Advertisement

Saniona (OM:SANION) Profit Margin Hits 77%—Sustainability of Turnaround Challenged by Revenue Decline Forecasts

Simply Wall St

Reviewed by Simply Wall St

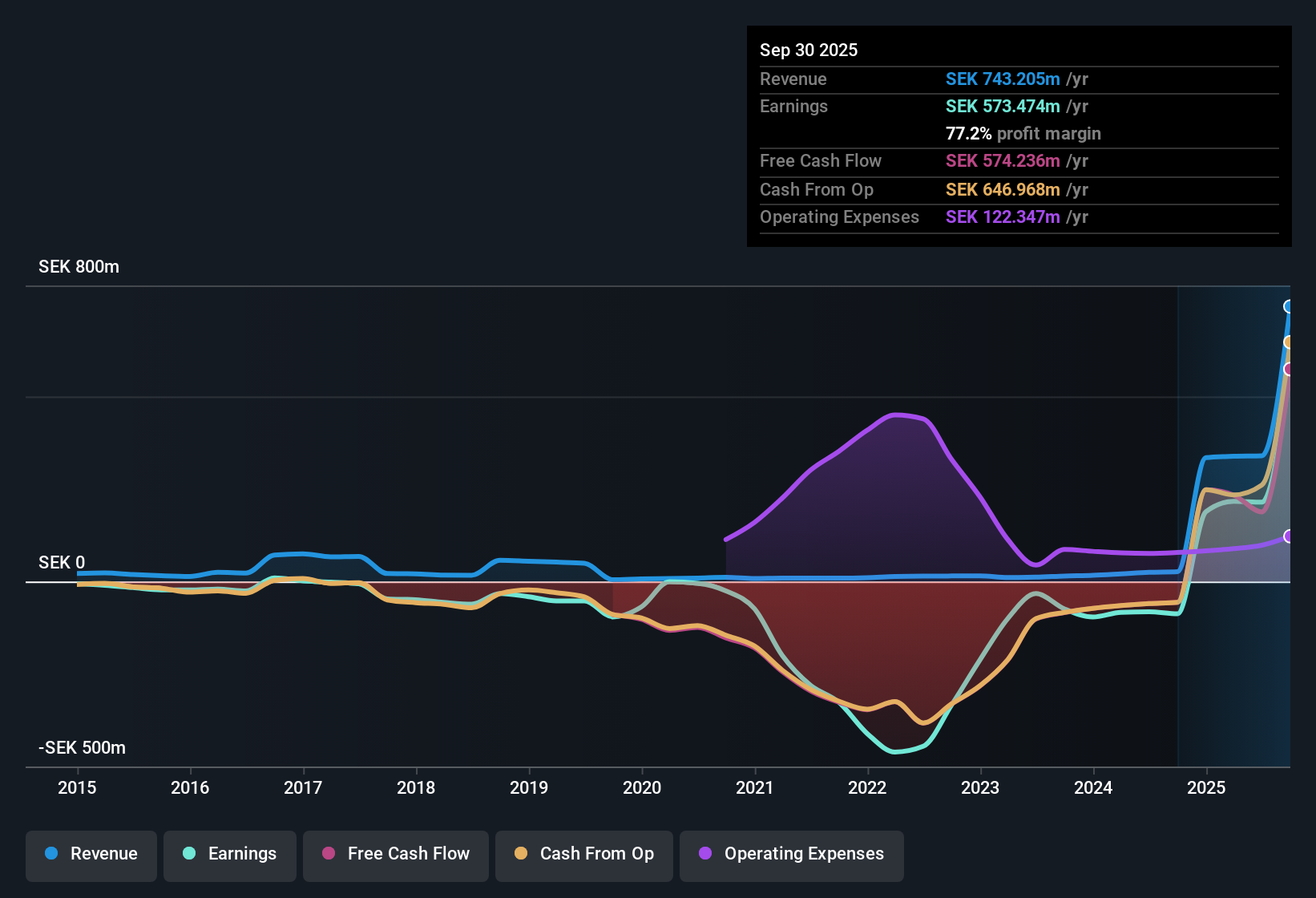

Saniona (OM:SANION) just posted its Q3 2025 results, reporting total revenue of 410.7 million SEK and basic EPS of 2.39 SEK, reflecting a solid headline performance. Over the past twelve months, revenue grew from 334.7 million SEK to 743.2 million SEK, while EPS climbed from 1.77 SEK to 4.64 SEK, marking a sharp uptick in profitability. Margins continued to stand out, with net income delivering a notable boost to the bottom line.

See our full analysis for Saniona.Now let's put these results in context. We will see which parts of the community narrative get confirmed and which take a hit as the latest numbers come through.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Surges to 77% on Trailing Twelve Months

- Saniona delivered net income of 573.47 million SEK from 743.21 million SEK in revenue for the last twelve months, putting net profit margins at a striking 77%.

- What’s notable here, based on prevailing market analysis, is that this surge in margins aligns with the company's transition to profitability. However:

- Net income swung sharply into positive territory compared to prior periods, reinforcing the case that cost controls or one-off revenue may be supporting recent profitability.

- With revenue projected to decline by 25.3% per year over the next three years, the durability of these margins comes into question even as the current level heavily supports investor optimism about future profit potential.

Shares Trade Far Below DCF Fair Value

- Saniona’s current share price is 17.66 SEK, dramatically below its DCF fair value of 1,269.46 SEK, and its P/E ratio sits at just 4.3x compared to the European biotech sector’s 18.3x.

- Investors are paying attention as prevailing market opinion suggests the deep valuation discount and profits signal an overlooked opportunity. However:

- This major divergence from peer and sector valuation multiples could be driven by recent share price volatility and shareholder dilution reported over the past year.

- It creates a tension where strong recent earnings back a bullish outlook, but the market appears unconvinced about the sustainability of these gains, as reflected in the continued low share price.

Revenue Expected to Drop Despite Turn to Profit

- Consensus estimates indicate Saniona’s revenue is set to decline at an annual rate of 25.3% for the next three years, despite recent multi-quarter profitability in EPS and net income.

- Prevailing perspectives highlight a key watchpoint, as future revenue declines challenge the bullish narrative that profitability alone justifies rerating:

- While the company’s trailing twelve month Basic EPS improved to 4.64 SEK from negative levels, expected revenue contraction could limit the runway for further profit growth or margin expansion.

- For investors, the data underscores the need to track whether efficiency and cost management can offset top-line pressures or if falling sales will cap near-term upside.

Bulls looking for deep-value turnaround plays will want to see if historic profitability can hold up as revenue declines, and the current valuation leaves room for significant re-rating if expectations shift.

See what the community is saying about SanionaNext Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Saniona's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Saniona's outlook is clouded by forecasts of sharp revenue declines, raising real doubts about whether its recent profitability can be sustained in the years ahead.

If steady, reliable performance matters to you, switch focus to stable growth stocks screener (2074 results) and target companies with proven resilience and consistent revenue expansion instead.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:SANION

Saniona

A clinical-stage biopharmaceutical company, engages in the research, development, and commercialization of treatments for rare disease patients in Sweden, the United States, Germany, Denmark, and the United Kingdom.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative