Advertisement

- United States

- /

- Professional Services

- /

- NYSE:LDOS

Is It Too Late To Consider Leidos After Its Strong Multi Year Share Price Gains?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Leidos Holdings is still a smart buy after its big run, or if the easy money has already been made? This breakdown will help you decide whether the current price still offers value.

- The stock trades around $185.62 after a modest pullback of 1.5% over the last week and 5.8% over the last month. It is still up 29.5% year to date and 17.0% over the last year, with a 78.8% gain over three years and 89.8% over five years.

- Recent moves have been shaped by steady contract wins in defense, intelligence, and civil government work, alongside growing interest in the company’s role in digital modernization and cyber solutions. Investors are increasingly viewing Leidos as a key long term beneficiary of sustained US government spending on technology, security, and mission critical services.

- On our core valuation checks, Leidos scores a 5 out of 6, suggesting it still looks attractively priced on several fronts. Next we will walk through the main valuation approaches we use, before finishing with a more holistic way to think about what the stock is really worth.

Approach 1: Leidos Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in dollar terms.

For Leidos Holdings, the latest twelve month Free Cash Flow is about $1.33 billion. Analysts expect this to rise steadily, with Simply Wall St extending their forecasts beyond the formal analyst horizon using a 2 Stage Free Cash Flow to Equity model. Under these projections, annual Free Cash Flow is expected to be around $2.19 billion by 2035, illustrating a solid long term growth trajectory from today’s levels.

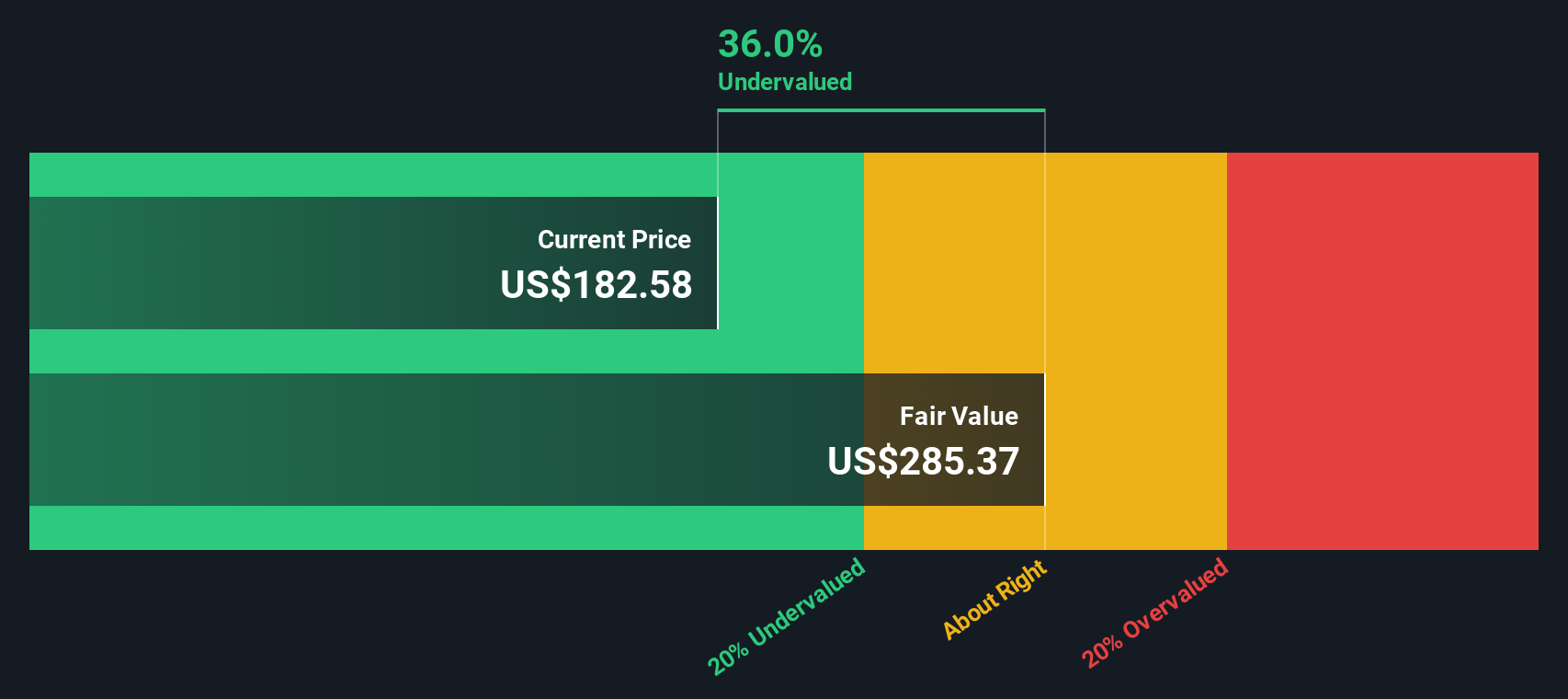

When all those future cash flows are discounted back to the present, the model arrives at an intrinsic value of roughly $299.87 per share. Compared with the recent share price around $185.62, the DCF implies the stock is about 38.1% undervalued, indicating a sizeable potential upside if the cash flow projections are realized.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Leidos Holdings is undervalued by 38.1%. Track this in your watchlist or portfolio, or discover 902 more undervalued stocks based on cash flows.

Approach 2: Leidos Holdings Price vs Earnings

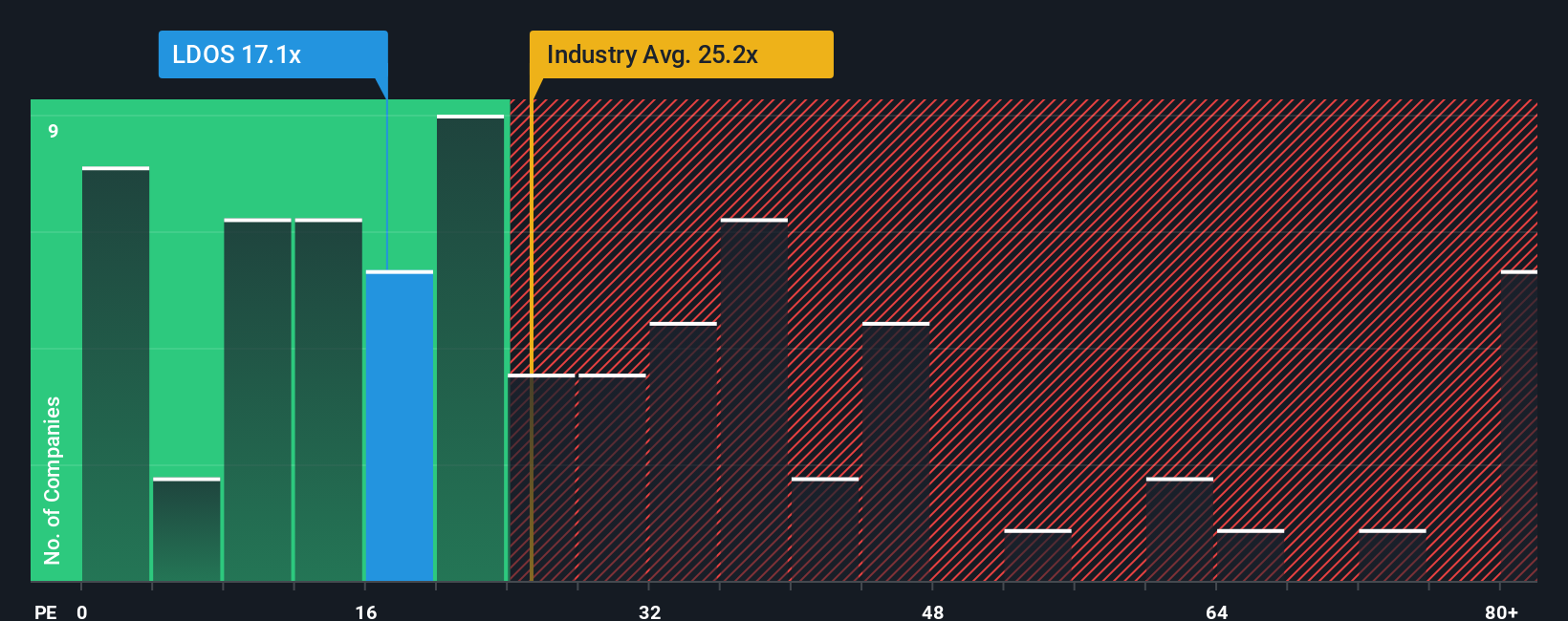

For a profitable business like Leidos, the Price to Earnings (PE) ratio is a useful way to gauge how much investors are paying for each dollar of current earnings. A higher PE usually reflects stronger growth expectations or lower perceived risk, while a lower PE can signal weaker prospects or higher uncertainty. In other words, what counts as a normal or fair PE largely depends on how fast earnings are expected to grow and how reliable those earnings are.

Leidos currently trades on a PE of about 16.9x. That is well below the Professional Services industry average of roughly 25.0x and also below the broader peer group average of around 39.1x. This suggests the market is valuing Leidos at a discount to many comparable companies. Simply Wall St also calculates a proprietary Fair Ratio of 26.1x for Leidos, based on its earnings growth outlook, profitability, risk profile, industry and market cap. This Fair Ratio is more informative than a simple peer or industry comparison because it adjusts for the company’s specific strengths and risks rather than assuming all companies deserve similar multiples.

Since the Fair Ratio of 26.1x sits meaningfully above the current 16.9x, Leidos appears undervalued on a PE basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1453 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Leidos Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to turn your view of a company into a story that links its business drivers to a financial forecast and, ultimately, to a fair value estimate.

On Simply Wall St, Narratives live in the Community page and are used by millions of investors to describe how they think a company’s revenue, earnings and margins will evolve, then translate that story into a forecast and a fair value that can be compared against today’s share price to inform their decision on whether to buy, hold or sell.

Because Narratives on the platform update dynamically as new earnings, news and guidance are released, they stay current and can highlight when the gap between Fair Value and Price is widening or closing. This can help you react faster and with more confidence.

For example, some Leidos investors might build a bullish Narrative that assumes strong Health and Civil margins, AI driven efficiency gains and a fair value closer to $230 per share. More cautious investors may focus on government funding risks and margin pressure to justify a fair value nearer to $164, and the Community makes it easy to see and compare both perspectives side by side.

Do you think there's more to the story for Leidos Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LDOS

Leidos Holdings

Provides services and solutions for government and commercial customers in the United States and internationally.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RA

RacerBVN on iShares Trust - iShares Preferred and Income Securities ETF ·

This one is all about the tax benefits

Fair Value:US$54.5543.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FatPie on SoFi Technologies ·

Estimated Share Price is $79.54 using the Buffett Value Calculation

Fair Value:US$79.5465.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative