Advertisement

- Philippines

- /

- Food

- /

- PSE:RFM

3 Top Undervalued Small Caps In Asian Markets With Insider Buying

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, Asian markets have been navigating a complex landscape marked by trade tensions and economic policy shifts, impacting investor sentiment and small-cap stocks. Despite these challenges, opportunities may arise for investors looking at small-cap companies that demonstrate strong fundamentals and potential for growth. Identifying such stocks often involves examining factors like insider buying activity, which can signal confidence from those closest to the company's operations.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.3x | 1.0x | 38.25% | ★★★★★★ |

| Infomedia | 29.9x | 3.3x | 30.65% | ★★★★★☆ |

| East West Banking | 3.1x | 0.7x | 33.41% | ★★★★★☆ |

| ReadyTech Holdings | NA | 2.4x | 49.86% | ★★★★★☆ |

| Puregold Price Club | 8.7x | 0.4x | 41.52% | ★★★★☆☆ |

| Atturra | 28.7x | 1.2x | 32.28% | ★★★★☆☆ |

| Sing Investments & Finance | 7.2x | 3.7x | 39.63% | ★★★★☆☆ |

| Dicker Data | 18.5x | 0.6x | -13.63% | ★★★☆☆☆ |

| Pacific Textiles Holdings | 11.9x | 0.4x | 44.65% | ★★★☆☆☆ |

| Integral Diagnostics | 157.1x | 1.8x | 34.20% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

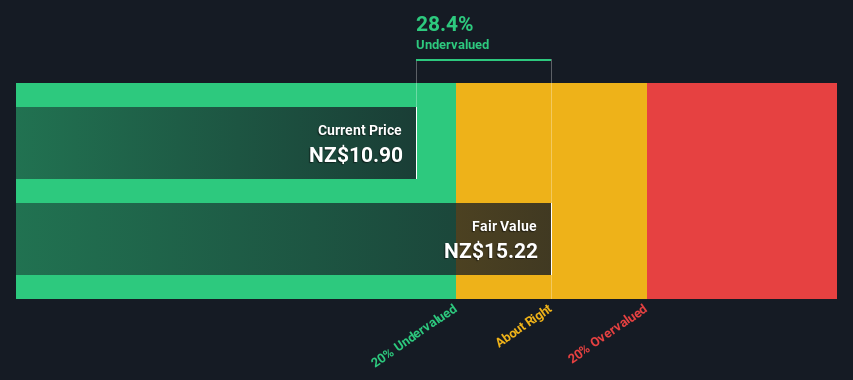

Freightways Group (NZSE:FRW)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Freightways Group is a logistics and information management company that operates primarily in express package and business mail services, with a market capitalization of NZ$1.52 billion.

Operations: Freightways Group generates revenue primarily from its Express Package & Business Mail segment, contributing NZ$1.03 billion, and Information Management segment, adding NZ$226.23 million. The company's gross profit margin has shown a declining trend from 33.66% in December 2016 to 29.52% in December 2024, indicating changes in cost structure or pricing strategies over time.

PE: 26.1x

Freightways Group, a small company in Asia, has caught attention due to its insider confidence. Recent share purchases by insiders in the past six months indicate belief in its potential. Despite having A$1.2 billion of debt primarily from external borrowing, which is considered higher risk, the company's earnings are expected to grow 11% annually. This growth potential paired with insider activity suggests optimism about future performance amidst financial challenges.

- Navigate through the intricacies of Freightways Group with our comprehensive valuation report here.

Understand Freightways Group's track record by examining our Past report.

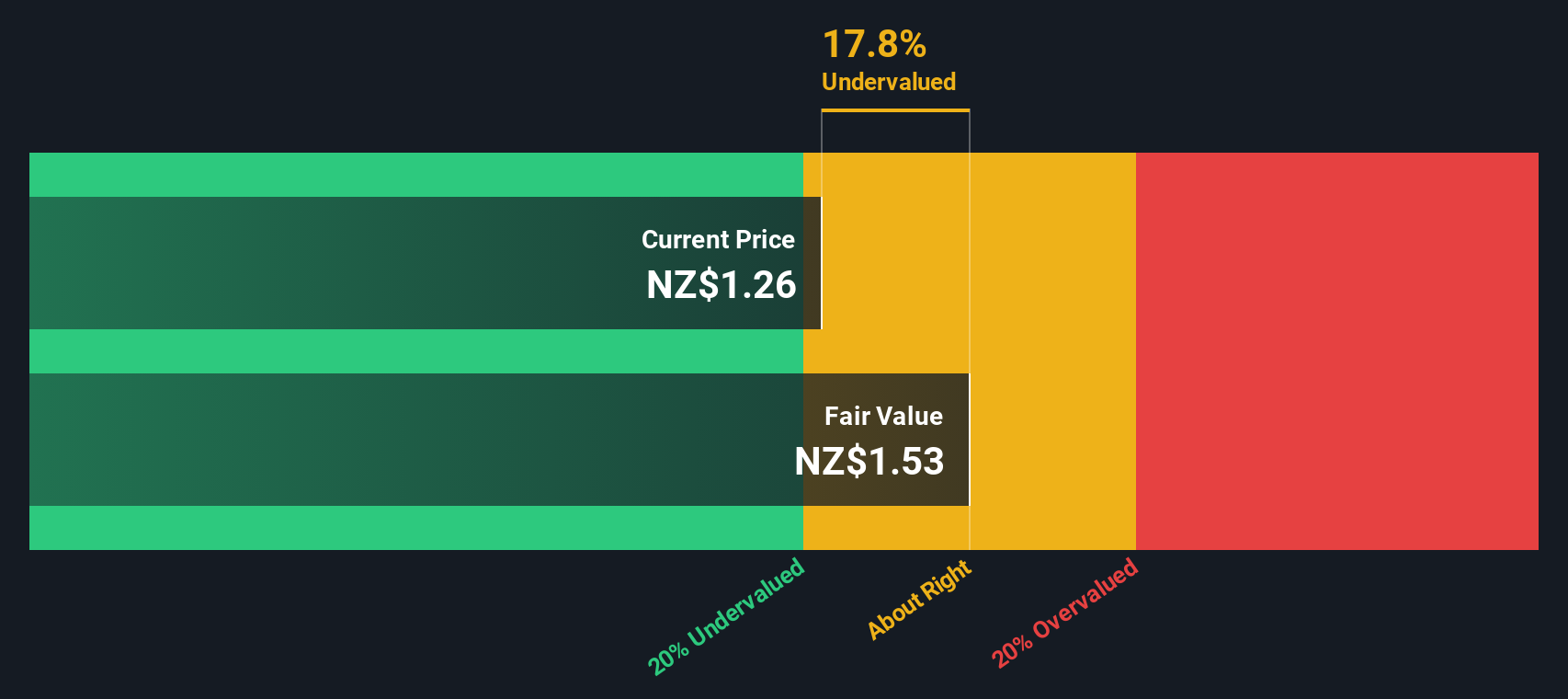

Precinct Properties NZ & Precinct Properties Investments (NZSE:PCT)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Precinct Properties NZ is a real estate investment company focused on premium office and mixed-use properties, with operations spanning flexible spaces, hotel and hospitality services, investment management, and investment properties; it has a market capitalization of approximately NZ$1.98 billion.

Operations: Precinct Properties generates revenue primarily from its investment properties, which account for NZ$215.60 million, followed by flexible space and hotel and hospitality segments. The company has seen fluctuations in net income margins, with a notable decline to -0.10% as of December 2024. Operating expenses have been consistently around NZ$20-22 million, while non-operating expenses have varied significantly over time, impacting overall profitability.

PE: -66.4x

Precinct Properties, a small player in Asia's property sector, has caught attention with insider confidence shown through recent share purchases. Their commitment to developing student accommodation for the University of Auckland and forming a strategic partnership with a Singapore-based investor highlights growth ambitions. However, reliance on external borrowing poses financial risks. Despite this, earnings are projected to grow 65% annually, suggesting potential for future value creation amidst these challenges.

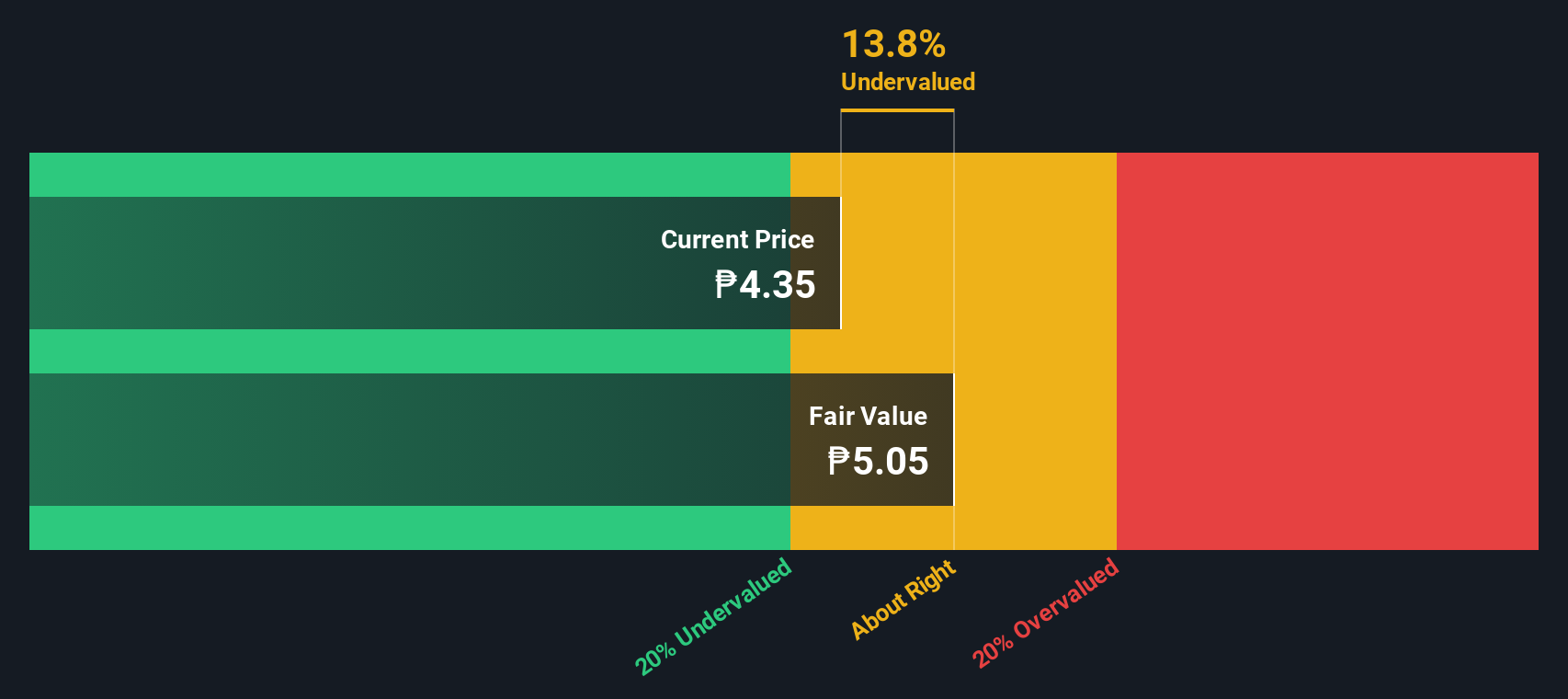

RFM (PSE:RFM)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: RFM is a company engaged in the consumer and institutional business sectors, with operations including various revenue segments, and it has a market capitalization of ₱18.68 billion.

Operations: The Consumer Business segment is the primary revenue driver, generating ₱16.50 billion, while the Institutional Business contributes ₱5.32 billion. Over recent periods, gross profit margin has shown a varied trend, reaching 35.21% in December 2021 and fluctuating to 33.40% by March 2025. Operating expenses have been significant, with Sales & Marketing consistently being a major component within these costs.

PE: 9.4x

RFM's recent performance highlights its potential as an undervalued player in Asia's market. In the first quarter of 2025, sales rose to PHP 4.5 billion from PHP 4.4 billion last year, with net income jumping to PHP 310 million from PHP 200 million. Despite relying solely on external borrowing for funding, the company demonstrates resilience through consistent earnings growth and a commitment to shareholder returns with two cash dividends totaling PHP 400 million in early 2025.

Next Steps

- Click this link to deep-dive into the 63 companies within our Undervalued Asian Small Caps With Insider Buying screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:RFM

RFM

Engages in milling, manufacturing, and marketing food and beverage products in the Philippines and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative