Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:RTX

Is RTX Fairly Priced After Strong 44.8% Year-To-Date Return?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious whether RTX is priced fairly in today's market, or if there is a hidden value waiting to be unlocked? You are not alone. This stock's story is catching attention from investors seeking both stability and opportunity.

- While the share price is down 2.4% over the past week and 5.9% in the last month, RTX has delivered a strong 44.8% return year-to-date and an impressive 153.0% return over the last five years.

- RTX's recent price trends have been shaped by a string of industry updates and macroeconomic headlines, including renewed focus on defense contracts and supply chain resilience. These developments have contributed to both optimism about future growth and caution around potential volatility.

- The company currently scores a 3 out of 6 on our valuation checks, signaling the market may be split on how much value is left on the table. Let's break down the classic valuation approaches you should know, and stay tuned for a perspective that can help you dig even deeper at the end of the article.

Approach 1: RTX Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them to reflect their value in today’s dollars. This approach helps investors understand what a business is truly worth based on the cash it is expected to generate in the years ahead.

For RTX, the current Free Cash Flow stands at $4.47 Billion. Analyst estimates suggest this figure will increase each year, reaching a projected $10.77 Billion by 2029. After 2029, forecasts rely on careful extrapolation rather than direct analyst estimates. The DCF model used here is a Two Stage Free Cash Flow to Equity approach, which blends both analyst insight and methodical projections to build out a 10-year view of RTX’s potential.

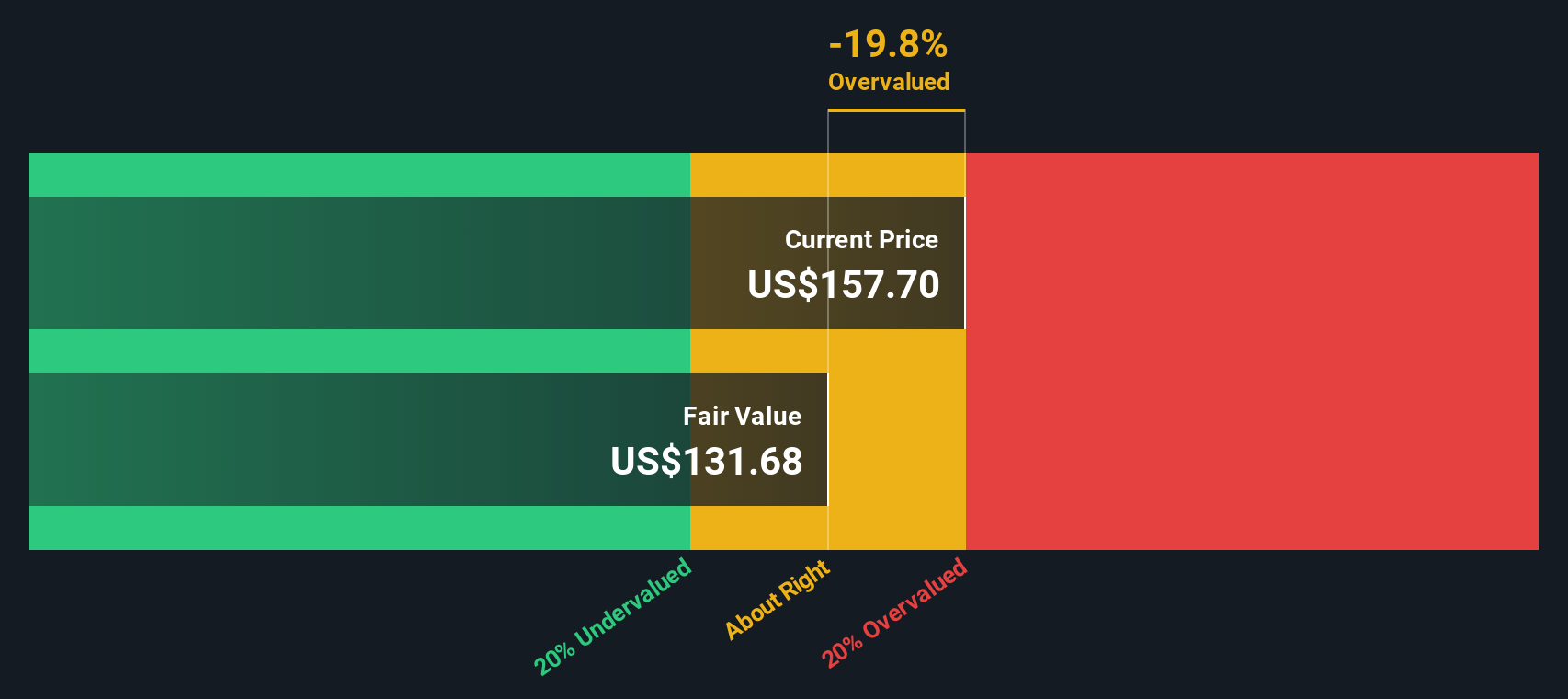

According to the DCF valuation, RTX’s estimated intrinsic value is $144.75 per share. However, this model suggests the stock is trading at a 16.1% premium to its fair value, indicating RTX may be overvalued at current market levels.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests RTX may be overvalued by 16.1%. Discover 930 undervalued stocks or create your own screener to find better value opportunities.

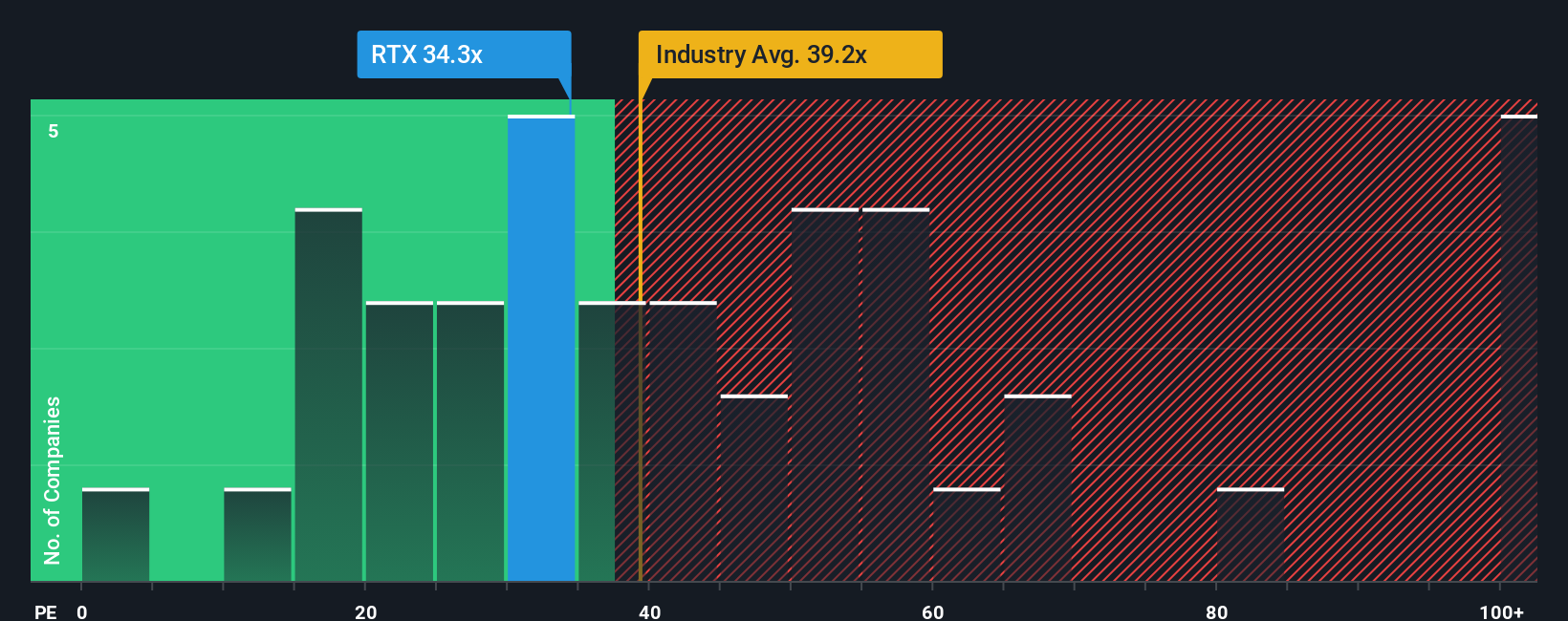

Approach 2: RTX Price vs Earnings

The Price-to-Earnings (PE) ratio is widely used to value profitable companies because it relates the market price of a stock to its underlying earnings. This offers a direct sense of how investors value every dollar of profit RTX generates. This metric is particularly useful for stable, mature businesses like RTX, where earnings form a key driver of long-term returns.

The “right” PE ratio for any company depends on expectations for future growth and the risks it faces. Companies expected to grow quickly or those seen as less risky tend to trade at higher PE ratios. Slower-growing or riskier businesses trade at lower PE ratios.

RTX currently trades on a PE ratio of 34.2x. This is in line with its peer average of 34.6x and just below the Aerospace & Defense industry average of 37.8x. These comparisons suggest the market values RTX similarly to its direct competitors and the broader sector.

Simply Wall St’s proprietary Fair Ratio model provides a more tailored benchmark. The Fair Ratio, calculated at 35.3x for RTX, adjusts for specific factors such as the company’s future earnings growth, profit margins, risk, market cap, and industry conditions. This model goes beyond raw peer or industry comparisons and reflects what is considered reasonable for RTX in its specific context.

With RTX’s current PE ratio of 34.2x sitting just below the Fair Ratio, the stock appears to be priced about right based on its core fundamentals and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your RTX Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your story for a company like RTX, linking your view of its future, such as key catalysts, growth opportunities, and risks, to a specific forecast for revenue, earnings, and profit margins, and ultimately your own estimate of fair value.

Narratives connect the numbers to real-world developments by making it easy for investors to build and track their unique perspective on a stock. Think of it as a bridge between what’s happening on the ground and the company’s true worth. This powerful feature is available on Simply Wall St’s Community page, where millions of investors create, share, and refine Narratives in just a few clicks without the need for spreadsheets.

With Narratives, you can clearly see when the Fair Value you have calculated signals a buy or sell compared to the current share price. And because Narratives update dynamically with new company news and earnings, your valuation stays relevant and actionable at all times.

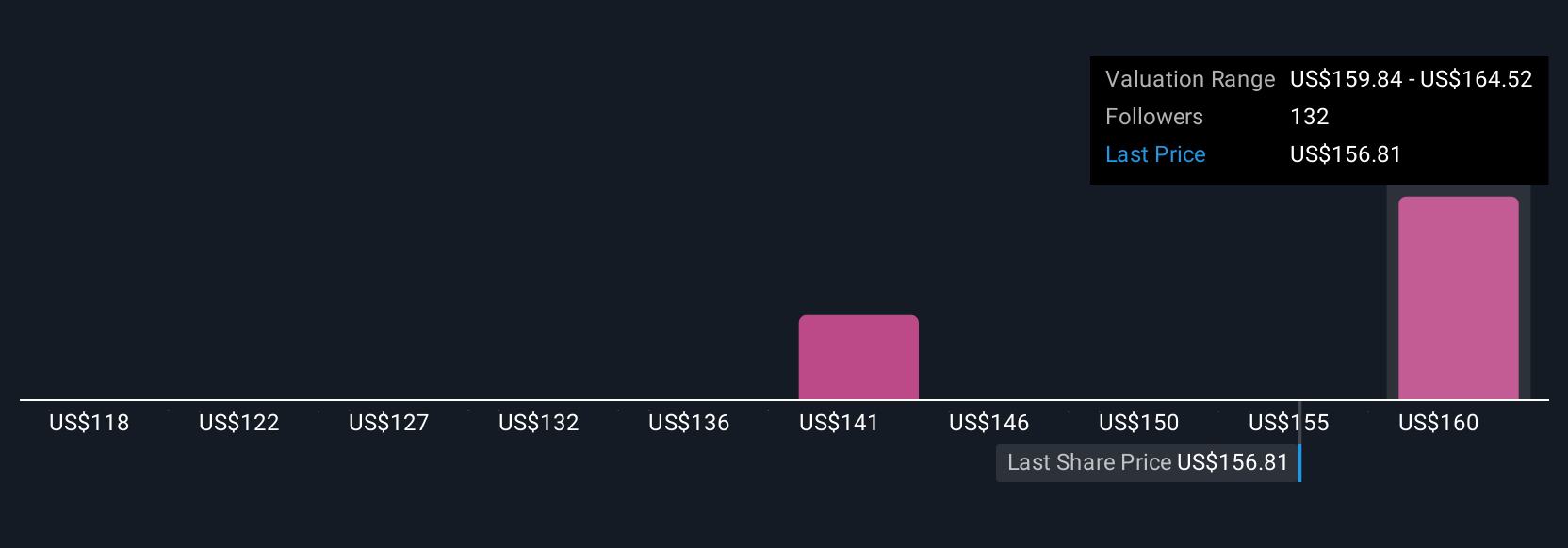

For example, some RTX investors forecast strong defense contract growth and tech-driven margin expansion, resulting in a bullish Fair Value of $180 per share. Others focus on risks like engine overruns or defense budget pressures, arriving at a much more conservative $134 per share.

Do you think there's more to the story for RTX? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RTX

RTX

An aerospace and defense company, provides systems and services for the commercial, military, and government customers in the United States and internationally.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.7% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative