The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Berjaya Corporation Berhad (KLSE:BJCORP) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Berjaya Corporation Berhad

What Is Berjaya Corporation Berhad's Net Debt?

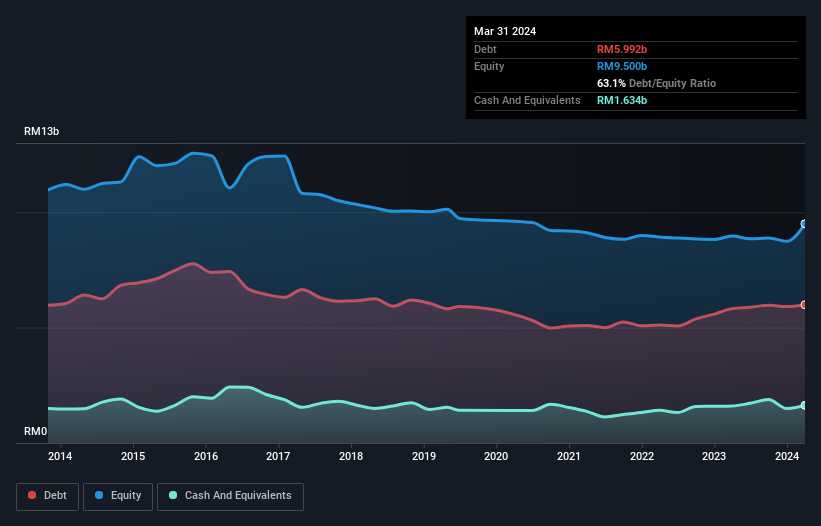

As you can see below, Berjaya Corporation Berhad had RM5.99b of debt, at March 2024, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of RM1.63b, its net debt is less, at about RM4.36b.

How Strong Is Berjaya Corporation Berhad's Balance Sheet?

The latest balance sheet data shows that Berjaya Corporation Berhad had liabilities of RM6.33b due within a year, and liabilities of RM6.89b falling due after that. Offsetting these obligations, it had cash of RM1.63b as well as receivables valued at RM3.05b due within 12 months. So its liabilities total RM8.54b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the RM1.84b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Berjaya Corporation Berhad would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Berjaya Corporation Berhad has a debt to EBITDA ratio of 4.9, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 1k is very high, suggesting that the interest expense on the debt is currently quite low. If Berjaya Corporation Berhad can keep growing EBIT at last year's rate of 16% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But it is Berjaya Corporation Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Berjaya Corporation Berhad produced sturdy free cash flow equating to 80% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

While Berjaya Corporation Berhad's level of total liabilities has us nervous. To wit both its interest cover and conversion of EBIT to free cash flow were encouraging signs. Looking at all the angles mentioned above, it does seem to us that Berjaya Corporation Berhad is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Berjaya Corporation Berhad that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Berjaya Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BJCORP

Berjaya Corporation Berhad

Provides consumer marketing, direct selling, and retailing services.

Low and slightly overvalued.