Advertisement

- United States

- /

- Construction

- /

- NYSE:FIX

How Record Backlog Growth and CEO Share Sale Could Shape Comfort Systems USA (FIX) Investor Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 24, 2025, Brian E. Lane, President and CEO of Comfort Systems USA, sold 7,158 shares after the company delivered third-quarter results that surpassed both earnings and revenue forecasts.

- Analyst sentiment shifted as UBS revised its outlook on Comfort Systems USA, highlighting strong quarterly performance and robust backlog growth as key factors supporting the company’s outlook.

- To understand the implications for investors, we’ll consider how the record growth in backlog enhances Comfort Systems USA’s future revenue visibility.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Comfort Systems USA Investment Narrative Recap

To be a shareholder in Comfort Systems USA, you likely believe in the ongoing demand for complex mechanical and electrical projects, underpinned by the company’s record project backlog and expanding presence in technology and healthcare construction. While the CEO’s recent share sale and strong Q3 results grabbed attention, neither event materially changes the stock’s key short-term catalyst, execution of its sizable order book, or its biggest risk, which remains heavy exposure to potential cyclical slowdowns in technology-driven construction.

Among recent company announcements, the Q3 2025 earnings report is most relevant, revealing revenue of US$2,450.97 million and net income of US$291.62 million, both significant year-over-year increases. This robust financial performance directly supports analysts’ focus on backlog growth as a driver of future results, but adds context to the ongoing risk of sector concentration, especially with so much of the backlog tied to technology projects.

By contrast, investors should also be aware that if construction demand in the data center and tech sectors slows suddenly...

Read the full narrative on Comfort Systems USA (it's free!)

Comfort Systems USA's outlook anticipates $10.5 billion in revenue and $1.3 billion in earnings by 2028. This is based on a forecasted annual revenue growth rate of 10.9% and nearly doubling earnings, an increase of $607.8 million from the current $692.2 million earnings.

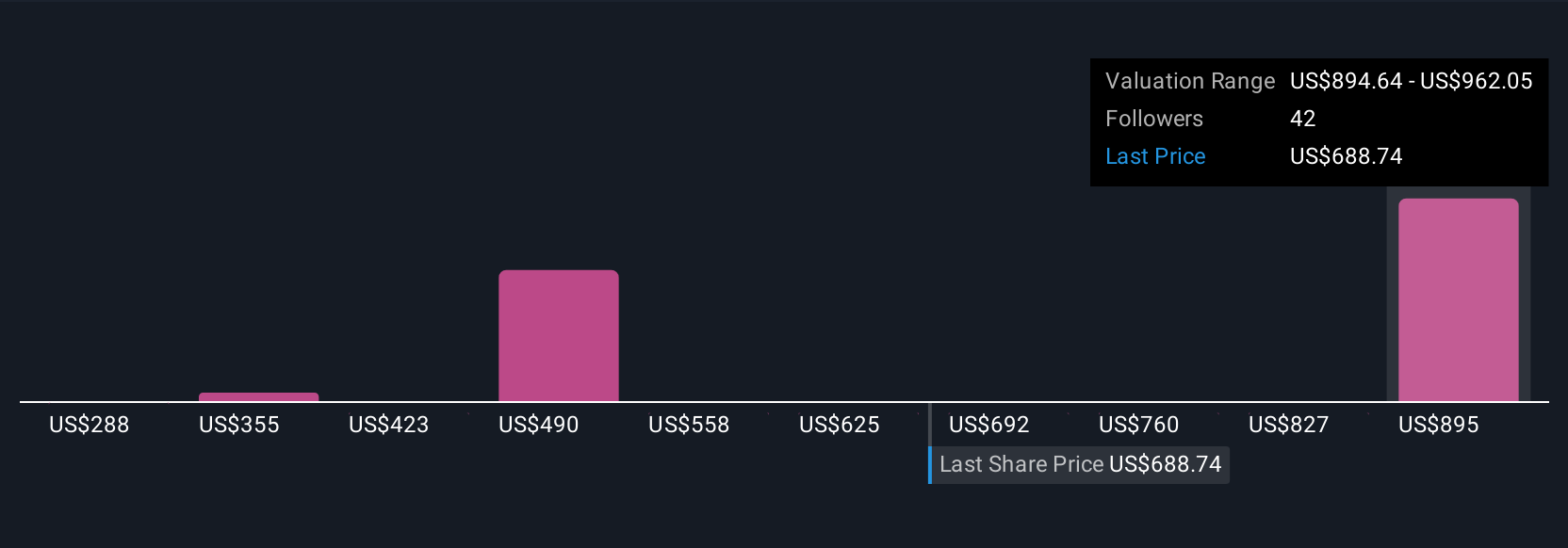

Uncover how Comfort Systems USA's forecasts yield a $1133 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members produced 11 fair value estimates for Comfort Systems USA, ranging from US$287.88 to US$1,476.42 per share. While many highlight strong execution and a record backlog as a catalyst, risk remains around the company’s revenue concentration in technology sectors, urging you to review a range of opinions on future performance.

Explore 11 other fair value estimates on Comfort Systems USA - why the stock might be worth less than half the current price!

Build Your Own Comfort Systems USA Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Comfort Systems USA research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Comfort Systems USA research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Comfort Systems USA's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FIX

Comfort Systems USA

Provides mechanical and electrical installation, renovation, maintenance, repair, and replacement services for the mechanical and electrical services industry in the United States.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative