Advertisement

- United States

- /

- Machinery

- /

- NYSE:ITT

A Fresh Look at ITT (ITT) Valuation After Major Saudi Expansion Boosts Regional Capacity

Simply Wall St

Reviewed by Simply Wall St

ITT (ITT) just wrapped up the second phase of a $25 million expansion at its Dammam, Saudi Arabia facility, doubling production capacity. This move puts the company in a stronger position to meet fast-growing demand in the region.

See our latest analysis for ITT.

ITT’s steady expansion in the Middle East comes against a year marked by strong momentum for the stock. It boasts a 29.85% year-to-date share price return and an 18.78% total shareholder return over the past twelve months, outpacing many industrial peers. Long-term holders have seen even more impressive gains, with a three-year total shareholder return topping 120%, signaling solid growth potential and steady execution alongside recent wins such as the Dammam facility ramp-up.

If this kind of compounding performance has your attention, it could be the perfect time to explore other fast-growing stocks with high levels of insider confidence. Discover fast growing stocks with high insider ownership

With so much momentum and ambitious growth targets, the question for investors now is whether ITT’s strong fundamentals and future prospects are already reflected in its share price or if there is still room for upside ahead.

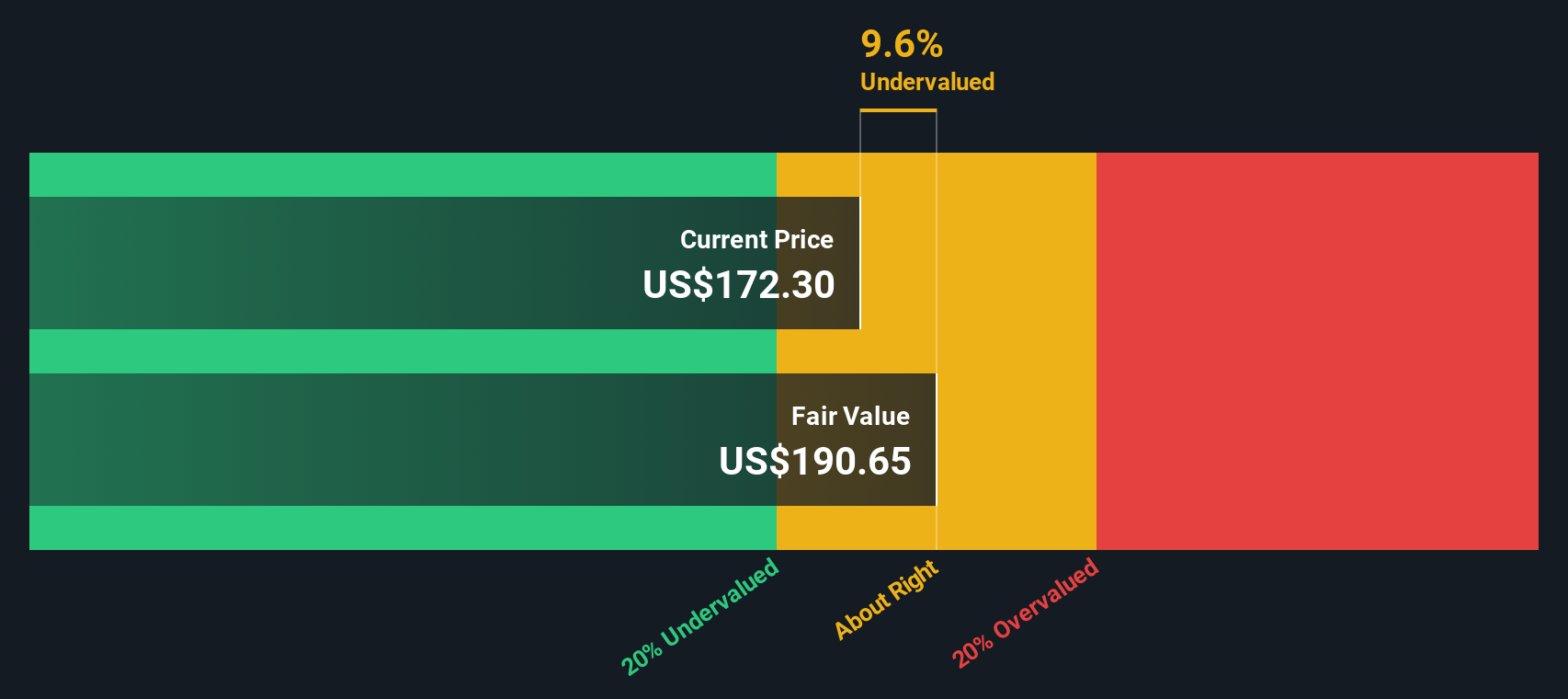

Most Popular Narrative: 11.8% Undervalued

With ITT shares last closing at $184.16 and the fair value from the most widely followed market narrative set at $208.91, there is a notable gap between the current price and what is considered justified for its growth trajectory.

Expansion of high-margin aftermarket and services business, along with new technologies (geopolymer brake pads, advanced fuel pumps, digital monitoring), positions ITT to benefit from industry digitalization and energy efficiency standards. This supports margin expansion and stable, recurring earnings streams.

What is the secret behind this bullish outlook? Analysts are focusing on aggressive margin gains and a shift in business mix to spark earnings momentum. Want to know which high-impact projections put ITT’s future profit power in a league of its own? The assumptions inside this fair value might surprise you.

Result: Fair Value of $208.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks such as project delays and increased integration costs from acquisitions could limit ITT’s margin gains if market conditions shift unexpectedly.

Find out about the key risks to this ITT narrative.

Another View: SWS DCF Model Suggests a Cautious Stance

The widely used SWS DCF model estimates ITT’s fair value at $162.92, which is notably below the current share price of $184.16. This approach signals ITT may be overvalued when factoring in projected cash flows and discount rates. Which method best reflects ITT’s true potential: analyst consensus or a stricter cash-flow perspective?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ITT for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ITT Narrative

If you want to look at the numbers differently or put your own spin on ITT’s story, it only takes a few minutes to shape your own perspective. Do it your way

A great starting point for your ITT research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let standout opportunities slip past you. Simply Wall Street makes it easy to spot stocks with unique advantages and impressive momentum. Get ahead by using these hand-picked screeners:

- Tap into the growth potential of fast-moving innovation by checking out these 25 AI penny stocks setting the pace in artificial intelligence.

- Boost your portfolio’s income with these 15 dividend stocks with yields > 3% that consistently deliver yields above 3% and offer stability in unpredictable markets.

- Catch undervalued gems early and unlock upside before the crowd with these 920 undervalued stocks based on cash flows based on rigorous cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ITT

ITT

Manufactures and sells engineered critical components and customized technology solutions for the transportation, industrial, and energy markets.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative