- Taiwan

- /

- Semiconductors

- /

- TWSE:5269

Downgrade: Here's How Analysts See ASMedia Technology Inc. (TPE:5269) Performing In The Near Term

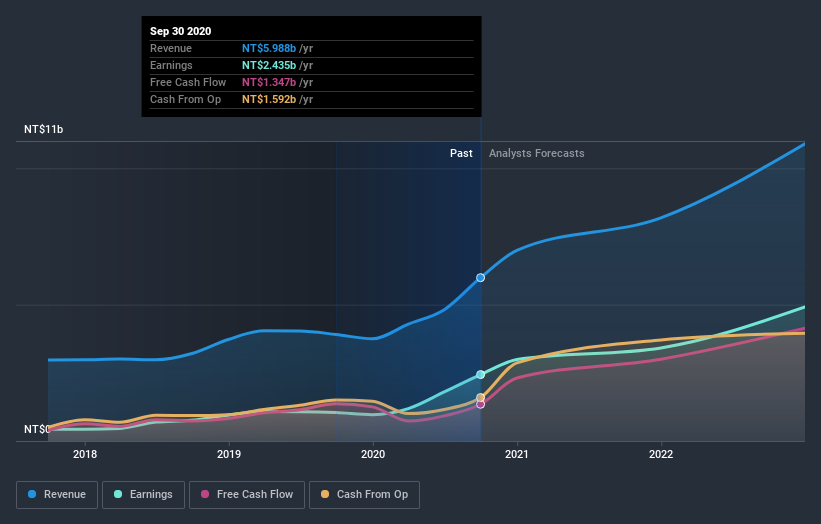

Today is shaping up negative for ASMedia Technology Inc. (TPE:5269) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analysts have soured majorly on the business.

After the downgrade, the five analysts covering ASMedia Technology are now predicting revenues of NT$7.9b in 2021. If met, this would reflect a huge 32% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to shoot up 22% to NT$46.45. Previously, the analysts had been modelling revenues of NT$8.9b and earnings per share (EPS) of NT$52.37 in 2021. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a considerable drop in earnings per share numbers as well.

View our latest analysis for ASMedia Technology

It'll come as no surprise then, to learn that the analysts have cut their price target 9.1% to NT$2,007. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic ASMedia Technology analyst has a price target of NT$2,599 per share, while the most pessimistic values it at NT$1,500. This shows there is still some diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that ASMedia Technology's rate of growth is expected to accelerate meaningfully, with the forecast 32% annualised revenue growth to the end of 2021 noticeably faster than its historical growth of 24% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 14% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that ASMedia Technology is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of ASMedia Technology.

That said, the analysts might have good reason to be negative on ASMedia Technology, given concerns around earnings quality. Learn more, and discover the 2 other risks we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade ASMedia Technology, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:5269

ASMedia Technology

A fabless IC design company, engages in the design, development, production, manufacture, and sale of high-speed analogue circuit products in the United States, Taiwan, China, Southeast Asia, Northeast Asia, and internationally.

Exceptional growth potential with flawless balance sheet.