Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:UWMC

Analysts' Revenue Estimates For UWM Holdings Corporation (NYSE:UWMC) Are Surging Higher

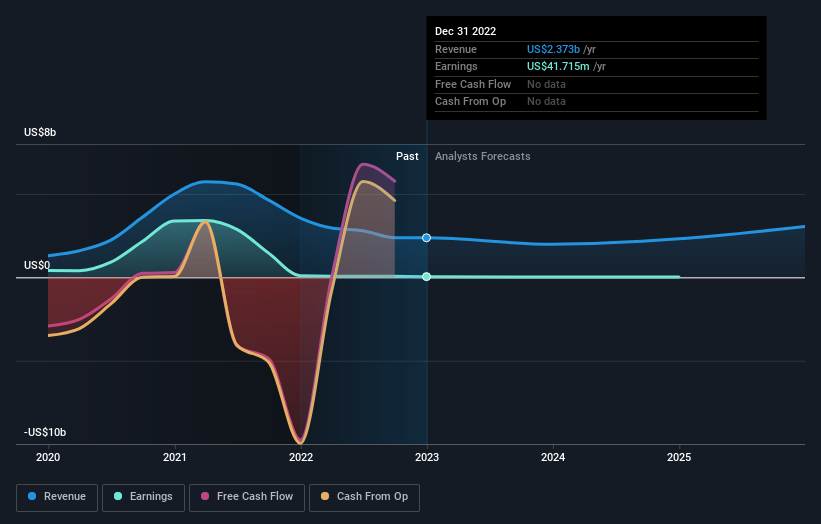

Shareholders in UWM Holdings Corporation (NYSE:UWMC) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. The market may be pricing in some blue sky too, with the share price gaining 15% to US$4.80 in the last 7 days. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

Following the latest upgrade, the seven analysts covering UWM Holdings provided consensus estimates of US$2.0b revenue in 2023, which would reflect a considerable 16% decline on its sales over the past 12 months. Statutory earnings per share are supposed to nosedive 43% to US$0.26 in the same period. Prior to this update, the analysts had been forecasting revenues of US$1.8b and earnings per share (EPS) of US$0.25 in 2023. The forecasts seem more optimistic now, with a nice increase in revenue and a small lift in earnings per share estimates.

Check out our latest analysis for UWM Holdings

With these upgrades, we're not surprised to see that the analysts have lifted their price target 14% to US$4.03 per share. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic UWM Holdings analyst has a price target of US$5.50 per share, while the most pessimistic values it at US$3.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 16% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 20% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 7.2% per year. It's pretty clear that UWM Holdings' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at UWM Holdings.

Analysts are clearly in love with UWM Holdings at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as its declining profit margins. You can learn more, and discover the 2 other concerns we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:UWMC

UWM Holdings

Engages in the origination, sale, and servicing residential mortgage lending in the United States.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor