Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:BA

Is NASA’s Starliner Mission Cut Reshaping the Investment Case for Boeing (BA)?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, NASA announced it had reduced its contract with Boeing for the Starliner space capsule, cutting planned missions to the International Space Station from six to four due to technical and safety concerns after a problematic prior test flight. This adjustment limits future spaceflight opportunities for Boeing and signals ongoing scrutiny of its space program reliability.

- This shift highlights how program setbacks can influence investor confidence by narrowing Boeing’s potential for growth within the space segment.

- We'll examine how the reduction in NASA Starliner missions impacts Boeing’s long-term space growth outlook and risk profile.

Find companies with promising cash flow potential yet trading below their fair value.

Boeing Investment Narrative Recap

Boeing shareholders are often anchored by confidence in the company’s ability to restore production momentum and profitability, largely driven by commercial aircraft demand and operational improvements in its supply chain. The recent cut to NASA’s Starliner contract does not materially affect Boeing's most important short-term catalyst, which remains the ramp-up of 737 and 787 deliveries; however, it adds incremental risk to perceptions of execution reliability across its segments, a sensitive area given recent program delays and reputational challenges.

Among recent announcements, Emirates’ expanded order for 65 additional 777X jets stands out, reinforcing the critical role that recovery in commercial aircraft production and backlog conversion plays in Boeing’s near-term earnings trajectory and broader growth opportunities, particularly as defense and space revenues fluctuate.

By contrast, what some investors may miss is how Boeing’s ongoing quality and certification challenges across flagship models could still...

Read the full narrative on Boeing (it's free!)

Boeing's narrative projects $114.4 billion in revenue and $7.1 billion in earnings by 2028. This requires 14.9% yearly revenue growth and an $18 billion earnings increase from the current earnings of -$10.9 billion.

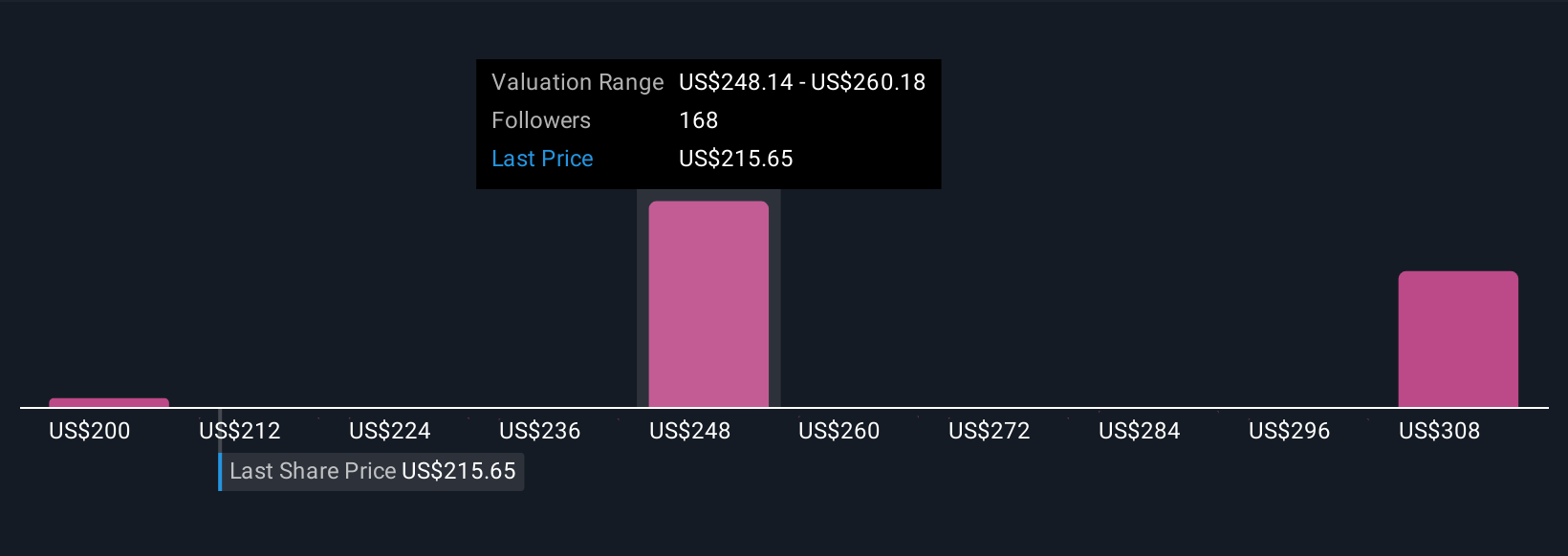

Uncover how Boeing's forecasts yield a $249.32 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members set fair values for Boeing between US$206.79 and US$352.81, based on 19 different analyses. Against this backdrop of wide-ranging views, certification and quality risks remain a key issue that could reshape Boeing’s future performance; consider how your expectations compare before making a call.

Explore 19 other fair value estimates on Boeing - why the stock might be worth just $206.79!

Build Your Own Boeing Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boeing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BA

Boeing

Designs, develops, manufactures, sells, services, and supports commercial jetliners, military aircraft, satellites, missile defense, human space flight and launch systems, and services worldwide.

Very undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

100 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative