Advertisement

- Netherlands

- /

- Banks

- /

- ENXTAM:INGA

Is ING Groep Still a Bargain After a 63% Price Surge in 2024?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if ING Groep could be a bargain or has already run ahead of itself? You are not alone. Many investors are eyeing the stock’s current price and what it actually represents in value terms.

- The share price has been anything but sleepy lately, rising 3.9% over the past week and a striking 47.2% since the start of the year. This brings a notable 63.6% return over the last 12 months.

- This increase in price has come alongside a wave of positive sentiment, supported by the company’s strategic initiatives and a broader uptick in the European banking sector. Multiple reports have pointed to improved balance sheet strength and recently announced share buybacks.

- When measured against our standard checks, ING Groep achieves a valuation score of 2 out of 6. This suggests there may be more beneath the surface. Next, we will dig into a variety of valuation methods to see where the numbers land, but even those do not tell the full story, so stay tuned for a fresh perspective at the end.

ING Groep scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: ING Groep Excess Returns Analysis

The Excess Returns valuation model is designed for banks and financial institutions, where it gauges value based on the return a company generates on its shareholders’ equity over and above its cost of equity. Instead of focusing on projected cash flows alone, it measures whether the company can reinvest at rates higher than what investors demand, thus creating value for shareholders.

For ING Groep, the model shows a book value of €16.84 per share and stable earnings per share (EPS) of €2.41, calculated from a consensus of 15 analysts’ future return on equity (ROE) forecasts. The cost of equity for the business is €1.13 per share. This means ING Groep earns €1.28 per share in “excess” profits above its required return, with an average ROE of 13.43%. In the longer run, analysts estimate a stable book value near €17.95 per share, showing confidence in sustained growth and profitability.

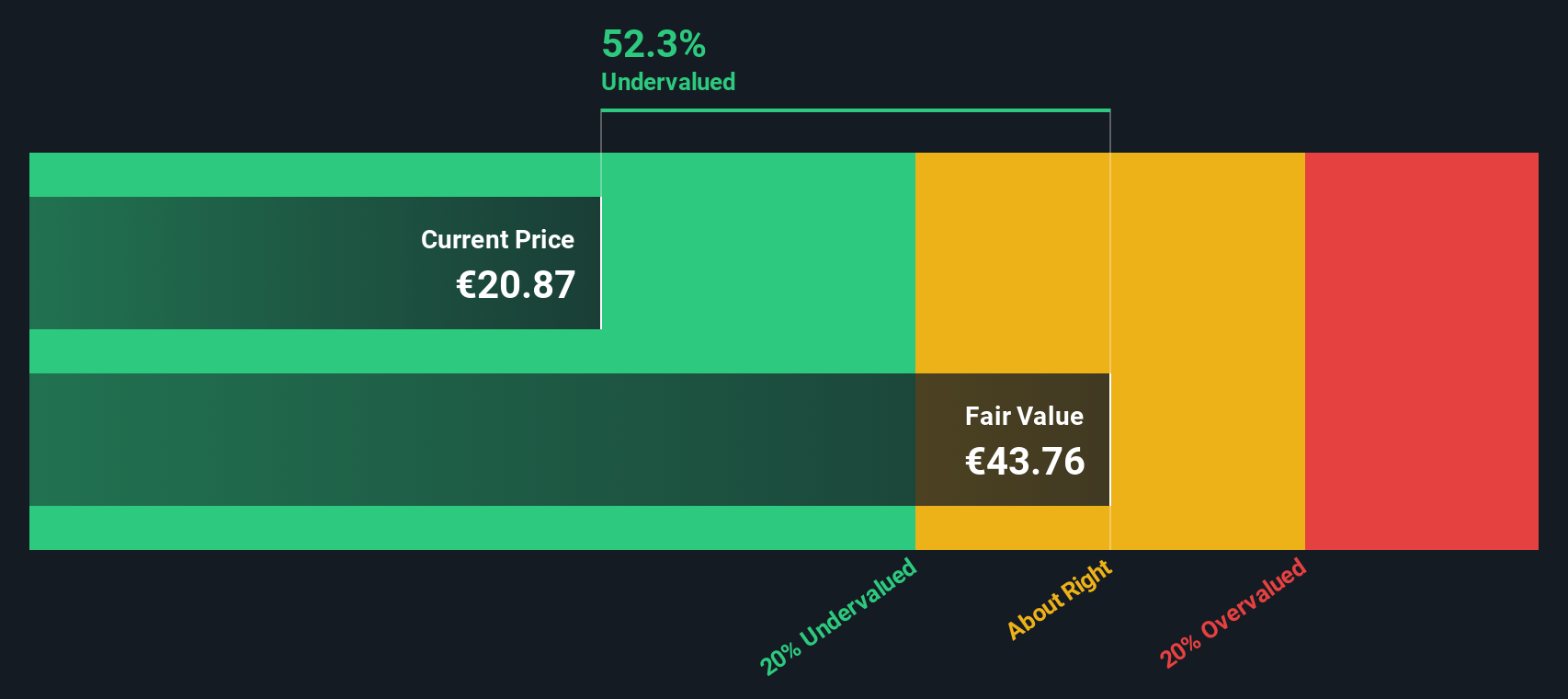

Applying these figures, the intrinsic value estimate suggests ING Groep’s shares are trading at a 51.8% discount versus their fair value. This substantial margin signals that the stock is meaningfully undervalued according to the Excess Returns approach, despite recent share price gains.

Result: UNDERVALUED

Our Excess Returns analysis suggests ING Groep is undervalued by 51.8%. Track this in your watchlist or portfolio, or discover 921 more undervalued stocks based on cash flows.

Approach 2: ING Groep Price vs Earnings

For profitable companies like ING Groep, the price-to-earnings (PE) ratio is a widely recognized valuation metric. It links a company’s share price directly to its underlying earnings power, making it a practical way to assess how much investors are willing to pay for each euro of earnings. This can offer insights into expectations for future growth and risk.

Growth prospects and risk levels play a major role in determining what constitutes a “fair” PE ratio. Faster-growing or more stable companies typically justify higher PE ratios because investors expect larger future earnings or steadier results. In contrast, lower-growth or riskier firms are generally valued more conservatively by the market.

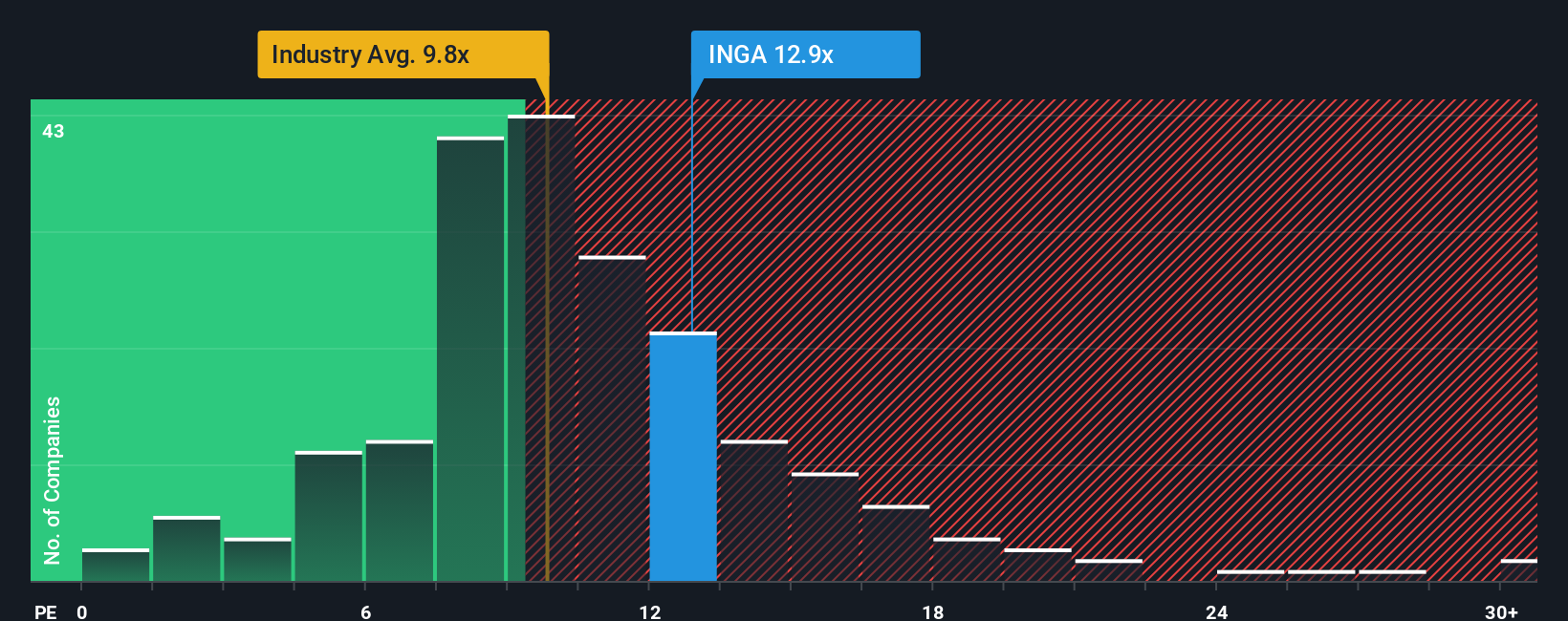

Currently, ING Groep trades at a PE of 13.0x. This is above both the industry average PE of 10.4x for banks and the peer group average of 9.9x. On the surface, this could suggest ING Groep is priced at a premium to its direct competition. However, Simply Wall St’s proprietary Fair Ratio sets the company’s fair PE at 12.3x, which takes into account ING’s growth, risks, profit margin, industry standing, and market capitalization as a single, holistic benchmark.

The Fair Ratio serves as a more robust comparison point than peers or industry averages. Unlike raw market comparisons, it is specifically tailored to ING Groep’s unique financial and business profile, providing a deeper, context-driven assessment of value.

With ING Groep’s current PE just above its Fair Ratio by less than 0.1x, the stock appears to be valued about right relative to its fundamentals and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ING Groep Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives are simple, powerful investment stories that allow you to express your perspective on a company like ING Groep. Essentially, they link your view of the business and industry to concrete financial forecasts, which then drive your estimated fair value. Using Narratives on Simply Wall St’s Community page, millions of investors can access or create these stories, update them as news and results emerge, and make smarter decisions about when to buy or sell by directly comparing their fair value to the market price.

This makes the process more dynamic and personal than relying solely on backward-looking multiples or consensus figures. For instance, if you expect ING Groep’s future to be bright, with fair value as high as €27.92 based on optimistic fee and loan growth, your story will differ from more cautious forecasts that set fair value closer to €17.50. Both approaches are instantly visible, actionable, and update automatically as new information becomes available.

Do you think there's more to the story for ING Groep? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:INGA

ING Groep

Provides various banking products and services in the Netherlands, Belgium, Germany, rest of Europe, and internationally.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative