Advertisement

- United States

- /

- Auto Components

- /

- NYSE:DAN

Reassessing Dana (DAN) After an 86% Year-to-Date Surge: Is the Valuation Getting Ahead of Earnings?

Simply Wall St

Reviewed by Simply Wall St

Dana (DAN) has quietly turned into a strong performer this year, with the stock up roughly 86% year to date despite softer annual revenue, as improving profitability reshapes how investors are valuing the business.

See our latest analysis for Dana.

That surge has come with some bumps, and the latest 1 day and 7 day share price returns of negative 4.15% and negative 6.29% suggest a breather after big gains. At the same time, a 72.72% 1 year total shareholder return still points to strong, improving sentiment around Dana’s earnings power.

If Dana’s rebound has you rethinking the auto space, it could be worth scanning other auto manufacturers that are showing similar shifts in growth and profitability expectations.

With Dana’s shares already up sharply and trading about 24% below the average analyst target but near some estimates of intrinsic value, the key question is whether this rally still leaves upside or if future growth is fully priced in.

Most Popular Narrative: 19.7% Undervalued

With Dana last closing at $21 and the most followed narrative pointing to fair value near $26, the current gap centers on future earnings power and capital returns.

The strategic redeployment of Off Highway sale proceeds to reduce leverage to <1x EBITDA and an accelerated, below intrinsic value share buyback (~25% reduction in share count), directly boost future earnings per share (EPS) and position Dana for stronger capital returns.

Curious how shrinking revenues and rising margins can still support a higher valuation? This narrative leans on bold EPS compounding and a future earnings multiple that looks more like a quality compounder than a cyclical auto name. Want to see how those moving pieces come together in the model?

Result: Fair Value of $26.14 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, concentrated exposure to a few North American light vehicle customers and execution risk on deeper cost cuts could easily derail this optimistic earnings path.

Find out about the key risks to this Dana narrative.

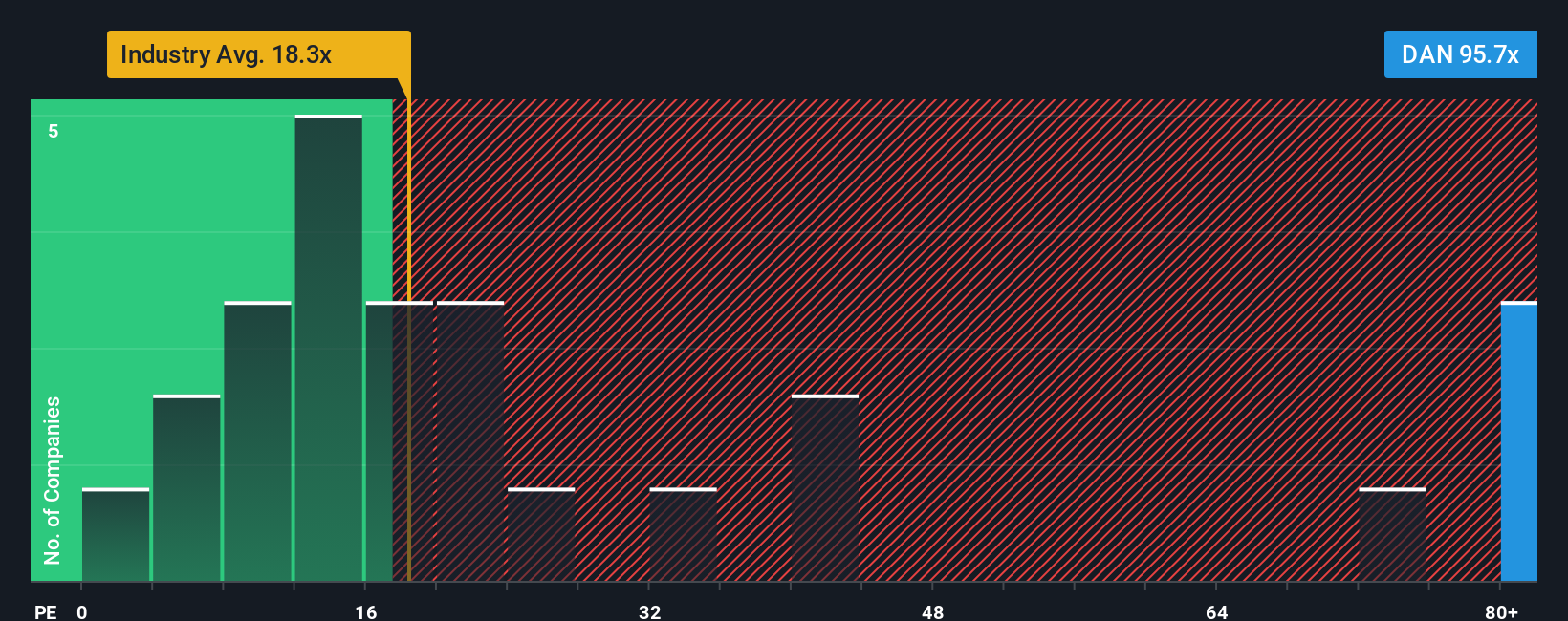

Another View, Rich on Earnings

While the narrative suggests upside to $26, the current price near $21 already implies a steep 37.7x price to earnings ratio versus 18.8x for the US Auto Components industry and a 24.8x fair ratio. That premium signals valuation risk and not a clear bargain, if earnings stumble.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Dana Narrative

If you see the numbers differently or want to stress test your own thesis, you can build a full narrative in minutes: Do it your way.

A great starting point for your Dana research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Use the Simply Wall St Screener now to uncover fresh opportunities across sectors and themes, so you never feel stuck on a single stock story.

- Target steady income by reviewing these 15 dividend stocks with yields > 3% that can help anchor your portfolio with cash returns.

- Capitalize on cutting edge innovation by scanning these 26 AI penny stocks positioned to benefit from the rapid adoption of artificial intelligence.

- Strengthen your value strategy by focusing on these 906 undervalued stocks based on cash flows that may offer attractive upside based on cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DAN

Dana

Provides power-conveyance and energy-management solutions for vehicles and machinery in North America, Europe, South America, and the Asia Pacific.

Average dividend payer with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative