Advertisement

- South Korea

- /

- Semiconductors

- /

- KOSE:A000660

Is SK hynix Still Trading at a Discount After Its 217% Price Surge?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if SK hynix's stock is still a bargain or if you've already missed the boat? You're not alone, and a closer look at its valuation might just surprise you.

- After years of stellar gains, with a whopping 217.8% jump year-to-date and 241.2% over the past year, SK hynix's recent 4.7% slip this week and 4.4% gain over the last month show that momentum comes with a dose of volatility.

- Big moves in semiconductor stocks are not happening in a vacuum, and SK hynix has been in the headlines lately thanks to global chip demand, supply chain updates, and AI-driven optimism. These factors have fueled a rush of investor interest, shifting perceptions of both the company's growth potential and its risks.

- When we run SK hynix through our valuation checks, it scores a strong 5 out of 6, hinting that value might still be on offer. Up next, we will break down how we reach that score using different valuation methods. Stick around, because by the end, you will discover an even better way to understand what SK hynix is really worth.

Approach 1: SK hynix Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s worth by calculating the present value of all expected future cash flows. It essentially projects how much cash SK hynix will generate and discounts this amount back to today’s value. This approach is widely used because it focuses on the underlying cash that shareholders could ultimately receive.

For SK hynix, recent data shows the company generated ₩20.85 billion in Free Cash Flow over the last twelve months. Analysts forecast meaningful growth, projecting Free Cash Flow to reach ₩37.24 billion by 2026 and ₩48.42 billion by 2027. Further out, projections extend over the next decade, with estimates growing to ₩94.18 billion by 2035. It’s important to note that only the next few years are based on direct analyst estimates. Anything beyond is extrapolated by Simply Wall St’s model.

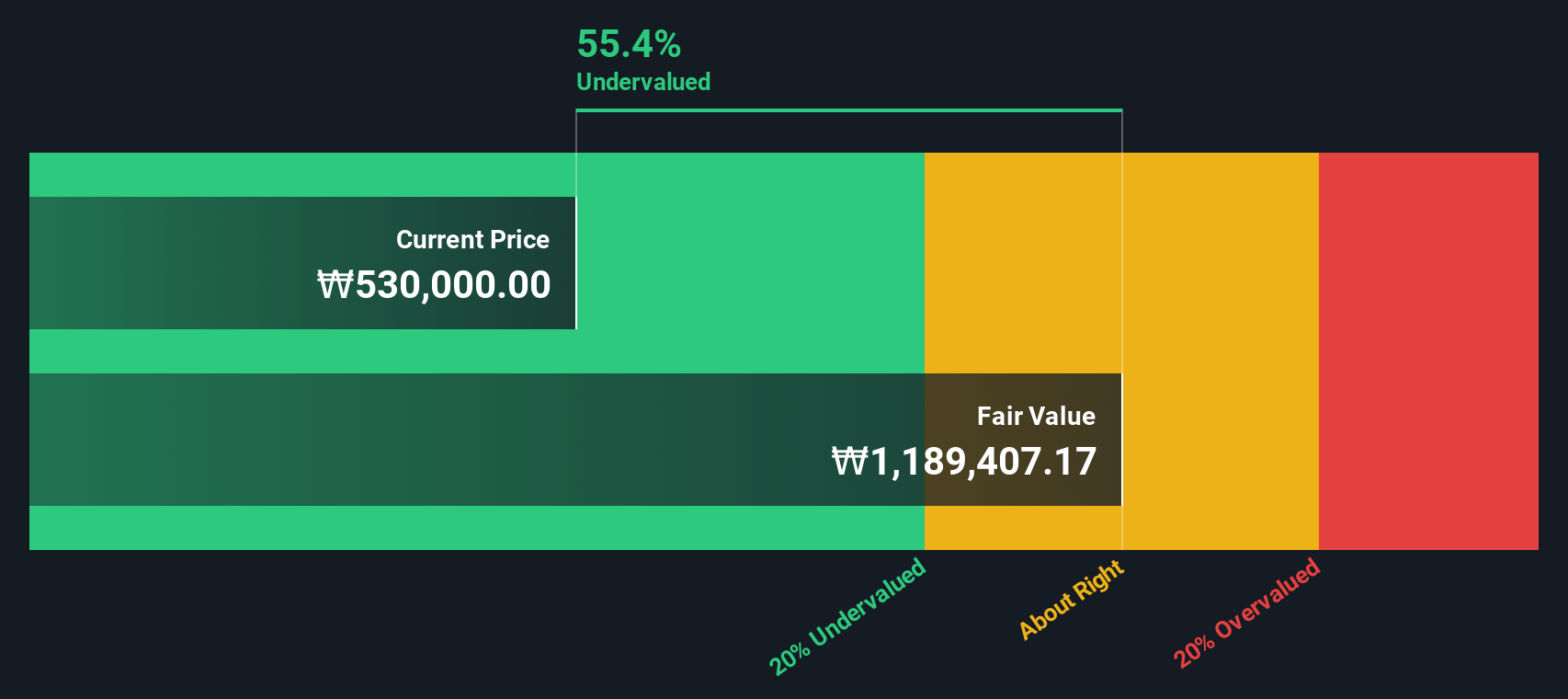

Based on these cash flow projections and discounting them using a 2 Stage Free Cash Flow to Equity approach, SK hynix’s intrinsic value comes out to ₩1,189,407 per share. This is a 54.3% discount compared to the current share price, making the stock appear significantly undervalued at today’s levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests SK hynix is undervalued by 54.3%. Track this in your watchlist or portfolio, or discover 928 more undervalued stocks based on cash flows.

Approach 2: SK hynix Price vs Earnings

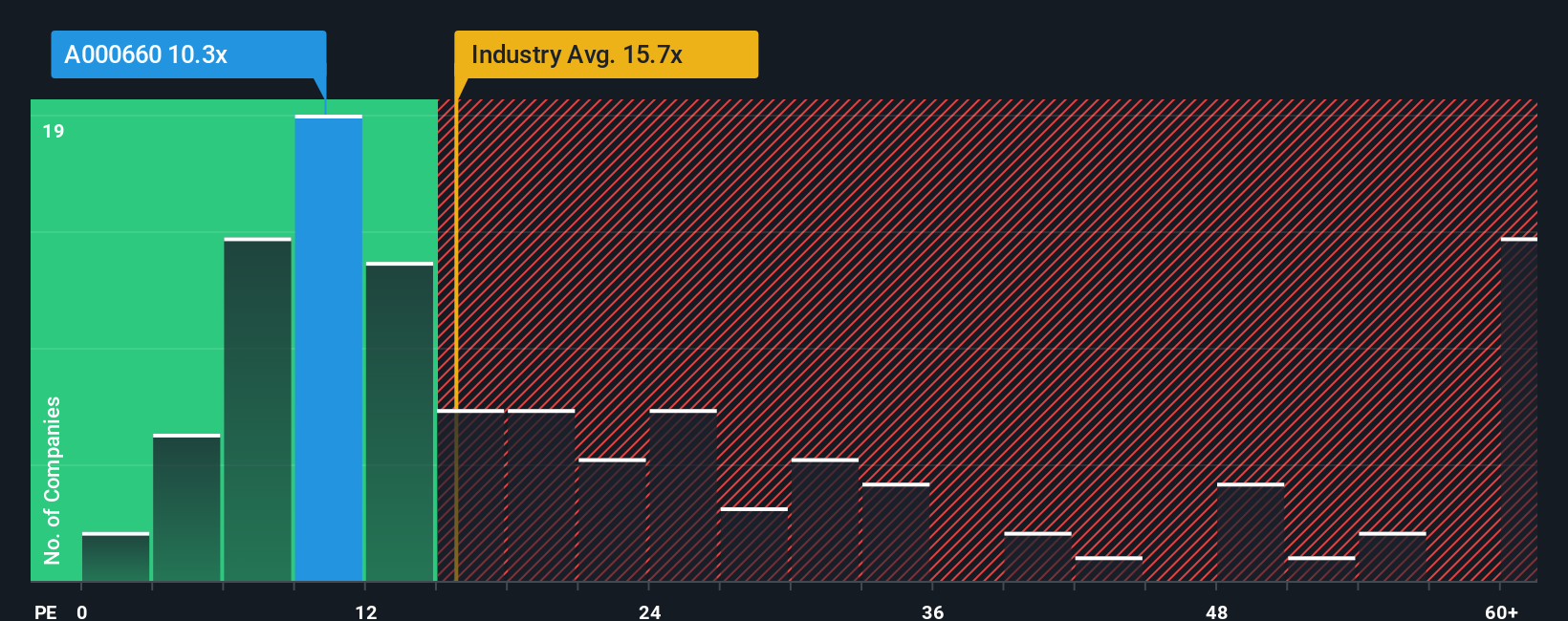

The Price-to-Earnings (PE) ratio is a popular valuation metric for profitable companies like SK hynix because it measures how much investors are willing to pay for each won the company earns. It's a quick way to see whether the market thinks SK hynix’s current profits justify its share price. This makes it ideal for large, established businesses generating positive earnings.

Of course, the "right" PE ratio is rarely set in stone. High growth prospects and lower risk often mean investors are willing to pay a higher PE, while companies facing slower growth or more risks usually trade at a discount. So, context matters. Comparing a company's PE to meaningful benchmarks is essential.

Currently, SK hynix trades at a PE of 10.5x. That is lower than both the Semiconductor industry average of 15.7x and its peer group average of 26.2x. At first glance, SK hynix looks attractively valued, but averages do not always tell the full story.

This is where Simply Wall St’s “Fair Ratio” comes in. It is a proprietary metric that estimates what SK hynix’s PE ratio should be, based on its actual earnings growth, risk profile, profit margins, market cap, and industry. This approach goes deeper than simple peer or industry averages, offering a more tailored view of value.

For SK hynix, the Fair Ratio is calculated at 40.0x, much higher than the current PE. This suggests that when you properly account for the company’s fundamentals and prospects, SK hynix is trading well below what would be expected.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your SK hynix Narrative

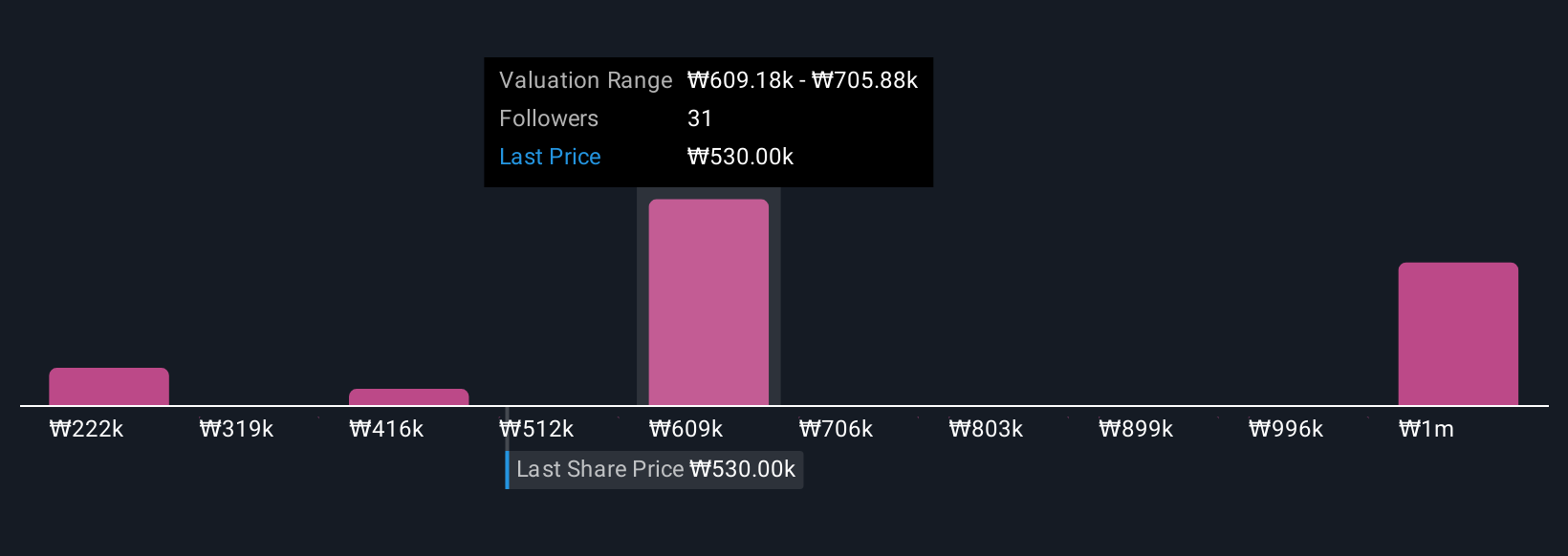

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. In simple terms, a Narrative is your own story or perspective about a company, a set of assumptions about SK hynix’s future revenue, earnings, and margins that you connect to a projected fair value. Unlike just looking at numbers, Narratives let you explain the “why” behind your forecast, linking SK hynix's business story directly to a financial outlook and what you believe the shares are truly worth.

Narratives are intuitive and accessible. They are available to everyone on Simply Wall St's Community page and are used by millions of investors. By building a Narrative, you can easily see whether your fair value is above or below the current market price, helping you decide when to consider buying or selling. Plus, Narratives update automatically when new earnings, news, or industry shifts happen, so your investment outlook adapts as the facts change.

For example, with SK hynix, some investors might believe that next-generation memory and strong AI partnerships will drive future profits and assign a high fair value. Others might focus on risks such as geopolitical uncertainty and assign a more conservative value. Narratives give you a transparent, dynamic way to see and test different viewpoints, all in one place.

Do you think there's more to the story for SK hynix? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A000660

SK hynix

Manufactures, distributes, and sells semiconductor products in Korea, China, rest of Asia, the United States, and Europe.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative