Advertisement

- United States

- /

- Construction

- /

- NYSE:ACM

How AECOM's (ACM) Construction Management Review and Dividend Boost Could Reshape Its Growth Narrative

Simply Wall St

Reviewed by Sasha Jovanovic

- In November 2025, AECOM announced it is reviewing strategic alternatives for its Construction Management business while approving a 19% increase in its quarterly dividend to US$0.31 per share, with double-digit dividend growth targets through 2029.

- The company’s focus on higher-growth segments like AI and Advisory services, alongside a significant dividend increase, points to an emphasis on shareholder returns and business transformation.

- We’ll explore how AECOM’s review of its Construction Management division could shape its future investment narrative and growth strategy.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

AECOM Investment Narrative Recap

To own AECOM, an investor must believe in the company’s ability to execute its pivot toward higher-returning sectors like AI and Advisory, balancing long-term growth potential against execution and market risks. The review of strategic alternatives for its Construction Management business directly addresses this shift, although the most important short-term catalyst, winning and retaining high-margin contracts in Advisory and digital solutions, remains largely unaffected. The biggest risk continues to be exposure to public sector spending cycles; this news does not materially change that risk profile.

Among recent announcements, the company’s new double-digit dividend growth targets through 2029 stand out as especially relevant. This commitment to returning cash to shareholders is strongly linked to the strategic focus underlying the Construction Management review, reinforcing AECOM’s emphasis on optimizing capital allocation even while transforming its business mix to support future catalysts.

However, investors should also be aware of the mounting threat from emerging digital competitors, as the accelerating adoption of AI and data-driven technologies could...

Read the full narrative on AECOM (it's free!)

AECOM's narrative projects $18.8 billion revenue and $955.0 million earnings by 2028. This requires 5.4% yearly revenue growth and a $280.3 million earnings increase from $674.7 million.

Uncover how AECOM's forecasts yield a $143.42 fair value, a 39% upside to its current price.

Exploring Other Perspectives

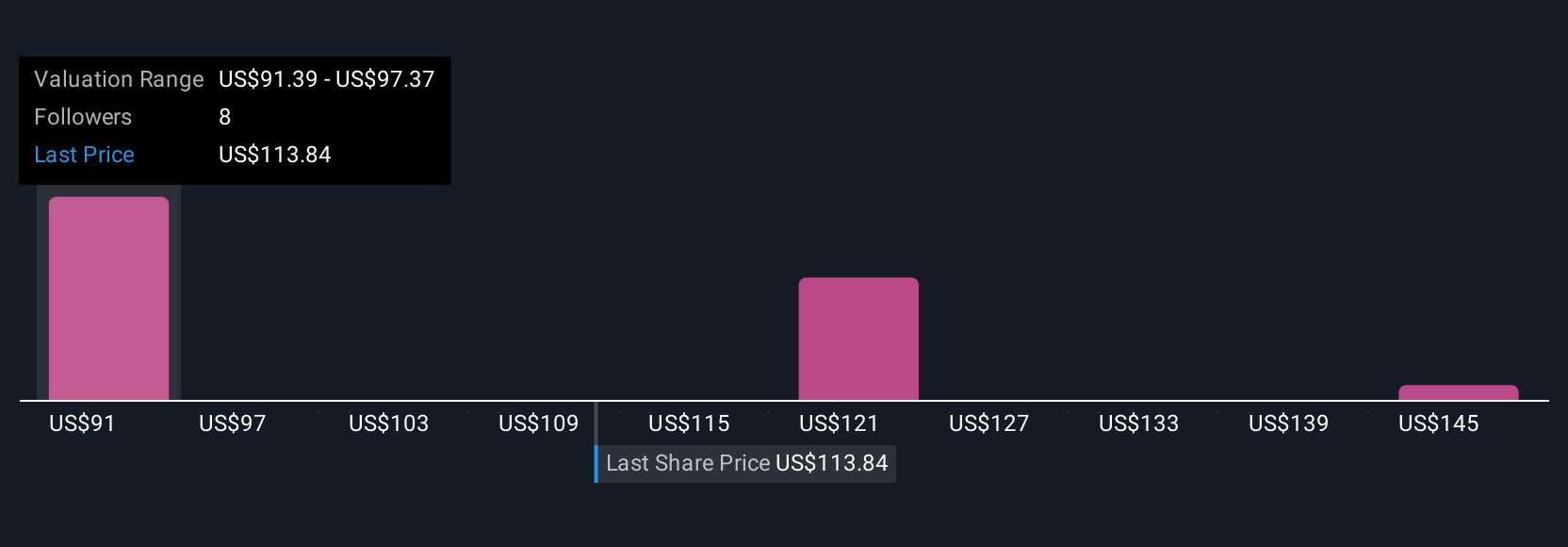

Simply Wall St Community members set fair value estimates for AECOM between US$84 and US$151, based on four distinct forecasts. While the company’s emphasis on Advisory and digital growth supports longer-term optimism, opinions remain widely split and highlight potential challenges linked to technological disruption and competition.

Explore 4 other fair value estimates on AECOM - why the stock might be worth 18% less than the current price!

Build Your Own AECOM Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your AECOM research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free AECOM research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate AECOM's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ACM

AECOM

Provides professional infrastructure consulting services for governments, businesses, and organizations internationally.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative