Advertisement

- United States

- /

- Machinery

- /

- NYSE:JBTM

Does Analyst Upgrade and Raised Earnings Outlook Shift the Bull Case for JBT Marel (JBTM)?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, JBT Marel Corporation received an upgraded Zacks Rank as analysts raised their full-year earnings estimates by 7.8%, reflecting improved sentiment about the company’s outlook. This positive reappraisal placed JBT Marel ahead of its Business Services peers, underscoring its differentiated performance in a challenging sector landscape.

- With analysts raising full-year earnings estimates, we’ll examine how this momentum could influence JBT Marel’s investment narrative going forward.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

JBT Marel Investment Narrative Recap

For anyone considering JBT Marel, confidence in the global need for food safety automation and integrated processing solutions is key. The recent analyst upgrades and improved earnings outlook do provide positive momentum, yet the most important short-term catalyst, the realization of merger synergies, remains largely unchanged. At the same time, significant risks from unresolved integration challenges and margin pressures due to tariffs still warrant close attention; the overall impact of analyst upgrades on these factors appears modest.

JBT Marel's Q3 earnings report stands out, with year-over-year sales nearly doubling and incremental gains in net income. This supports the company’s growth prospects, as automation demand and merger integration continue to shape its earnings potential; however, whether growth offsets risks tied to margin headwinds or executive transitions is yet to be seen.

On the other hand, investors should not overlook the ongoing uncertainties surrounding tariff-driven cost pressures and the company’s ongoing supply chain adjustments, as these could...

Read the full narrative on JBT Marel (it's free!)

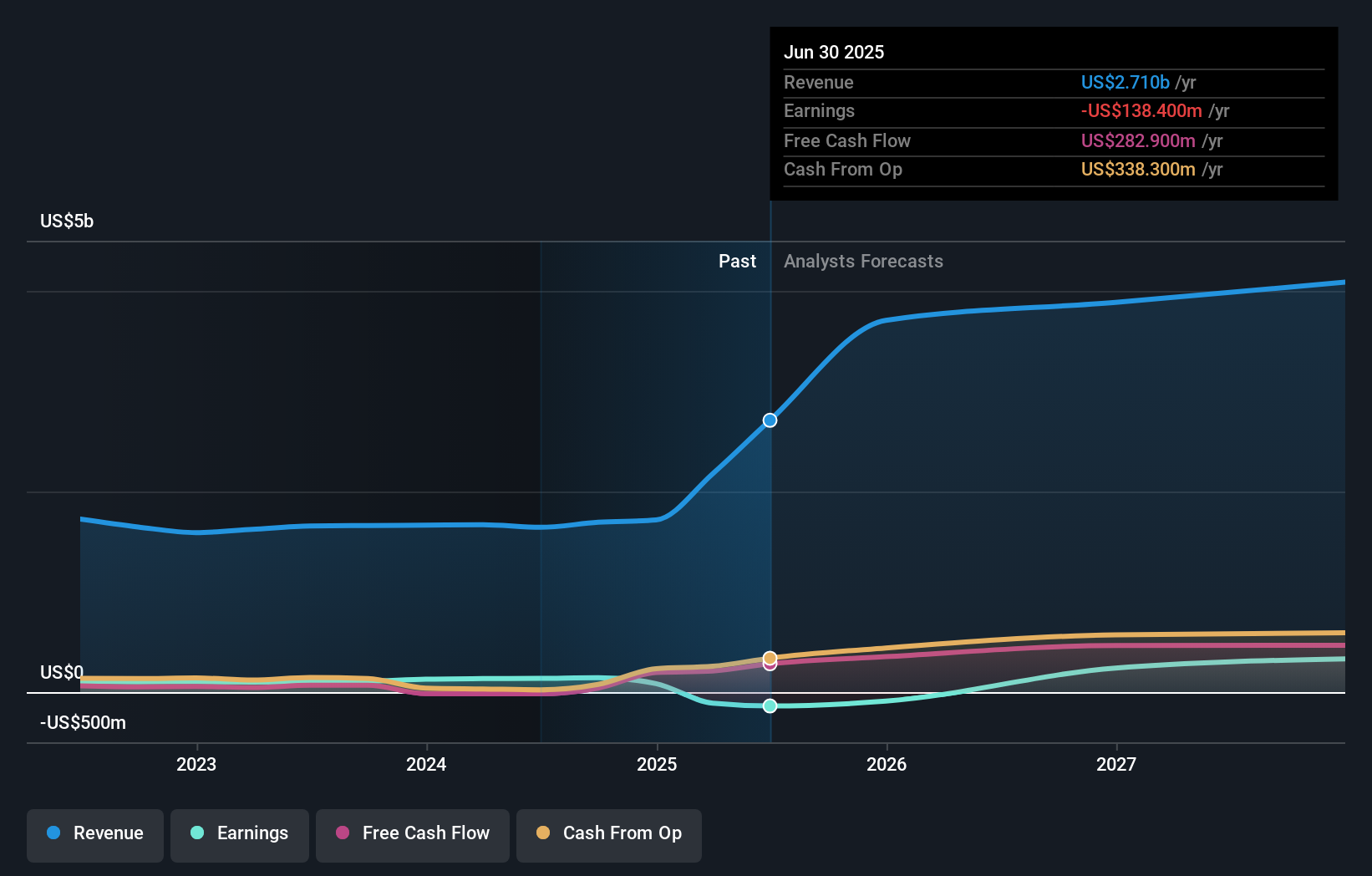

JBT Marel's outlook anticipates $4.6 billion in revenue and $591.0 million in earnings by 2028. This scenario assumes a 19.0% annual revenue growth rate and a $729.4 million increase in earnings from the current -$138.4 million.

Uncover how JBT Marel's forecasts yield a $155.25 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Retail investors in the Simply Wall St Community have published two fair value estimates for JBT Marel, spanning from US$155.25 to US$179.24 per share. These opinions highlight the wide range of views on future upside, at a time when merger synergy benefits and recurring revenue growth remain closely watched by the broader market.

Explore 2 other fair value estimates on JBT Marel - why the stock might be worth as much as 27% more than the current price!

Build Your Own JBT Marel Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your JBT Marel research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free JBT Marel research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate JBT Marel's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:JBTM

JBT Marel

Provides technology solutions to food and beverage industry in North America, Europe, the Middle East, Africa, the Asia Pacific, and Central and South America.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative