Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Will International Revenue Pressures and Analyst Downgrade Change Watsco's (WSO) Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- In the quarter ending September 2025, Watsco reported declines in international revenue from Canada and Latin America and the Caribbean, missing Wall Street expectations for the period.

- This shortfall, paired with analysts now projecting an annual revenue decrease and rating the company a Strong Sell, signals significant headwinds from international operations.

- We’ll examine how renewed international revenue pressures challenge the previous growth outlook for Watsco’s broader investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

Watsco Investment Narrative Recap

To be a Watsco shareholder, you need to have confidence in the long-term demand for HVAC products and the company’s ability to navigate challenges like tariffs and international market volatility. The recent report of declining international revenue and a negative analyst outlook raises concerns around the most pressing short-term catalyst, the transition to high-efficiency A2L systems, and spotlights international headwinds as the biggest current risk. For now, these international pressures appear material, potentially dampening momentum from ongoing product transitions.

The most relevant recent development is Watsco's October Q3 earnings announcement, which confirmed not only lower sales but also a drop in net income for the third consecutive quarter. This aligns directly with the warnings on international revenue pressures and gives investors fresh numbers to consider when weighing the potential impact of these headwinds on future performance.

By contrast, what investors might miss is how additional cost uncertainty, such as new tariffs, could further complicate...

Read the full narrative on Watsco (it's free!)

Watsco's outlook anticipates $9.1 billion in revenue and $758.2 million in earnings by 2028. This requires 6.5% annual revenue growth and a $262.7 million earnings increase from the current $495.5 million level.

Uncover how Watsco's forecasts yield a $415.60 fair value, a 19% upside to its current price.

Exploring Other Perspectives

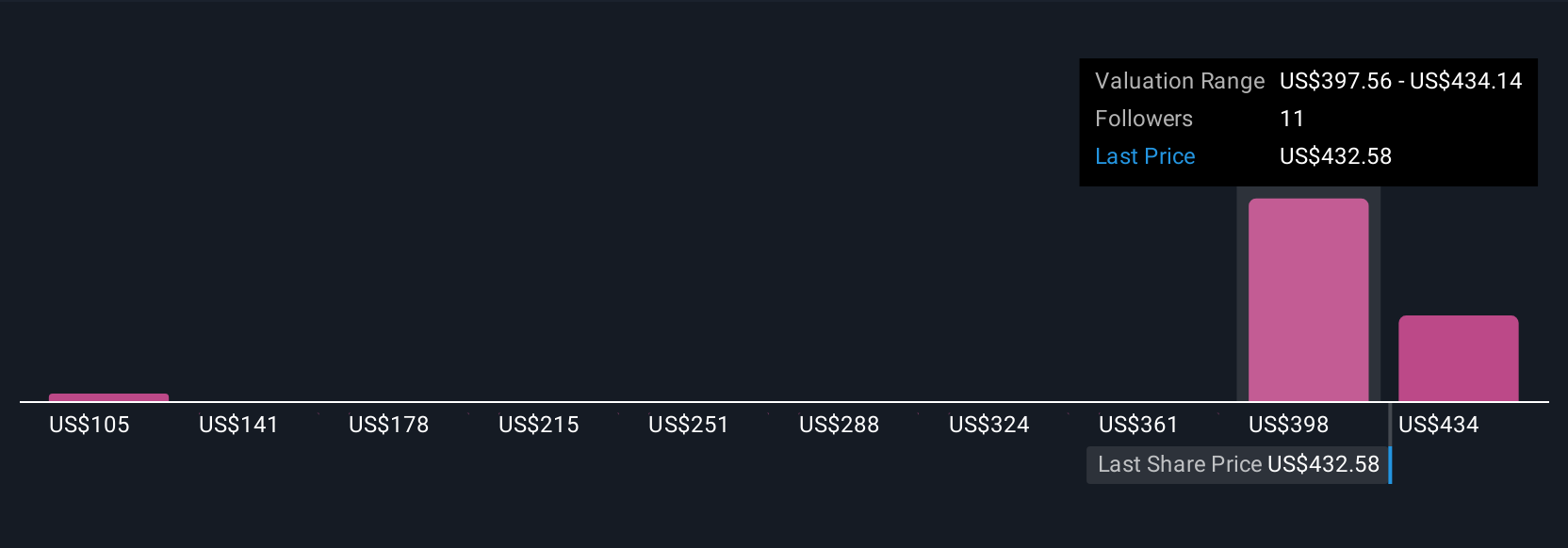

Simply Wall St Community members have set fair value estimates for Watsco ranging from US$104.90 to US$415.60, based on three different analyses. With international operations contributing to recent revenue disappointments, your outlook could shift depending on how you weigh global market risks.

Explore 3 other fair value estimates on Watsco - why the stock might be worth less than half the current price!

Build Your Own Watsco Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Watsco research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Watsco research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Watsco's overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Watsco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor