Advertisement

- United States

- /

- Auto Components

- /

- NYSE:MOD

Assessing Modine Manufacturing After Shares Surge 11% on Strategic Partnerships

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Modine Manufacturing’s incredible run could still be a great opportunity, or if the share price has already raced ahead of its true value? You’re not alone, and the numbers here are worth a closer look.

- The stock just jumped 11.1% this week, pushing its year-to-date gains to an impressive 36.8% and stretching its three-year return to an eye-popping 649.2%.

- Investor interest has surged after Modine Manufacturing announced new strategic partnerships focused on sustainable thermal management, as well as a recent contract win with a leading EV manufacturer. This has fueled optimism about its long-term growth potential.

- According to our checks, Modine scores just 2 out of 6 on key undervaluation metrics. This suggests there is more to this valuation story than meets the eye. Let’s break down the main ways investors gauge value. Stay tuned, because there is an even smarter way to analyze the stock coming up at the end.

Modine Manufacturing scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Modine Manufacturing Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model helps estimate a company's intrinsic value by forecasting its future cash flows and discounting them back to their present value. This approach is widely used because it provides a grounded assessment based on the company’s ability to generate cash in the years ahead.

For Modine Manufacturing, the most recent Free Cash Flow stands at $53.04 million. Analysts provide detailed projections for the next five years. For longer periods, Simply Wall St extends the forecast based on growth trends. By 2028, Free Cash Flow is anticipated to reach $362.4 million, and the model continues this projection out to 2035.

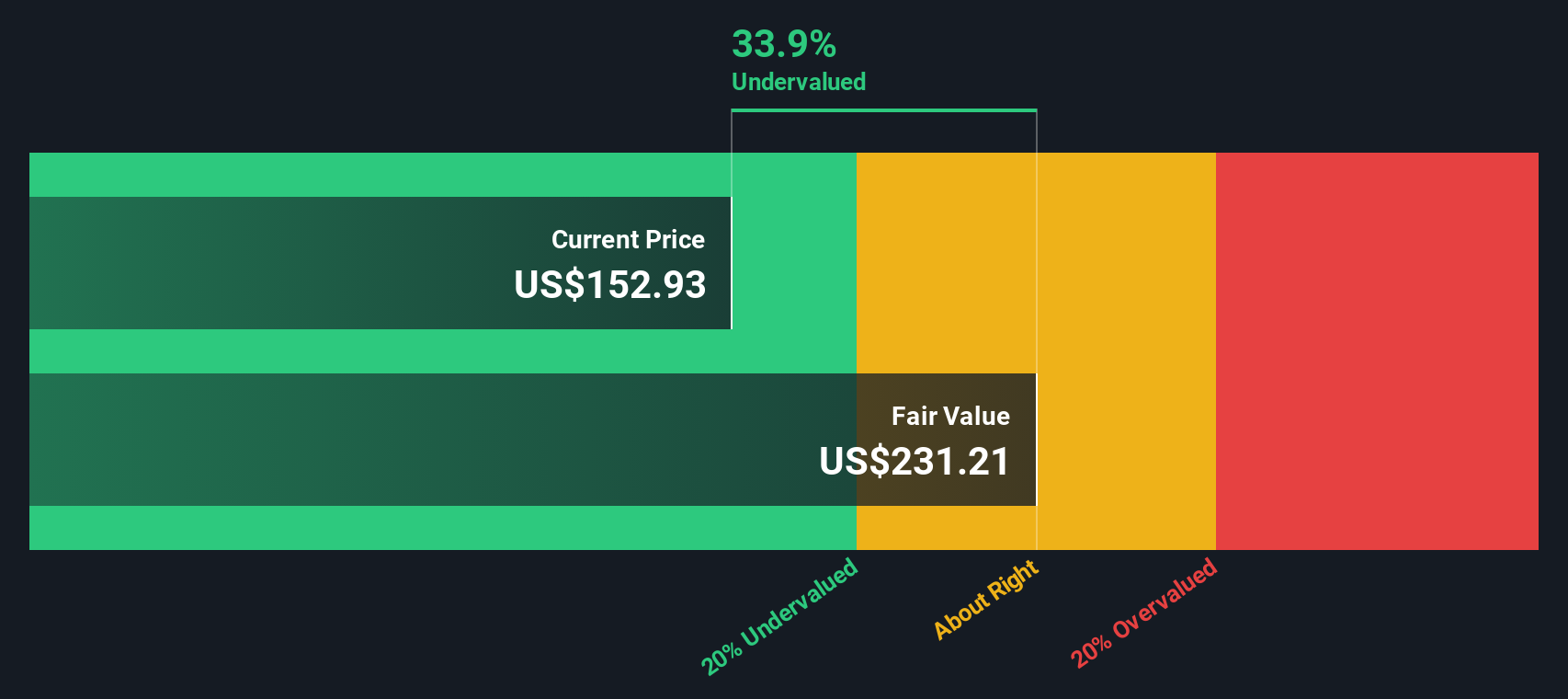

Using these projections, the DCF model estimates Modine’s intrinsic value at $217.43 per share. Compared to the current market price, this figure suggests the stock is trading at a 26.9% discount. In other words, the market may be undervaluing Modine’s future earnings potential based on these cash flow estimates.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Modine Manufacturing is undervalued by 26.9%. Track this in your watchlist or portfolio, or discover 922 more undervalued stocks based on cash flows.

Approach 2: Modine Manufacturing Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a widely used valuation benchmark for profitable companies like Modine Manufacturing. It tells investors how much they are paying for each dollar of earnings, making it particularly useful for stocks with consistent profitability.

Growth expectations and perceived risk play a big role in determining what constitutes a "fair" PE ratio for a company. Higher future growth or less risk will generally justify a higher PE, while slower growth or elevated risks result in lower norms.

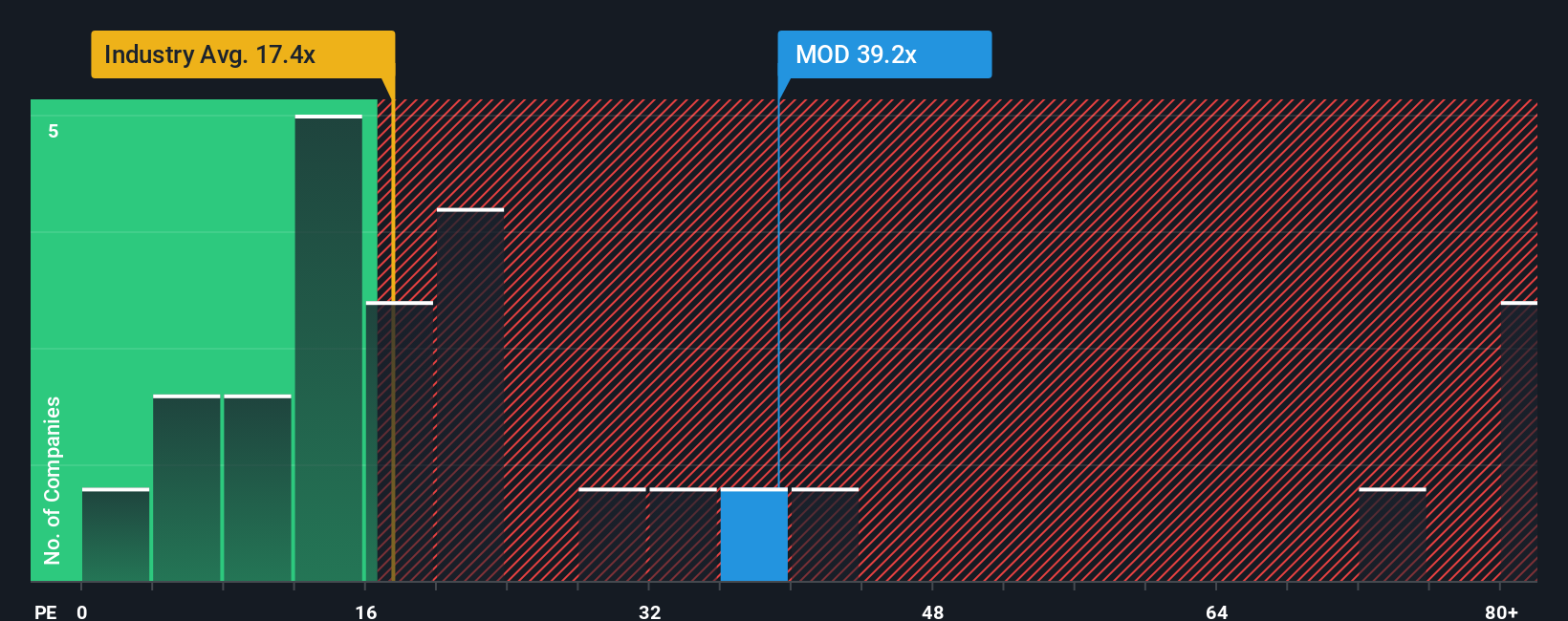

Currently, Modine Manufacturing trades at a PE ratio of 44.95x. This is well above the auto components industry average of 21.24x and also outpaces its peers, which average 26.37x. At first glance, the stock looks expensive compared to those benchmarks.

However, Simply Wall St’s proprietary “Fair Ratio” is calculated as 30.87x. This figure is determined by weighing the company’s specific earnings growth outlook, profit margins, industry position, company size, and risk factors. Relying solely on industry averages or peer comparisons can overlook these important details. The Fair Ratio provides a more custom-fit guide for fair valuation.

Since Modine’s actual PE is significantly higher than its Fair Ratio, the shares may be pricing in more optimism than justified by its fundamentals.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Modine Manufacturing Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your point of view about a company, connecting the story you believe in with your own expectations for its future revenue, earnings, and margins, which then flows through to your personal fair value calculation.

Narratives bring together everything you know about a business, whether it is a breakthrough in data center cooling, new customer wins, or operational challenges, tying the company’s story directly to a dynamic financial forecast and the fair value estimate that comes out of it.

On Simply Wall St’s Community page, millions of investors can easily create, share, and compare Narratives for companies like Modine Manufacturing. They help you make smarter decisions about when to buy or sell by showing how your Fair Value compares to the current Price. In addition, Narratives automatically update every time important news or earnings are released.

For example, some investors see surging demand for Modine’s data center cooling and set a higher fair value, while others focus on risks from legacy business exits and assign a lower value. This gives you a real-world view of the range of perspectives in the market.

Do you think there's more to the story for Modine Manufacturing? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MOD

Modine Manufacturing

Designs, engineers, tests, manufactures, and sells mission-critical thermal solutions in the United States, Canada, Italy, Hungary, the United Kingdom, China, and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative