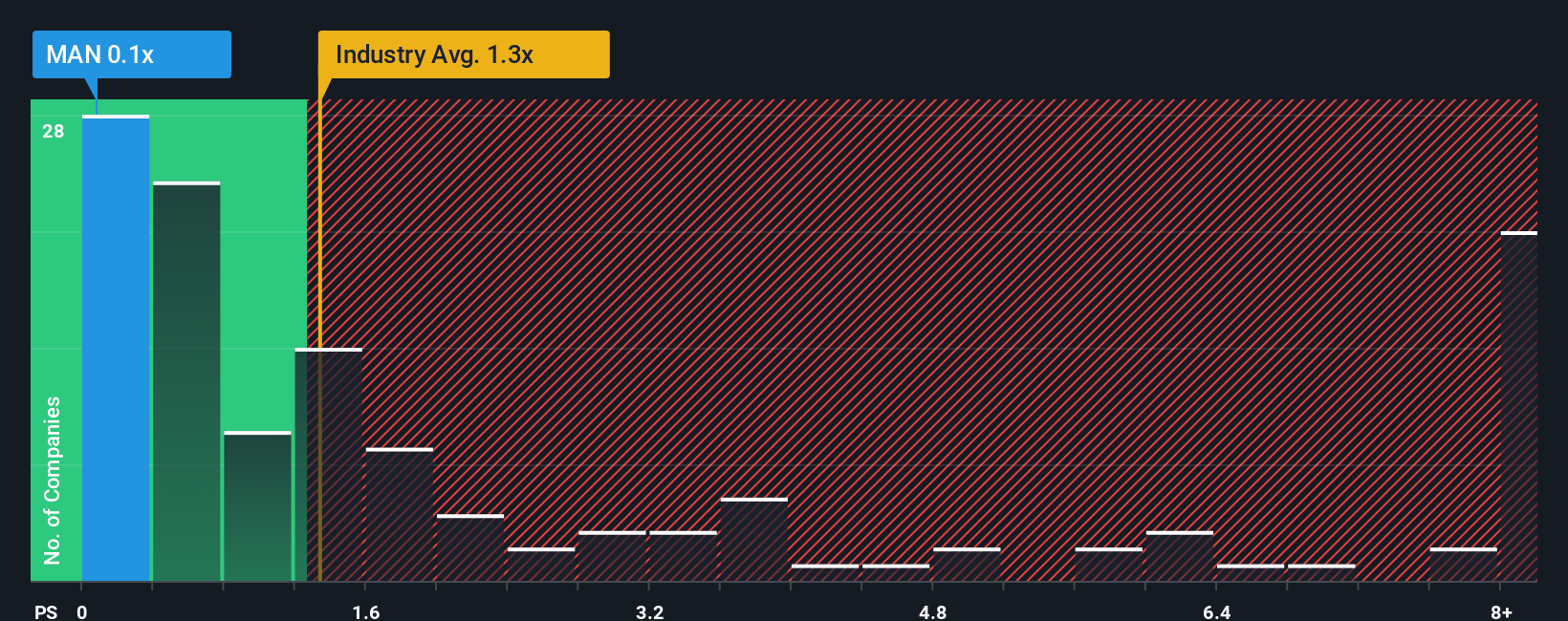

The Price-to-Sales (P/S) ratio is often used as a preferred valuation metric for companies like ManpowerGroup, particularly in situations where earnings may be negative or highly variable. For businesses in the professional services sector, where margins can fluctuate, the P/S ratio provides a clear snapshot of how the market values each dollar of revenue.

A "normal" or "fair" P/S ratio for a company depends on various factors including its growth outlook and risk profile. If investors expect a firm to expand quickly or enjoy a dominant market position with low risks, they are typically willing to pay a higher multiple. Conversely, lower growth and higher risks justify lower valuation multiples.

Currently, ManpowerGroup trades at a P/S ratio of just 0.07x. This stands in sharp contrast to the industry average of 1.34x and the peer average of 0.62x. On the surface, this deep discount is striking, but context is key. Simply Wall St’s proprietary Fair Ratio for ManpowerGroup is 0.67x. This reflects the company's unique combination of earnings growth, profit margins, industry trends, market capitalization, and risk profile.

Unlike simple peer and industry comparisons, the Fair Ratio method accounts for factors specific to ManpowerGroup’s circumstances. This provides a more precise benchmark for intrinsic value and helps investors sidestep common valuation pitfalls by focusing on what really matters for the stock.

Comparing the Fair Ratio of 0.67x to the actual P/S multiple of 0.07x, ManpowerGroup appears clearly undervalued on a sales basis.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1437 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ManpowerGroup Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your story or perspective about a company’s future. It is how you connect what you believe about ManpowerGroup’s growth, earnings, industry changes, and risks to a financial forecast, turning your viewpoint into a personalized fair value estimate.

Rather than relying only on common ratios or consensus targets, Narratives let you anchor your decisions in what you think will really drive the stock. For example, is ManpowerGroup’s AI-driven strategy and global expansion likely to boost margins and stabilize earnings, or do headwinds like automation risk and regional underperformance pose bigger threats?

On Simply Wall St’s Community page, millions of investors use Narratives to track how fair value changes compared to the current share price. This makes it easier to decide when to buy or sell based on your own assumptions and to see how others think differently.

Narratives automatically update when new news or earnings reports appear, keeping your view factual, current, and actionable.

For example, some investors see ManpowerGroup’s story supporting a future price of $55 based on successful AI adoption and strong revenue growth, while others project just $39 if regional challenges and competition outweigh the positives. Narratives help you put your beliefs into numbers and invest with conviction.

Do you think there's more to the story for ManpowerGroup? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MAN

ManpowerGroup

Provides workforce solutions and services under the Talent Solutions, Manpower, and Experis brands worldwide.

Very undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

99 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative