Advertisement

- United States

- /

- Banks

- /

- NYSE:WFC

Wells Fargo (WFC): Assessing Valuation After Asset Cap Removal Unlocks Growth Potential

Simply Wall St

Reviewed by Simply Wall St

Wells Fargo (WFC) has been making headlines after the lifting of its asset cap in June 2025. This move unlocks new growth opportunities for the bank’s deposit and loan businesses in today’s friendlier interest rate environment.

See our latest analysis for Wells Fargo.

Momentum has been building for Wells Fargo, with optimism around the recent asset cap lift and leadership changes helping lift sentiment. The 22.3% year-to-date share price return reflects renewed confidence in its growth outlook, while the 102% three-year total shareholder return highlights impressive longer-term value creation.

If Wells Fargo's growth story has caught your attention, this could be the perfect moment to discover fast growing stocks with high insider ownership.

But with shares up over 22% this year and optimism running high, the key question for investors is whether Wells Fargo has further room to run, or if the market has already priced in its next chapter of growth.

Most Popular Narrative: 8.2% Undervalued

Wells Fargo’s last close at $85.85 sits below the most-followed narrative’s fair value estimate of $93.54. This suggests notable upside potential if its projections hold true. Beneath the headline number are bold expectations for growth and profitability, shaped by recent regulatory shifts and an optimistic medium-term outlook.

The removal of the asset cap and resolution of multiple regulatory orders unlocks Wells Fargo's ability to aggressively grow its balance sheet, including deposits, loans, and trading assets, after years of constraint. This may result in higher revenue and earnings growth over the coming quarters and years.

Curious what powers this bullish price target? The narrative points to major changes, including regulatory victories, new digital initiatives, and increasing competition. These factors have contributed to a set of numbers analysts rarely agree on. Which bold assumptions and moving parts justify this higher valuation? Dive in to see the surprising projections behind the headline figure.

Result: Fair Value of $93.54 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent regulatory costs and accelerating digital competition could still threaten Wells Fargo's ability to meet its ambitious growth and margin targets.

Find out about the key risks to this Wells Fargo narrative.

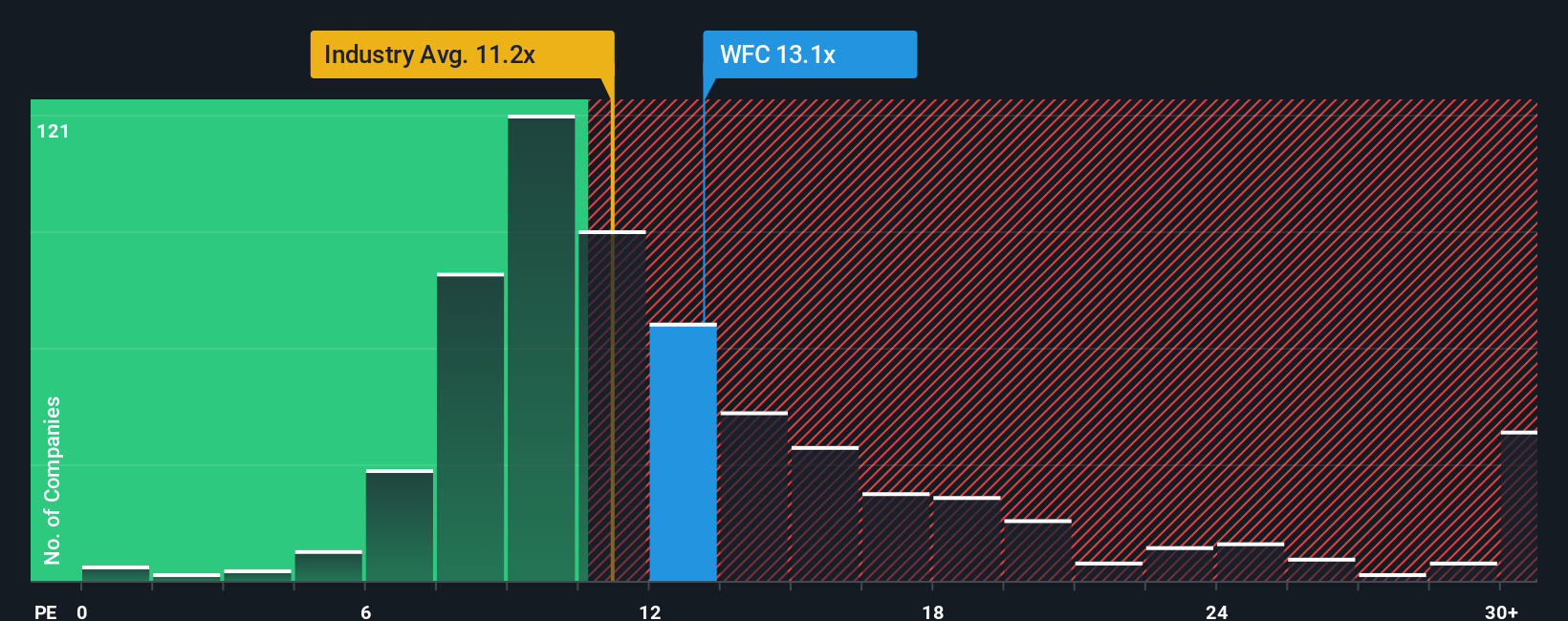

Another View: Multiples Tell a Less Optimistic Story

While our fair value estimate suggests Wells Fargo is undervalued, a look at its price-to-earnings ratio offers a contrasting perspective. Wells Fargo trades at 13.5 times earnings, which is higher than both its industry's average of 11.4 and its peers' 12.8. The fair ratio for Wells Fargo is estimated at 14.1, indicating that current valuations are already approaching where the market believes it should be. With little gap left, is the opportunity as big as it looks?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Wells Fargo Narrative

If you see things differently or want to challenge the numbers, it only takes a few minutes to dive into the details and shape your own perspective. Do it your way.

A great starting point for your Wells Fargo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don't miss your chance to spot hidden gems and build a smarter portfolio. Use these top investment ideas to get ahead and make confident moves in today’s market.

- Unlock the potential of fast-growing companies by checking out these 920 undervalued stocks based on cash flows before the market catches on.

- Tap into passive income possibilities and steady returns by reviewing these 15 dividend stocks with yields > 3% with high yields.

- Secure your stake in cutting-edge healthcare innovation by browsing these 30 healthcare AI stocks which is driving advancements in medical technology and AI.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wells Fargo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WFC

Wells Fargo

A financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative