Advertisement

- Netherlands

- /

- Banks

- /

- ENXTAM:ABN

A Look at ABN AMRO (ENXTAM:ABN) Valuation Following Third Quarter Earnings Decline

Simply Wall St

Reviewed by Simply Wall St

ABN AMRO Bank (ENXTAM:ABN) has published its third quarter and year-to-date earnings, highlighting declines in both net interest income and net income compared to the previous year. The latest results give investors a new perspective on the bank’s recent performance.

See our latest analysis for ABN AMRO Bank.

Despite the dip in quarterly profits, ABN AMRO’s resilience has fueled strong investor sentiment, with the share price climbing 85.8% so far this year and a remarkable 97.6% total shareholder return over the past 12 months. This momentum reflects growing confidence in the bank’s post-earnings outlook, even as sector risks remain on investors’ minds.

If ABN AMRO’s recent surge has you thinking more broadly, this could be the perfect moment to discover fast growing stocks with high insider ownership.

With shares up nearly 100% over the past year, investors now face a pivotal question: is ABN AMRO still trading at an attractive valuation, or has the market already factored in its future potential?

Most Popular Narrative: 3% Overvalued

ABN AMRO's most widely followed valuation narrative puts fair value at €26.98, slightly below the last close of €27.78. This small gap is fueling debate about whether the recent rally leaves more upside, or if expectations are finally priced in.

Increasing client focus on sustainable finance, evidenced by €2.5 billion in circular economy deals (targeting €3.5 billion by 2027) and active embedding of sustainability in lending decisions, is set to create strong future growth in green lending and related fee-based income streams, directly benefiting revenue diversification and topline growth.

Want to know what’s driving this call? The fair value leans on some bold profit margin and topline assumptions, plus an unexpected factor for future growth. Uncover the financial story the analysts believe will determine where this bank trades next.

Result: Fair Value of €26.98 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent regulatory scrutiny and pressure from fintech rivals could quickly dampen growth expectations and challenge the bullish outlook for ABN AMRO.

Find out about the key risks to this ABN AMRO Bank narrative.

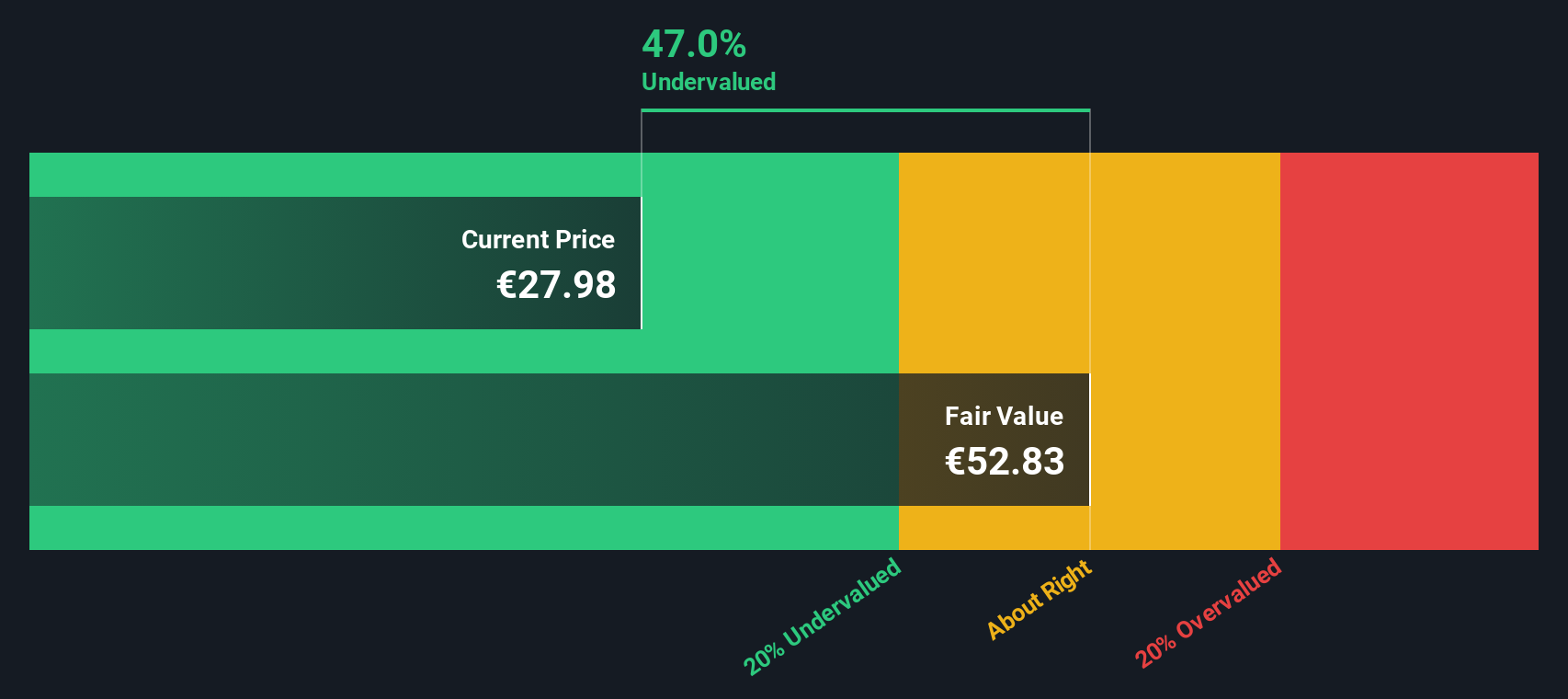

Another View: Discounted Cash Flow Paints a Different Picture

While many analysts believe ABN AMRO is either close to fair value or slightly overvalued after its recent rally, our DCF model sees things differently. By estimating future cash flows, the SWS DCF approach suggests ABN AMRO could be significantly undervalued. This raises the question: have market expectations missed a deeper value story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ABN AMRO Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 865 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ABN AMRO Bank Narrative

If you see the numbers differently, or prefer to form your own view, you can generate a personal narrative about ABN AMRO in just a few minutes. Do it your way.

A great starting point for your ABN AMRO Bank research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors always keep their options open. Take advantage of these unique opportunities. If you wait, you might miss the next winning stock story.

- Capture tomorrow’s growth with these 25 AI penny stocks, offering cutting-edge exposure to intelligent automation and advanced software trends.

- Secure a steady stream of income by reviewing these 14 dividend stocks with yields > 3% for companies with strong yields delivering consistent shareholder rewards above the market average.

- Boost your portfolio with these 3574 penny stocks with strong financials, primed for big potential and the strongest fundamentals among undervalued small-cap names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ABN

ABN AMRO Bank

Provides various banking products and financial services to retail, private, and business clients in the Netherlands, rest of Europe, the United States, Asia, and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor