- United States

- /

- Construction

- /

- NYSE:AGX

Analysts Are More Bearish On Argan, Inc. (NYSE:AGX) Than They Used To Be

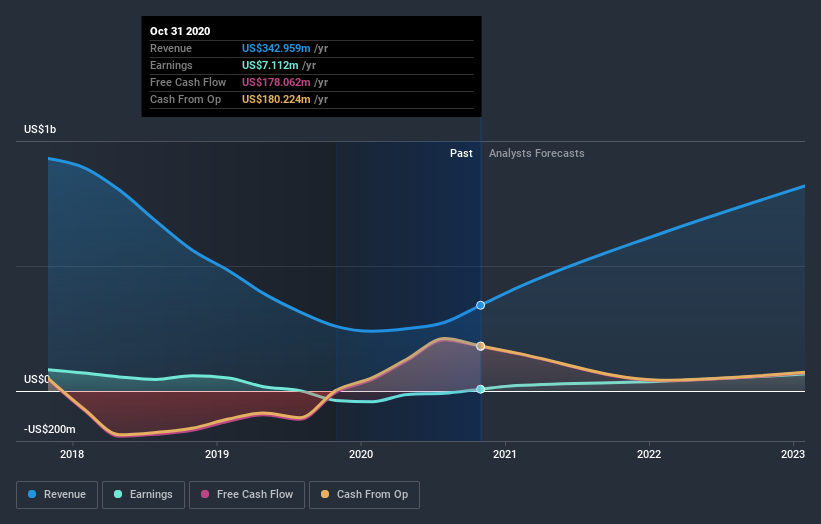

The analysts covering Argan, Inc. (NYSE:AGX) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for next year. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

After this downgrade, Argan's two analysts are now forecasting revenues of US$630m in 2022. This would be a sizeable 84% improvement in sales compared to the last 12 months. Per-share earnings are expected to leap 435% to US$2.43. Previously, the analysts had been modelling revenues of US$783m and earnings per share (EPS) of US$3.89 in 2022. Indeed, we can see that the analysts are a lot more bearish about Argan's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for Argan

Despite the cuts to forecast earnings, there was no real change to the US$60.50 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Argan, with the most bullish analyst valuing it at US$61.00 and the most bearish at US$60.00 per share. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that the analysts have a clear view on its prospects.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. For example, we noticed that Argan's rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 84%, well above its historical decline of 13% a year over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 5.7% next year. Not only are Argan's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Argan. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected next year, we wouldn't be surprised if investors were a bit wary of Argan.

Uncomfortably, our automated valuation tool also suggests that Argan stock could be overvalued following the downgrade. Shareholders could be left disappointed if these estimates play out. You can learn more about our valuation methodology for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Argan, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:AGX

Argan

Through its subsidiaries, provides engineering, procurement, construction, commissioning, maintenance, project development, and technical consulting services to the power generation market.

Flawless balance sheet with reasonable growth potential and pays a dividend.