Advertisement

KB Components (OM:KBC) Earnings Growth Accelerates 13.7%, Supporting Bullish Market Narratives

Simply Wall St

Reviewed by Simply Wall St

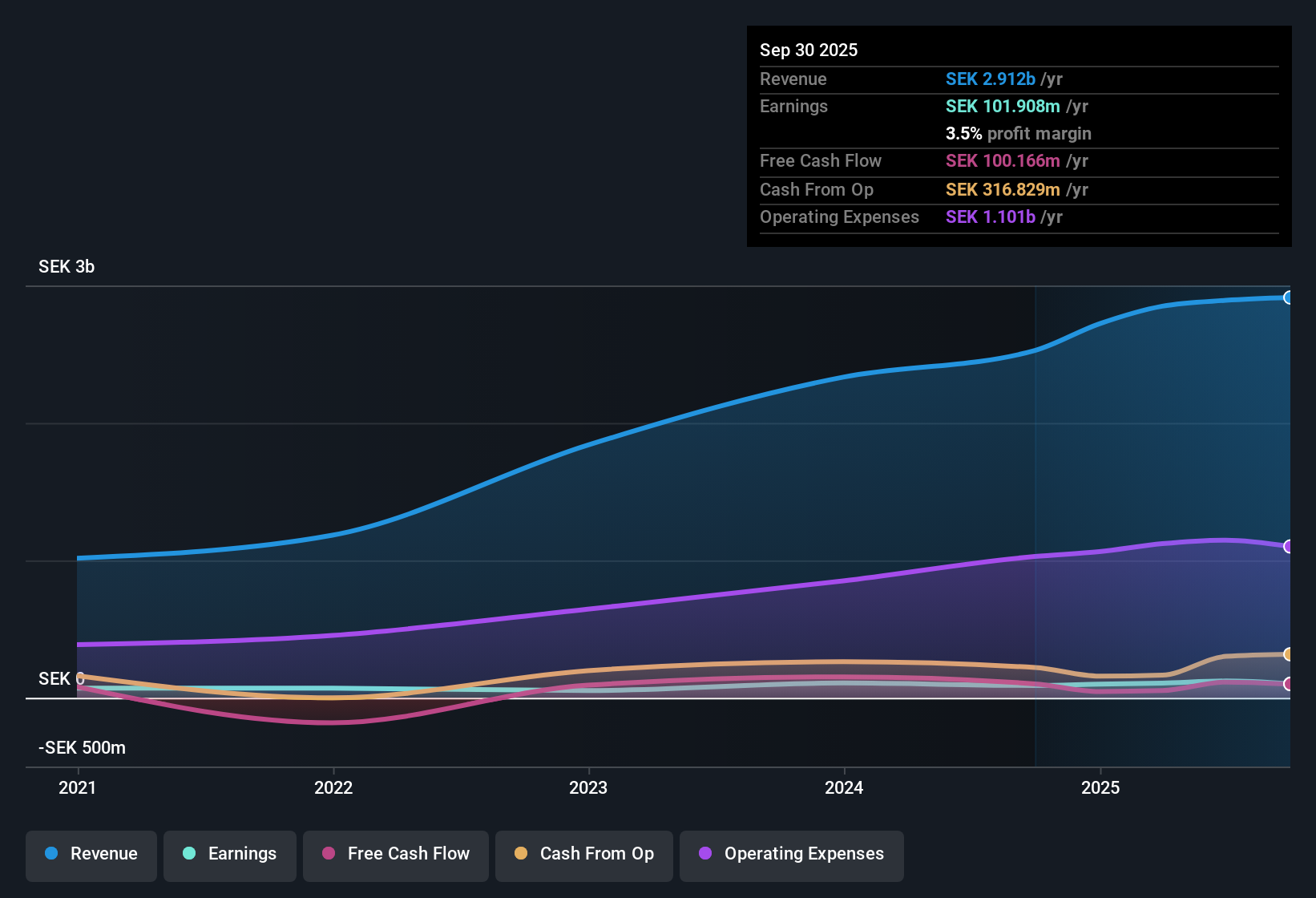

KB Components (OM:KBC) has just posted its Q3 2025 results, reporting revenue of 625.3 million SEK and basic EPS of 0.27 SEK for the quarter. Looking back, the company has seen revenue fluctuate from 808.5 million SEK in Q4 2024 to 625.3 million SEK in Q3 2025, while EPS moved from -0.01 SEK to 0.27 SEK over the same span. Margins remained steady, with the latest figures reflecting consistent profitability and setting the stage for investor debate.

See our full analysis for KB Components.Next, we will put the latest numbers side by side with the prevailing narratives from the market and the Simply Wall St community to see what holds up and what gets challenged.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Holds Firm at 3.5%

- KB Components maintained a net profit margin of 3.5% for the trailing twelve months, unchanged from the previous year, showing that operational profitability has been steady even as other metrics have shifted.

- What is striking in the prevailing market view is how margin stability contrasts with fluctuating quarterly earnings. While quarterly net income varied from -0.8 million SEK in Q4 2024 to 15.3 million SEK in Q3 2025, the company’s annual profit margin shows that volatility in revenue did not erode overall profitability.

- Quarterly net income swings highlight exposure to operational headwinds, but the full-year margin trend points to effective cost management.

- This pattern supports the case that sector and client diversity are giving KB Components resilient earnings capacity despite industry-specific price pressures.

Earnings Rise Accelerates Past Long-Term Pace

- Earnings increased 13.7% over the past year, well above the 5-year average annual growth rate of 11.4%, signaling acceleration in the bottom line that outpaces KB Components’ own historical results.

- The narrative highlights that such a step-up gives weight to arguments about above-market growth momentum. Trailing twelve-month net income climbed to 101.9 million SEK, topping both the previous year and long-term benchmarks.

- Growth outpaces the broader Swedish market, where forecasted earnings rises are slower. KB Components’ estimates for next year’s earnings growth (25.9% p.a.) and revenue growth (7% p.a.) both exceed market averages, reinforcing optimism on forward prospects.

- Even though the latest quarter’s net income dipped to 15.3 million SEK, the annualized acceleration reflects underlying business improvement, not just short-term bounces.

Trading Far Below DCF Fair Value, Despite Higher P/E

- The current share price of 38.05 SEK sits 53.8% below the DCF fair value estimate of 82.42 SEK, while the P/E ratio of 20.9x is above the 12.9x peer average and the 17.9x European industry average.

- Prevailing market opinion views this valuation setup as a double-edged sword. On the upside, the sizeable gap to DCF fair value hints at a possible bargain, but higher than average multiples and noted balance sheet debt mean investors should weigh both the potential for re-rating and the risks of volatility.

- Critics point out that high leverage and share price swings, relative to the Swedish market, are important watchpoints that temper straightforward deep value arguments.

- DCF-based discount could attract value-focused investors, but commitment requires comfort with inherent risk and earnings durability beyond short-term results.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on KB Components's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite accelerating earnings, KB Components faces ongoing concerns about high leverage and potential volatility related to its balance sheet health.

If you want less exposure to debt risk, check out solid balance sheet and fundamentals stocks screener (1937 results) to find companies built on stronger financial footing for greater peace of mind.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KB Components might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:KBC

KB Components

Designs, develops, manufactures, and sells polymer components for light vehicles, heavy vehicles, medical, furniture, lighting, chrome plating, and industrial applications in Sweden and internationally.

High growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative