Advertisement

We Think Shareholders May Want To Consider A Review Of Woodlandor Holdings Berhad's (KLSE:WOODLAN) CEO Compensation Package

Key Insights

- Woodlandor Holdings Berhad's Annual General Meeting to take place on 8th of December

- Total pay for CEO Weng Mun includes RM264.0k salary

- Total compensation is similar to the industry average

- Over the past three years, Woodlandor Holdings Berhad's EPS fell by 28% and over the past three years, the total loss to shareholders 23%

Woodlandor Holdings Berhad (KLSE:WOODLAN) has not performed well recently and CEO Weng Mun will probably need to up their game. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 8th of December. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for Woodlandor Holdings Berhad

How Does Total Compensation For Weng Mun Compare With Other Companies In The Industry?

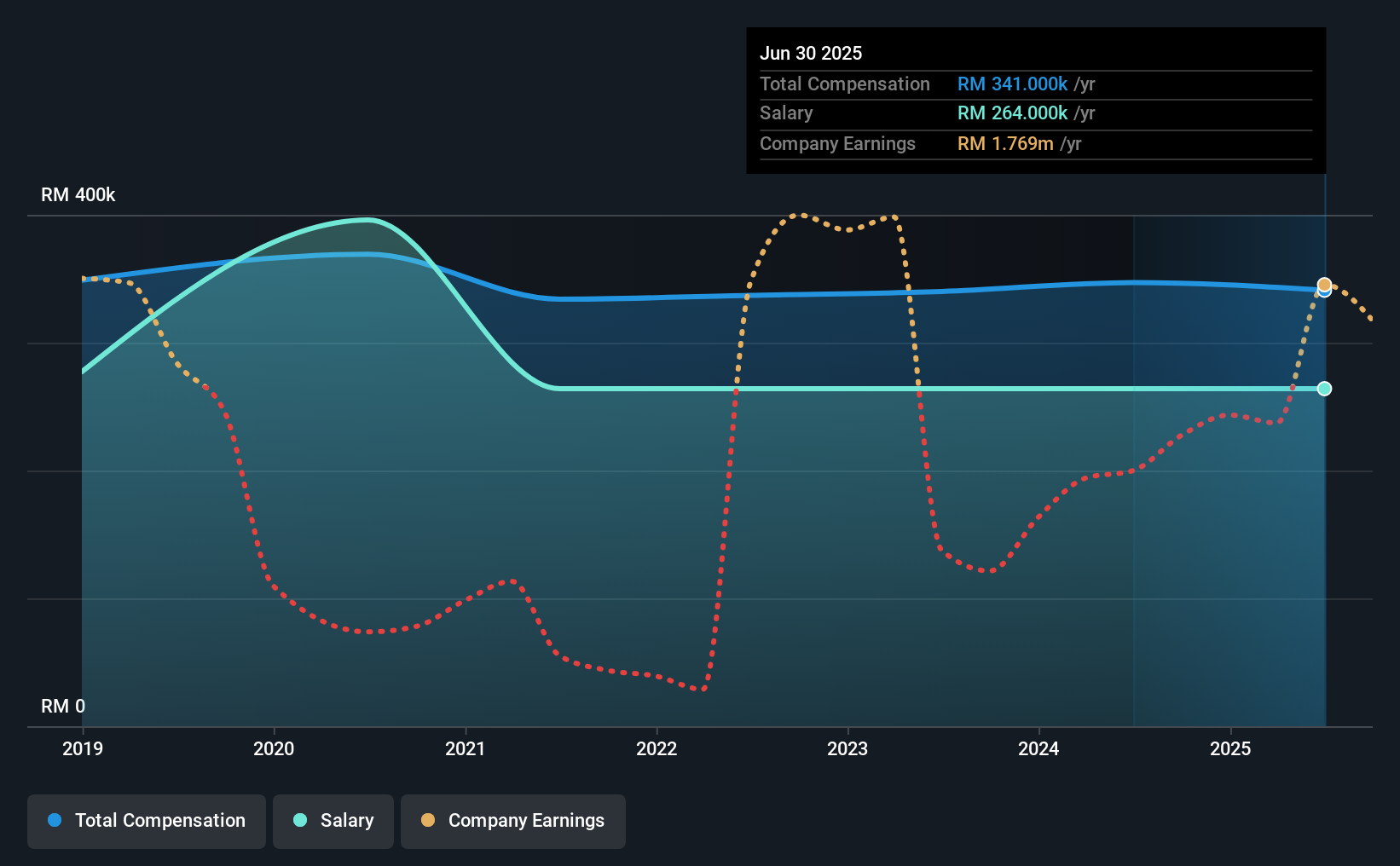

According to our data, Woodlandor Holdings Berhad has a market capitalization of RM23m, and paid its CEO total annual compensation worth RM341k over the year to June 2025. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at RM264.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Malaysia Building industry with market capitalizations below RM825m, we found that the median total CEO compensation was RM340k. This suggests that Woodlandor Holdings Berhad remunerates its CEO largely in line with the industry average. Moreover, Weng Mun also holds RM4.2m worth of Woodlandor Holdings Berhad stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | RM264k | RM264k | 77% |

| Other | RM77k | RM83k | 23% |

| Total Compensation | RM341k | RM347k | 100% |

On an industry level, around 80% of total compensation represents salary and 20% is other remuneration. Although there is a difference in how total compensation is set, Woodlandor Holdings Berhad more or less reflects the market in terms of setting the salary. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Woodlandor Holdings Berhad's Growth

Woodlandor Holdings Berhad has reduced its earnings per share by 28% a year over the last three years. Its revenue is down 1.7% over the previous year.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Woodlandor Holdings Berhad Been A Good Investment?

With a three year total loss of 23% for the shareholders, Woodlandor Holdings Berhad would certainly have some dissatisfied shareholders. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We did our research and identified 2 warning signs (and 1 which makes us a bit uncomfortable) in Woodlandor Holdings Berhad we think you should know about.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Woodlandor Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:WOODLAN

Woodlandor Holdings Berhad

An investment holding company, develops and produces wood-based products for the building and construction industry primarily in Malaysia and internationally.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Weekly Picks

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

TI

TibiT on Canadian National Railway ·

The Indispensable Artery for a New North American Economy

Fair Value:CA$132.870.7% overvalued

20 followersusers have followed this narrative

4 commentsusers have commented on this narrative

3 likesusers have liked this narrative

RE

RecMag on Agfa-Gevaert ·

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Fair Value:€5.3988.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative