Advertisement

- Norway

- /

- Oil and Gas

- /

- OB:BWLPG

Assessing BWG’s Valuation After New LNG Vessel Acquisition and Three Year 155% Rally

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if BWG stock is undervalued, fairly priced, or ready for a breakout? You're in the right place for a confident, clear-eyed look at what really drives the company's value.

- While the share price dipped 4.9% this week and is down 2.3% in the last month, BWG's longer-term growth remains impressive. Its stock has soared 155.3% over the past three years and 415.5% over five years.

- Recent market moves reflect rising interest as BWG announced a strategic vessel acquisition, boosting its LNG transport capacity and stirring fresh debate over future earnings power. The news has given analysts and investors more reason to watch closely for industry shifts that may be on the horizon.

- Looking at the numbers, BWG posts a solid valuation score of 5 out of 6, meaning it is considered undervalued on most standard checks. However, as we'll see, there is more than one way to figure out what the stock is really worth.

Approach 1: BWG Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and discounting them back to today’s value. This approach helps investors assess whether a stock’s current price reflects its underlying business prospects.

For BWG, the current Free Cash Flow stands at $211 million. Looking forward, analysts expect strong performance, with free cash flow forecast to rise to $363 million by 2027. Additionally, the most recent projections suggest that free cash flow could stabilize near $186 million by 2035, with estimates for intermediate years showing some natural cooling off from peak levels. While analysts typically provide estimates only five years ahead, these longer-term figures are extrapolated to provide a broader perspective.

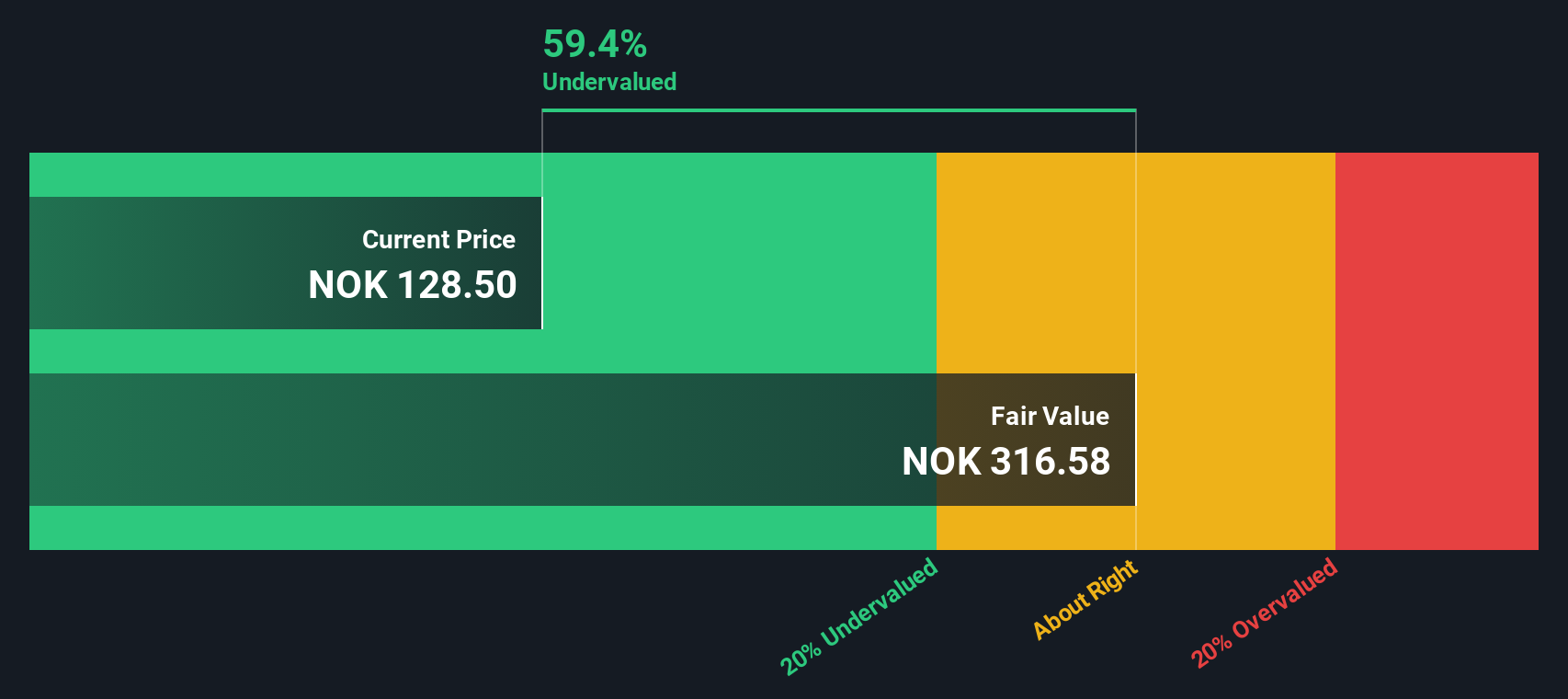

Based on these projections, the DCF analysis calculates BWG’s intrinsic fair value at $315.93 per share. Compared to the current share price, this suggests that BWG is trading at a significant 60.6% discount, indicating it is undervalued relative to the company’s long-term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BWG is undervalued by 60.6%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: BWG Price vs Earnings

The Price-to-Earnings (PE) ratio is often the preferred valuation metric for profitable companies because it directly connects a company’s share price with its bottom-line earnings. This relationship makes it a practical way to assess whether investors are paying a reasonable price for each unit of profit the company generates.

Typically, a higher PE ratio is justified for companies with above-average growth prospects or lower risk profiles, while lower PEs are more common if growth is limited or the company faces unique challenges. Industry norms and market sentiment both influence what is viewed as “normal” or “fair.”

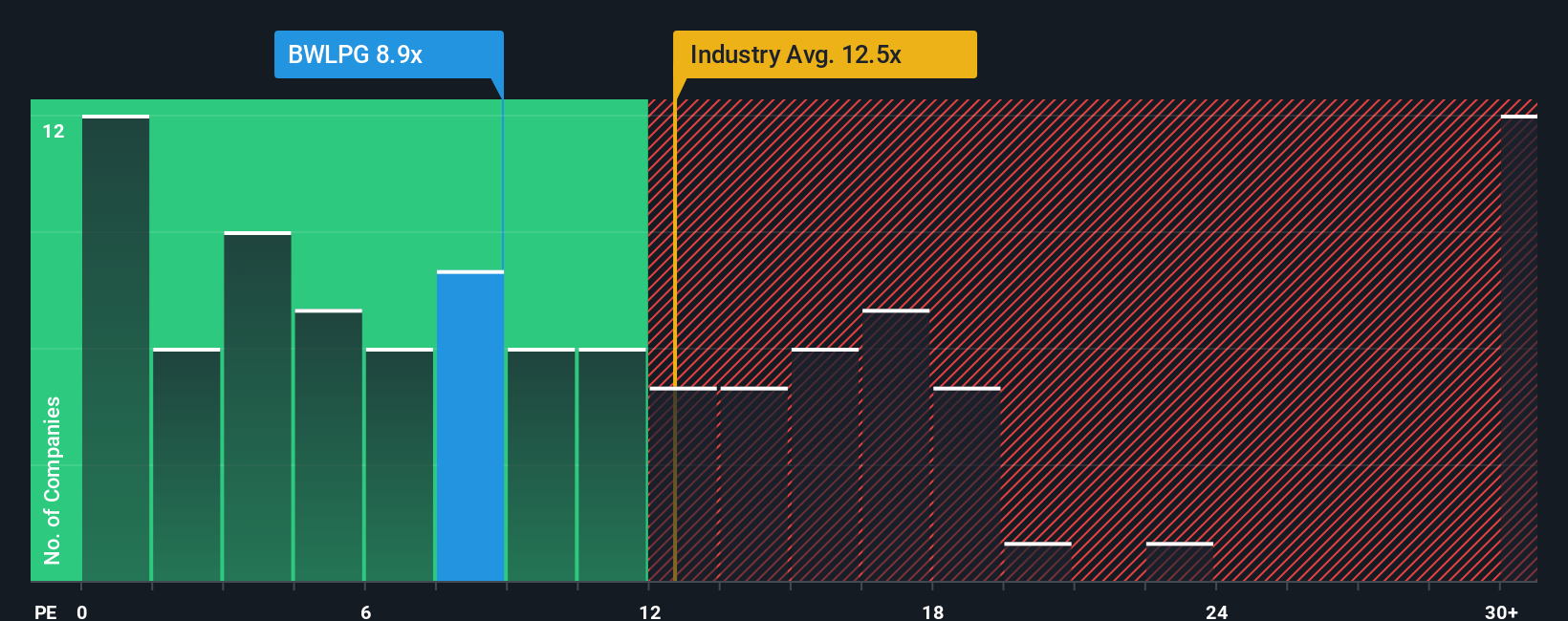

For BWG, the current PE ratio is 8.56x. This compares favorably to the peer average of 9.07x and is notably below the broader Oil and Gas industry average of 13.21x. At first glance, this could suggest BWG’s shares provide good value when using standard benchmarks.

Simply Wall St’s proprietary "Fair Ratio" for BWG is 6.06x. This modelled figure takes into account the company’s expected earnings growth, profit margins, risk profile, size, and the specific characteristics of its industry and market capitalization. It offers a more customized benchmark than simple comparisons to peers or sector norms.

Comparing BWG’s actual PE of 8.56x with the Fair Ratio of 6.06x indicates the shares are trading somewhat higher than what would be expected based on its fundamentals, suggesting the stock may be slightly overvalued on this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BWG Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a story that connects your unique perspective on a company, like BWG, with your own forecast for its future revenue, earnings, and profit margins. This story ultimately ties to an estimated fair value for the stock. Narratives help you see how your beliefs about key business drivers translate into actionable numbers, making it much easier to decide whether BWG's current share price represents an opportunity or a risk for you.

This approach is dynamic and accessible. It is built into Simply Wall St’s Community page, where millions of investors create and share their own Narratives. With Narratives, you compare your calculated Fair Value to the latest Price, so you can see in real time whether you would choose to buy, hold, or sell. In addition, Narratives automatically update as new earnings, news, or company developments arise, ensuring your view reflects the most current information.

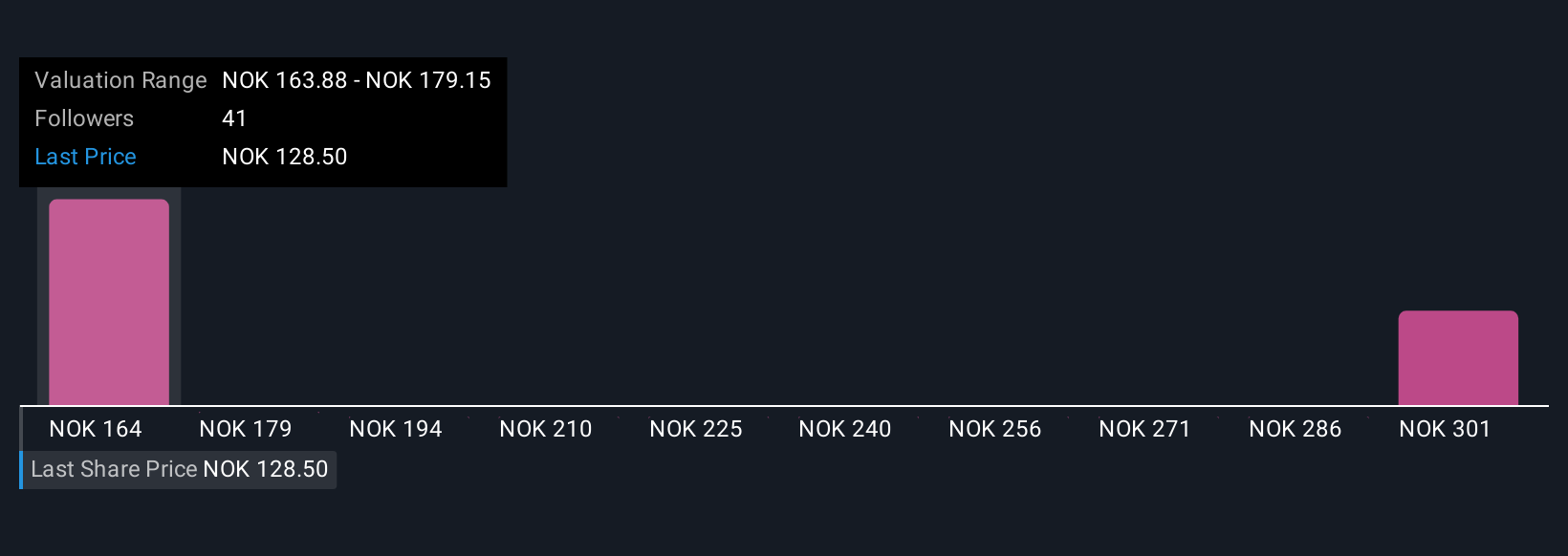

For example, one investor may forecast a fair value of NOK 185.02 for BWG, seeing strong industry tailwinds, while another might set it as low as NOK 158.03, highlighting challenges such as falling spot rates and rising risks. This illustrates how Narratives capture a full spectrum of market perspectives.

Do you think there's more to the story for BWG? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BWG might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:BWLPG

BWG

An investment holding company, engages in ship owning and chartering activities worldwide.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative