Advertisement

- United States

- /

- Electrical

- /

- NasdaqGS:FLNC

Fluence Energy (FLNC): Is Record Order Backlog Fueling a Valuation Disconnect After Latest Quarterly Highlights?

Simply Wall St

Reviewed by Simply Wall St

Fluence Energy (FLNC) delivered a record $1.4 billion in new orders last quarter, which lifted its backlog to $5.3 billion. This positions the company for strong revenue growth in 2026, even after missing Wall Street expectations.

See our latest analysis for Fluence Energy.

After a volatile few months, Fluence Energy’s share price has rebounded with real momentum, jumping 27.5% over the last week and delivering a striking 165% return over the past 90 days. While the one-year total shareholder return stands at just 4.4%, recent analyst upgrades and a record backlog are fueling a wave of optimism heading into 2026.

If you’re watching the pace of change in the renewables space, it’s a great time to broaden your perspective and discover fast growing stocks with high insider ownership

With shares rallying on strong order wins and 2026 guidance, the real question is whether Fluence Energy remains undervalued at these levels or if the market is already factoring in all of next year’s growth potential.

Most Popular Narrative: 71% Overvalued

The current narrative assigns Fluence Energy a fair value far below its last close of $19.64, indicating that the market has moved well ahead of underlying expectations. This creates a clear tension between how analyst models are projecting the next stage for valuation.

Rapid global electrification and surging power demand, driven by data centers, transportation, and industrial sectors, are expected to sharply increase the need for grid resilience and flexibility. This may lead to substantial projected growth for large-scale battery storage, and could drive material revenue growth for Fluence over the next several years.

Which assumptions are powering this dramatic divergence from the current share price? The primary drivers and missing pieces are in the narrative’s bold bets on future earnings, margin improvements, and sector-wide adoption. The key question is whether this outlook holds up to scrutiny, or whether something significant is being overlooked.

Result: Fair Value of $11.47 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent tariff uncertainties and ongoing competition from international battery suppliers could present challenges to Fluence Energy’s growth expectations in the coming quarters.

Find out about the key risks to this Fluence Energy narrative.

Another View: Contrasting the Multiples Approach

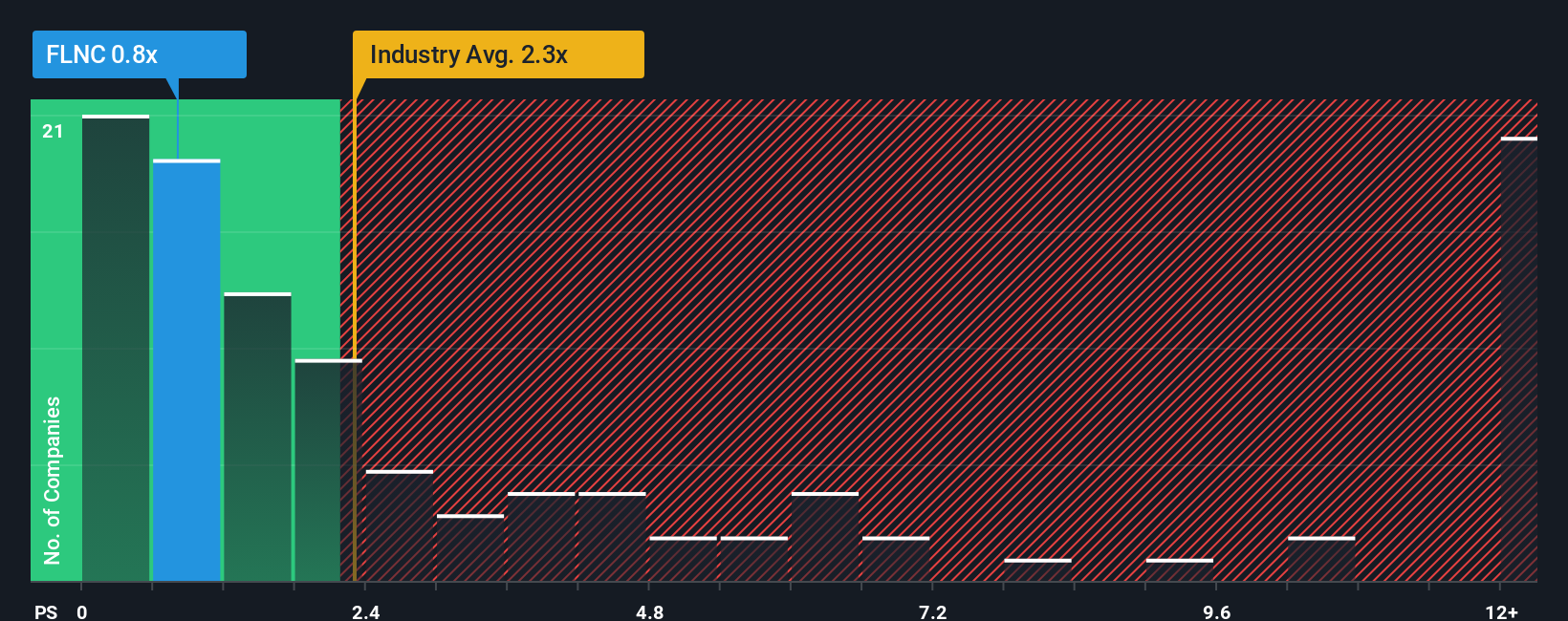

While the market currently sees Fluence Energy as overvalued based on analyst targets, looking at its price-to-sales ratio tells a very different story. At 1.1x, Fluence is trading far below the US Electrical industry average of 2x and the peer group average of 23.4x, suggesting relative value. If the market moves closer to the fair ratio of 2.2x, investors could see meaningful upside. However, with such a large valuation gap, this could be an overlooked opportunity or a sign of risk.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fluence Energy Narrative

If this perspective does not fit with your outlook, or you would prefer to analyze the numbers and form your own conclusions, you can craft a custom narrative in just a few minutes. Do it your way.

A great starting point for your Fluence Energy research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Unlock fresh opportunities in today’s market by checking out these powerful tools. Get ahead of the curve and make sure you are not missing out on tomorrow’s biggest winners.

- Start earning more from your portfolio by tapping into steady income with these 15 dividend stocks with yields > 3% which offers attractive yields above 3%.

- Accelerate your strategy by targeting market leaders in artificial intelligence using these 25 AI penny stocks to spot the next wave of innovation.

- Maximize potential returns with a search for undervalued gems through these 920 undervalued stocks based on cash flows based on proven cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FLNC

Fluence Energy

Through its subsidiaries, provides energy storage and optimization software for renewables and storage applications in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative