Advertisement

- United States

- /

- Machinery

- /

- NYSE:OSK

How Oshkosh’s (OSK) Lowered Revenue Outlook Could Influence Investor Expectations for Future Growth

Simply Wall St

Reviewed by Sasha Jovanovic

- Oshkosh Corporation recently reported its third-quarter 2025 results, showing US$2.69 billion in sales and US$196.2 million in net income, while also announcing a US$0.51 per share dividend and updates on share repurchases.

- Despite higher net income year-over-year, Oshkosh lowered its full-year revenue guidance due to anticipated declines in Transport and Access segment sales volumes, highlighting shifting demand patterns in key business areas.

- With Oshkosh lowering its revenue outlook, we’ll explore how this revised forecast shapes the company’s investment narrative and future growth assumptions.

We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Oshkosh Investment Narrative Recap

At its core, the Oshkosh investment story centers on stable long-term demand for specialty vehicles and strong positions in government and infrastructure-driven markets. The recent guidance cut, though reflecting headwinds in the Transport and Access segments, does not appear to sharply alter the main short-term catalyst: continued growth and earnings from large public-sector contracts. The biggest risk remains revenue volatility tied to shifting government priorities, which investors should weigh as sales guidance adjusts.

The announcement most relevant to this update is Oshkosh lowering its full-year revenue forecast for 2025, now expected at US$10.3 to US$10.4 billion, down from prior guidance. This update directly addresses softer market conditions in key segments and raises questions about near-term visibility for recurring revenue from public and private sector customers. But while forecasts have changed, investors may be watching for whether recent growth drivers can offset these cyclical swings.

However, the real test for investors will be if shifting government orders or funding priorities become a bigger issue than expected…

Read the full narrative on Oshkosh (it's free!)

Oshkosh's narrative projects $12.0 billion revenue and $940.2 million earnings by 2028. This requires 5.1% yearly revenue growth and a $289.8 million earnings increase from $650.4 million.

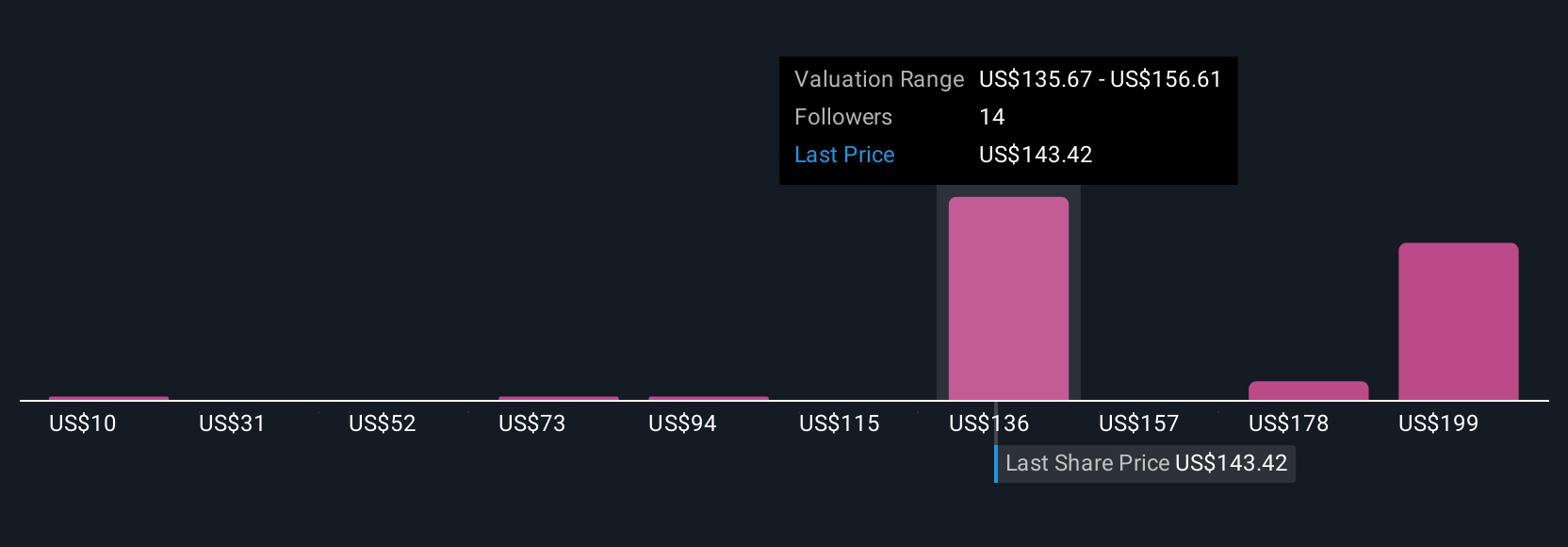

Uncover how Oshkosh's forecasts yield a $153.08 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offer seven fair value estimates for Oshkosh, ranging widely from US$10 up to US$252.51. With guidance now lowered due to softer Transport and Access outlooks, awareness of uncertain revenue streams is key as you compare these diverse views.

Explore 7 other fair value estimates on Oshkosh - why the stock might be worth over 2x more than the current price!

Build Your Own Oshkosh Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Oshkosh research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Oshkosh research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Oshkosh's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OSK

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor