Advertisement

- Netherlands

- /

- Professional Services

- /

- ENXTAM:ARCAD

Do Arcadis Shares Offer Value After Recent 36% Price Drop?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Arcadis stock is undervalued or if there is hidden opportunity in the recent price action? Here is a direct look at what the numbers show.

- The stock increased 7.1% over the last week, but it is still down 24.6% for the month and has dropped 36.3% so far this year. Its one-year return stands at -38.2%, although it shows a longer-term five-year gain of 64%.

- Recent headlines have highlighted the volatility, with Arcadis involved in high-profile infrastructure projects and strategic acquisitions that have influenced the sector. Developments such as the company’s focus on resilient urban design and shifts in global government infrastructure budgets provide additional context for the recent changes in share price.

- When examining valuation, Arcadis earns a perfect 6 out of 6 score based on key undervaluation checks, but there is more to consider. We will now review common valuation approaches and later discuss a perspective that may influence how Arcadis’s value is viewed.

Find out why Arcadis's -38.2% return over the last year is lagging behind its peers.

Approach 1: Arcadis Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a widely used valuation approach that works by forecasting a company’s expected future cash flows and then discounting them back to their present value using today’s terms. This method provides an estimate of what Arcadis might be worth based on how much cash the business is expected to generate in the coming years.

For Arcadis, the most recent full-year free cash flow reported was €247.6 million. Analysts anticipate consistent growth, with cash flow projections reaching €292 million in 2026 and €381.5 million by 2029. Beyond the fifth year, estimates are extrapolated to continue this trend, ultimately reaching over €470 million in 2035, according to Simply Wall St projections.

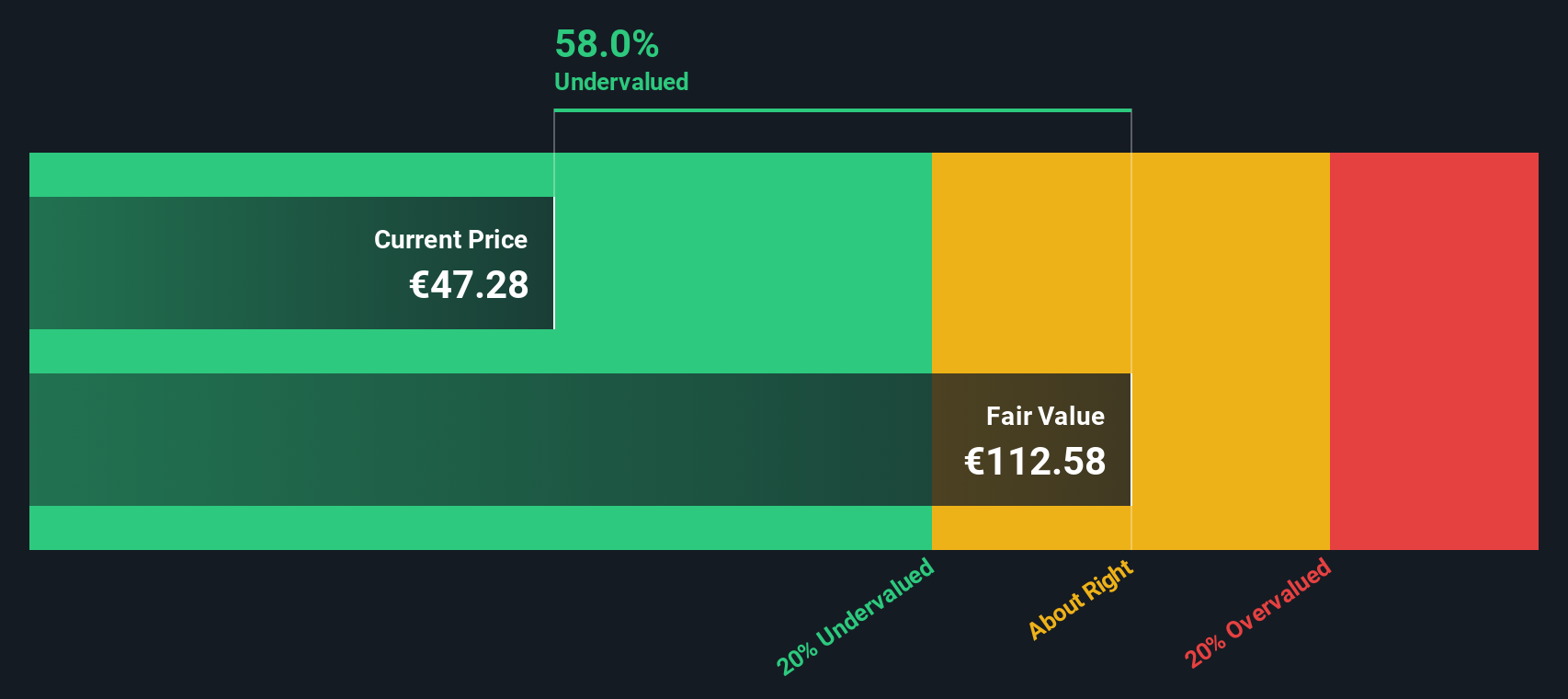

The DCF model results in an intrinsic value of €104.36 per share for Arcadis. This figure suggests the stock is currently trading at a substantial discount. The model indicates Arcadis is undervalued by 63.9% compared to present market prices. In other words, the current share price is well below what the company’s cash flows are expected to justify.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Arcadis is undervalued by 63.9%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

Approach 2: Arcadis Price vs Earnings

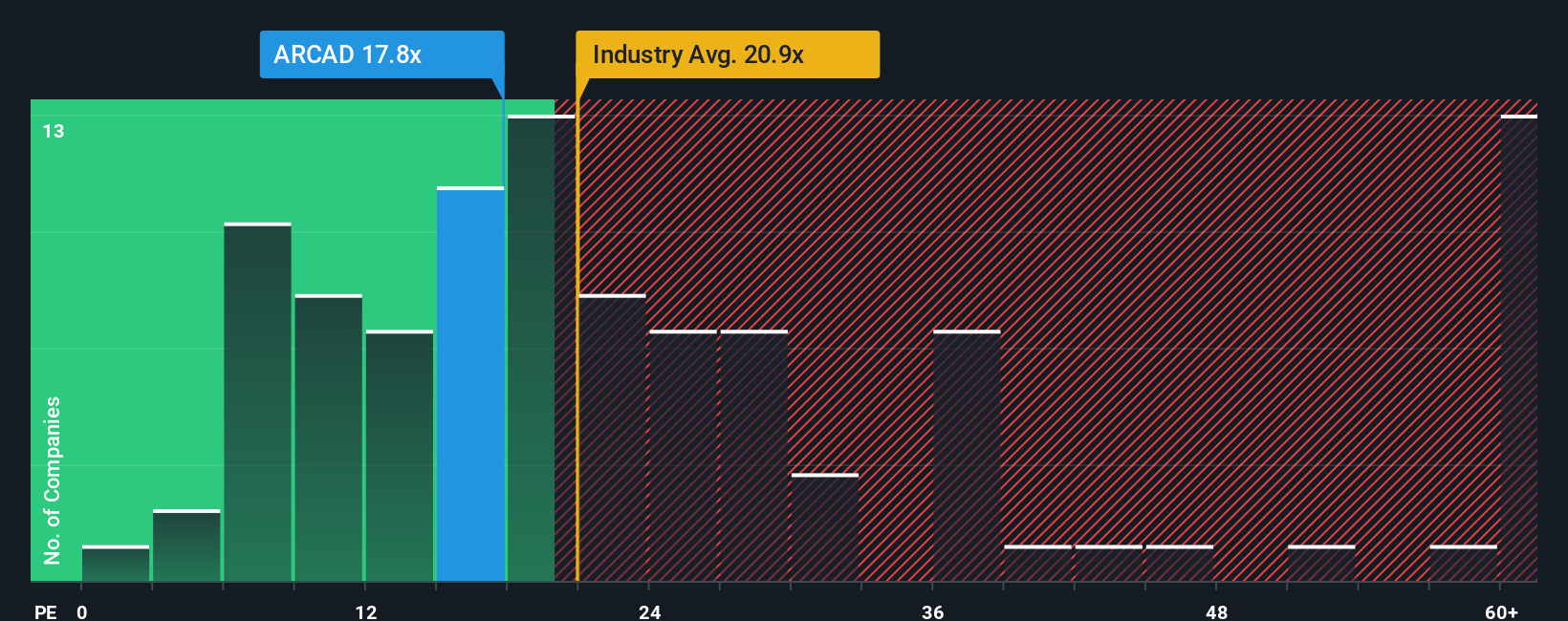

The price-to-earnings (PE) ratio is a widely used valuation tool for profitable companies like Arcadis, as it shows how much investors are willing to pay for each euro of earnings. It is particularly relevant for firms with stable profits, as it allows for quick comparisons against both peers and industry benchmarks.

The appropriate or “fair” PE ratio can vary depending on several factors, including a company’s growth prospects and risk profile. High-growth, lower-risk companies often warrant higher PE ratios, while slower growth or riskier businesses tend to trade at lower multiples.

Currently, Arcadis trades at a PE ratio of 13.9x. For context, the industry average for Professional Services stands at 18.1x, and peer companies trade at an even higher average of 48.0x. This positions Arcadis well below typical sector and peer valuations.

To offer deeper insight, Simply Wall St applies a proprietary “Fair Ratio,” a data-driven metric estimating what Arcadis’s PE ratio should be, adjusting for factors like growth expectations, profitability, company size, and risks. This approach is more robust than a simple peer or industry comparison, as it personalizes valuation to Arcadis’s unique financial and operational profile.

In this case, Arcadis’s Fair Ratio is calculated as 19.1x, noticeably above its current PE multiple. This suggests the market may be underestimating Arcadis’s earnings potential relative to its risk and growth outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Arcadis Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple yet powerful tool that lets investors tell the story behind their numbers by combining personal assumptions about Arcadis’s future revenue, margins, and fair value with the latest data to craft a forecast that is truly their own.

Narratives connect your perspective on Arcadis’s business outlook to a financial forecast and an estimated fair value, making it easier to see how your view compares with both the market and other investors. Accessible via the Simply Wall St Community page used by millions worldwide, Narratives simplify investment decisions by showing when the gap between Fair Value and Current Price might present an opportunity to buy or sell.

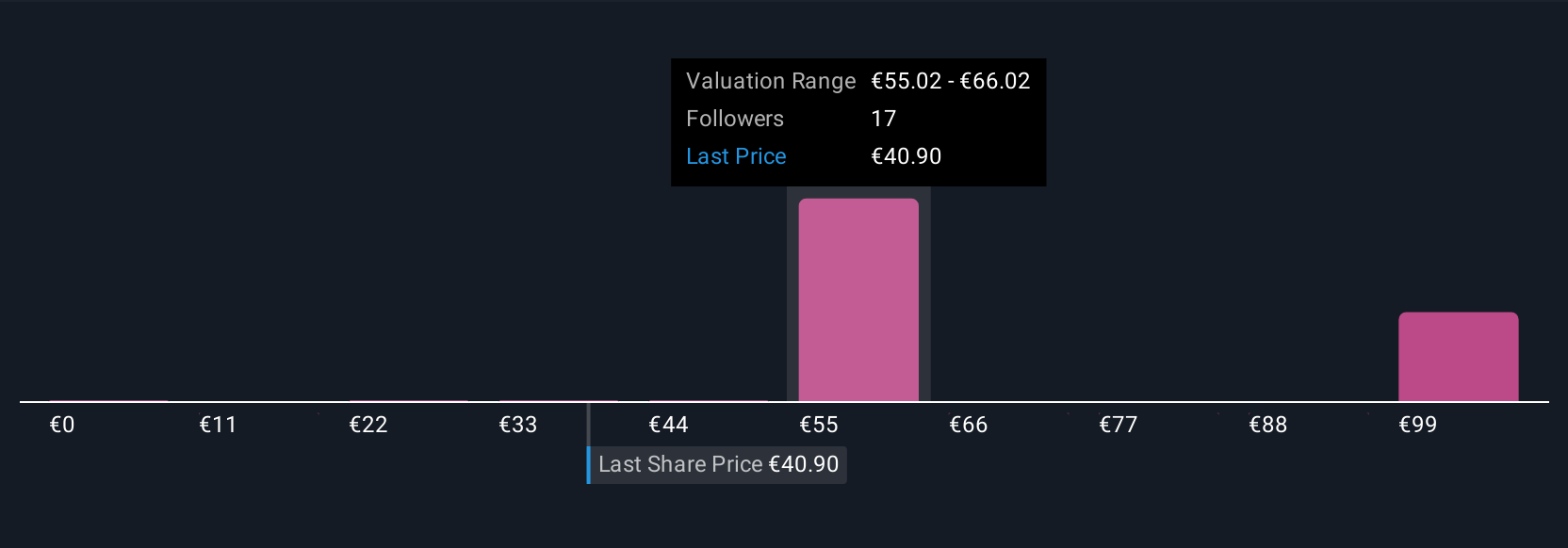

What is more, Narratives update automatically whenever new news or earnings reports are released, ensuring your research stays current. For example, while some Arcadis investors see opportunity and set a price target as high as €70.5 due to optimism about digitalization and resilient backlog growth, others are more cautious, setting their fair value at just €47.0 as they focus on execution risks and margin pressures. Narratives put these perspectives at your fingertips, empowering you to invest with conviction.

Do you think there's more to the story for Arcadis? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ARCAD

Arcadis

Offers design, engineering, architecture, and consultancy solutions for natural and built assets in The Americas, Europe, the Middle East, and the Asia Pacific.

Very undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative