Advertisement

- United States

- /

- Machinery

- /

- NYSE:TKR

Is Timken’s (TKR) Upbeat Outlook and Share Buyback Shaping a Stronger Investment Case?

Simply Wall St

Reviewed by Sasha Jovanovic

- The Timken Company recently reported third quarter 2025 results, highlighting sales of US$1,157.1 million and net income of US$69.3 million, alongside the completion of an 8,500,489 share repurchase program for US$617.37 million initiated in 2021.

- Timken revised its 2025 full-year earnings outlook upwards, coupled with management emphasizing disciplined cost control, improved price realization, and a continued review of its portfolio for margin enhancement opportunities.

- We'll explore how Timken’s updated 2025 earnings guidance and focus on cost efficiency may influence its corporate outlook and investment thesis.

Find companies with promising cash flow potential yet trading below their fair value.

Timken Investment Narrative Recap

To believe in Timken as a shareholder, you need confidence in its ability to return to earnings and margin growth through cost control, pricing initiatives, and a focus on portfolio optimization, despite industrial demand risks. The latest third quarter results and the completion of a major share buyback do not materially affect the immediate catalyst, the company’s ongoing margin recovery, but highlight the current challenge of lower net margins due to volume softness and cost pressures. The company’s updated full-year earnings guidance, now calling for US$3.90 to US$4.00 per diluted share, stands as the most relevant announcement, offering a slightly improved revenue outlook despite muted top-line growth, and supports the idea that disciplined cost management remains central to the near-term investment case. However, with intensifying pricing competition and persistent demand softness in key regions, investors should be aware that ...

Read the full narrative on Timken (it's free!)

Timken's outlook sees revenues reaching $4.9 billion and earnings hitting $474.3 million by 2028. This is based on analysts' projections of 2.7% annual revenue growth and an earnings increase of $164.5 million from the current $309.8 million.

Uncover how Timken's forecasts yield a $85.87 fair value, a 9% upside to its current price.

Exploring Other Perspectives

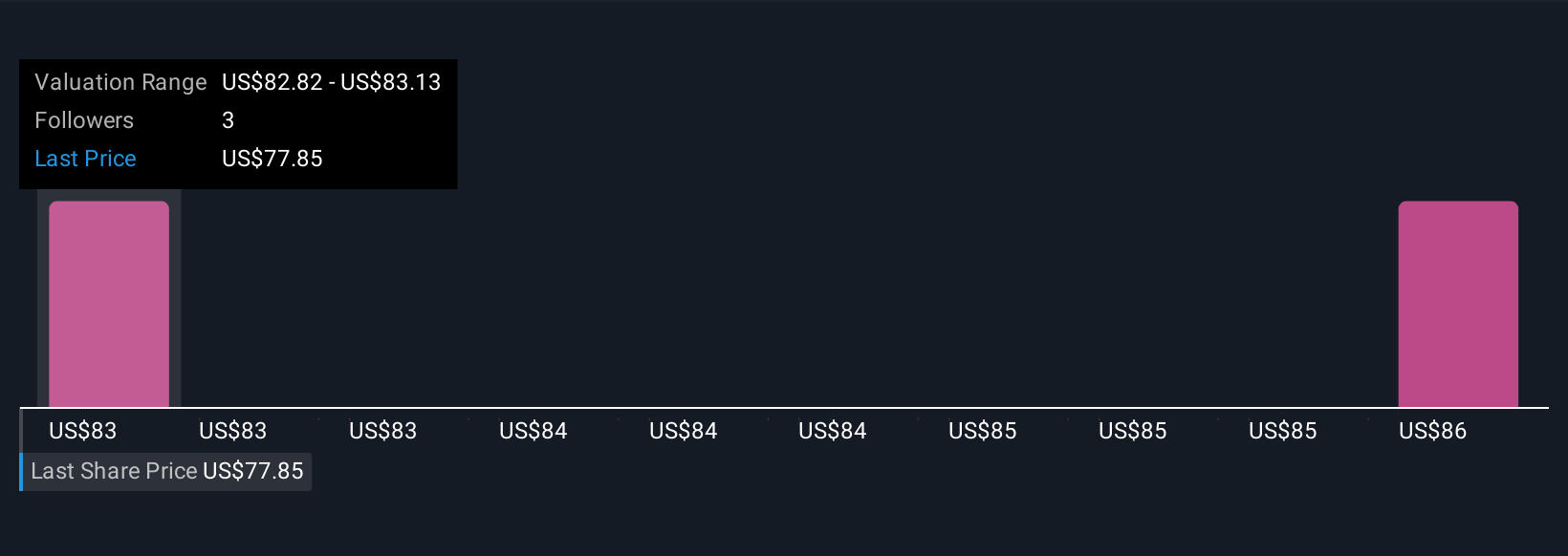

Simply Wall St Community members estimate fair value between US$82.76 and US$85.87 based on two perspectives. While some anticipate margin recovery driven by cost savings, keep in mind that opinions broadly differ, so explore alternative viewpoints closely tied to current market conditions.

Explore 2 other fair value estimates on Timken - why the stock might be worth as much as 9% more than the current price!

Build Your Own Timken Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Timken research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Timken research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Timken's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Timken might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TKR

Timken

Designs, manufactures, and sells engineered bearings and industrial motion products, and related services in the United States and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor