Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:BWXT

Is BWXT’s Share Price Still Justified After Recent 63% Surge and Strong Earnings?

Simply Wall St

Reviewed by Simply Wall St

If you are sitting on the fence about what to do with BWX Technologies stock right now, you are definitely not alone. With its impressive run over the last year, climbing more than 63%, BWXT has landed squarely on the radar for many investors searching for growth stories and stable plays alike. The stock’s gains are even more eye-catching when you zoom out, doubling over the last three and five years, and surging more than 51% in just the past three months. These outsized returns tell a story that is hard to ignore and have prompted a lot of questions about whether there is still room to grow or if the price has raced too far ahead of the fundamentals.

Recent enthusiasm around the defense sector, and BWX Technologies’ positioning in specialized nuclear solutions, has fueled that momentum. At the same time, the company’s most recent annual results showed healthy revenue growth of nearly 8.8% and net income up by more than 13%, giving further credibility to its run. Despite this, when we turn to a numbers-based valuation analysis, BWXT’s current value score—a 0 out of 6, with points earned for each standard check of undervaluation—raises questions about whether the stock is actually cheap at these levels.

Now that you have the story behind those recent price surges and the headline valuation score, let’s walk through how BWX Technologies stacks up against classic valuation frameworks. I will also share a perspective that goes beyond the usual checks, so read on if you are after a deeper understanding of BWXT’s value potential.

BWX Technologies delivered 63.9% returns over the last year. See how this stacks up to the rest of the Aerospace & Defense industry.Approach 1: BWX Technologies Cash Flows

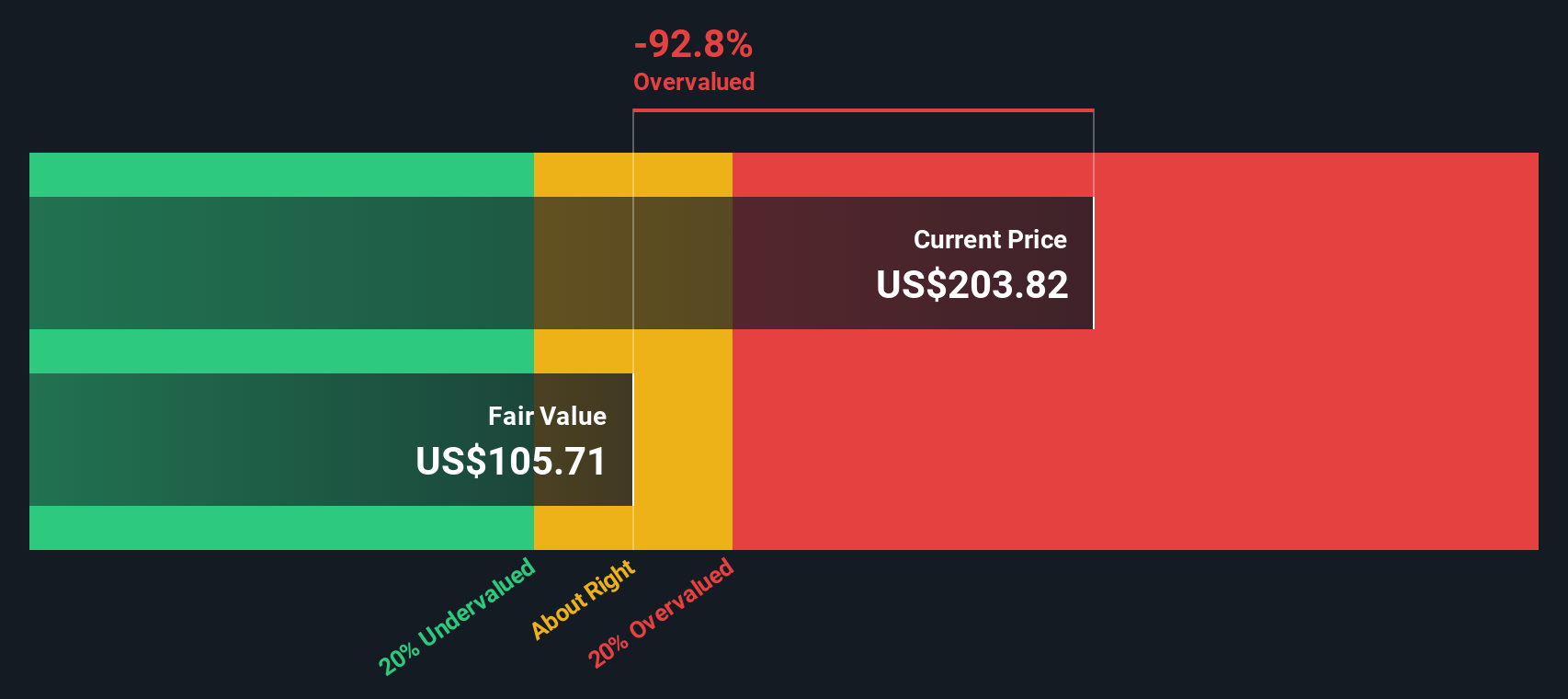

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future free cash flows and then discounting those figures back to today’s dollars. This approach provides an intrinsic value that helps investors decide if a stock appears attractive at current prices.

For BWX Technologies, the latest trailing twelve months generated free cash flow of $344.85 million. Analyses project steady growth in free cash flow over the coming decade, with 2028’s forecast at $418.05 million and estimates reaching $679.81 million by 2035. These projections use a two-stage method, factoring in expected growth rates that gradually slow over time.

Based on these trends, the DCF calculation estimates an intrinsic value of $113.02 per share. However, when compared to the current market price, this valuation suggests BWX Technologies is 44.7% overvalued. In other words, the anticipated cash flows do not fully support today’s higher share price, according to this model.

Result: OVERVALUED

Approach 2: BWX Technologies Price vs Earnings (P/E)

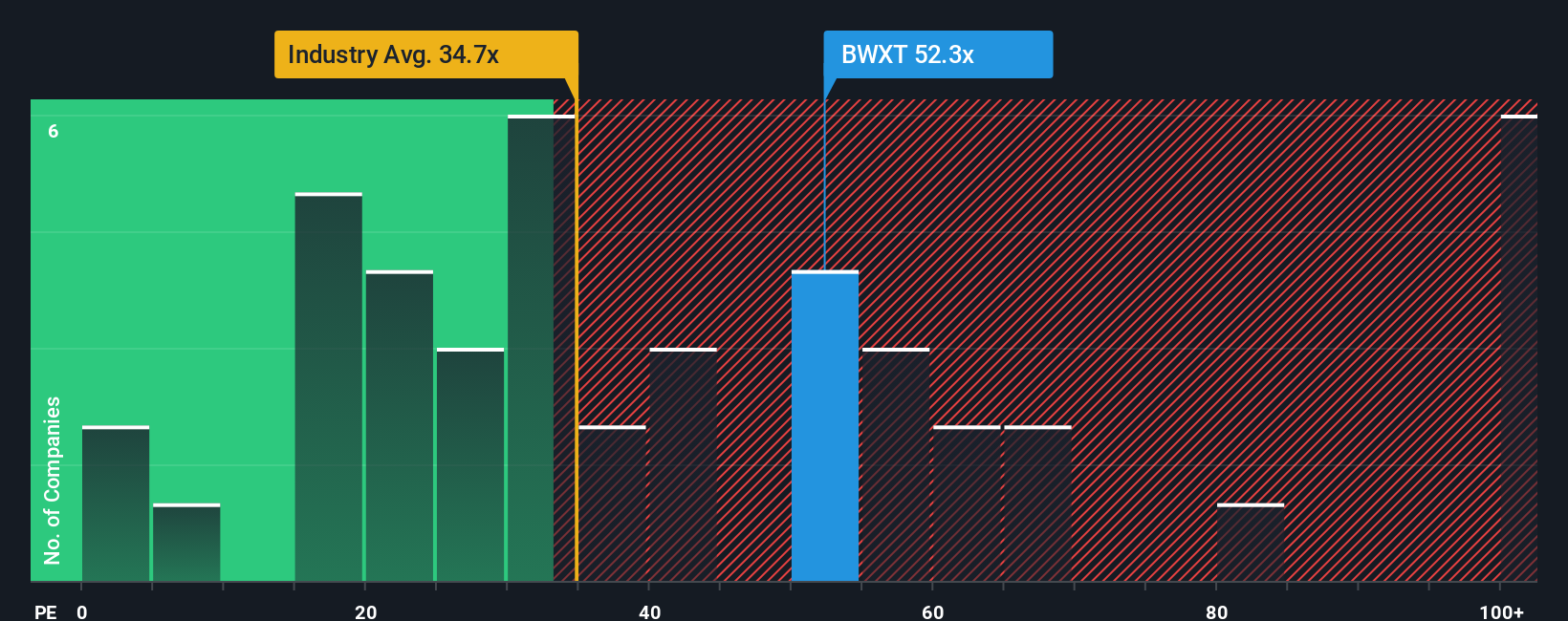

The price-to-earnings (P/E) ratio is a commonly used valuation metric for profitable businesses, providing a quick way to assess how much investors are willing to pay for each dollar of earnings. This metric is especially relevant for BWX Technologies, which continues to generate solid profits, making the P/E ratio useful for peer and industry comparisons.

What counts as a “normal” or “fair” P/E ratio generally depends on a company’s growth outlook and risk profile. Rapidly growing or lower-risk companies often justify a higher P/E, while mature or riskier firms tend to trade at lower multiples. For BWX Technologies, the current P/E is 50.8x, which is notably higher than both the peer average of 34.8x and the Aerospace & Defense industry average of 33.7x. This elevated P/E suggests strong investor optimism regarding future growth prospects.

Simply Wall St’s Fair Ratio for BWXT is 28.5x, a tailored benchmark based on the company’s actual growth, profitability, industry context, and risk. Since the current P/E is well above this fair level, the stock appears to reflect a high degree of optimism, indicating limited value at today’s level.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your BWX Technologies Narrative

Introducing Narratives, a simple yet powerful investment tool that lets you create your own story about BWX Technologies. This tool connects what you believe about its future growth, earnings, and margins to what you think the company is actually worth.

Rather than just relying on static numbers or ratios, a Narrative helps you translate your view of the company’s prospects, such as strong defense contracts or nuclear demand, into a future-focused financial forecast and then to an up-to-date fair value.

Narratives are easy for anyone to use through the Simply Wall St platform and its global community. They make investment decisions more accessible, letting you check and shape the outlook as new earnings, news, or surprises emerge.

This approach allows you to quickly see whether it makes sense to buy or sell by comparing your Narrative's fair value with the current share price. Because Narratives update instantly when new data arrives, your decision is always informed by the latest facts.

For example, some investors might believe BWX Technologies should be priced near $250, based on aggressive defense expansion and nuclear innovation. Others might set fair value closer to $120 if they see real risks in future government spending or commercial volatility.

Do you think there's more to the story for BWX Technologies? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BWX Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BWXT

BWX Technologies

Manufactures and sells nuclear components in the United States, Canada, and internationally.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative