- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A240810

3 KRX Stocks Estimated To Be Trading Below Intrinsic Value In September 2024

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has risen 1.2%, while it has remained flat over the past 12 months. With earnings forecast to grow by 29% annually, identifying stocks trading below their intrinsic value can offer significant opportunities for investors looking to capitalize on future growth potential.

Top 10 Undervalued Stocks Based On Cash Flows In South Korea

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| APR (KOSE:A278470) | ₩266000.00 | ₩523226.89 | 49.2% |

| VIOL (KOSDAQ:A335890) | ₩8880.00 | ₩17741.24 | 49.9% |

| T'Way Air (KOSE:A091810) | ₩3115.00 | ₩5742.21 | 45.8% |

| TSE (KOSDAQ:A131290) | ₩51300.00 | ₩97716.05 | 47.5% |

| Lutronic (KOSDAQ:A085370) | ₩36700.00 | ₩63217.94 | 41.9% |

| Oscotec (KOSDAQ:A039200) | ₩34300.00 | ₩65583.14 | 47.7% |

| ABCO Electronics (KOSDAQ:A036010) | ₩6120.00 | ₩11538.47 | 47% |

| Global Tax Free (KOSDAQ:A204620) | ₩3565.00 | ₩6414.11 | 44.4% |

| Shinsung E&GLtd (KOSE:A011930) | ₩1733.00 | ₩3016.08 | 42.5% |

| Hotel ShillaLtd (KOSE:A008770) | ₩47650.00 | ₩82736.50 | 42.4% |

Let's review some notable picks from our screened stocks.

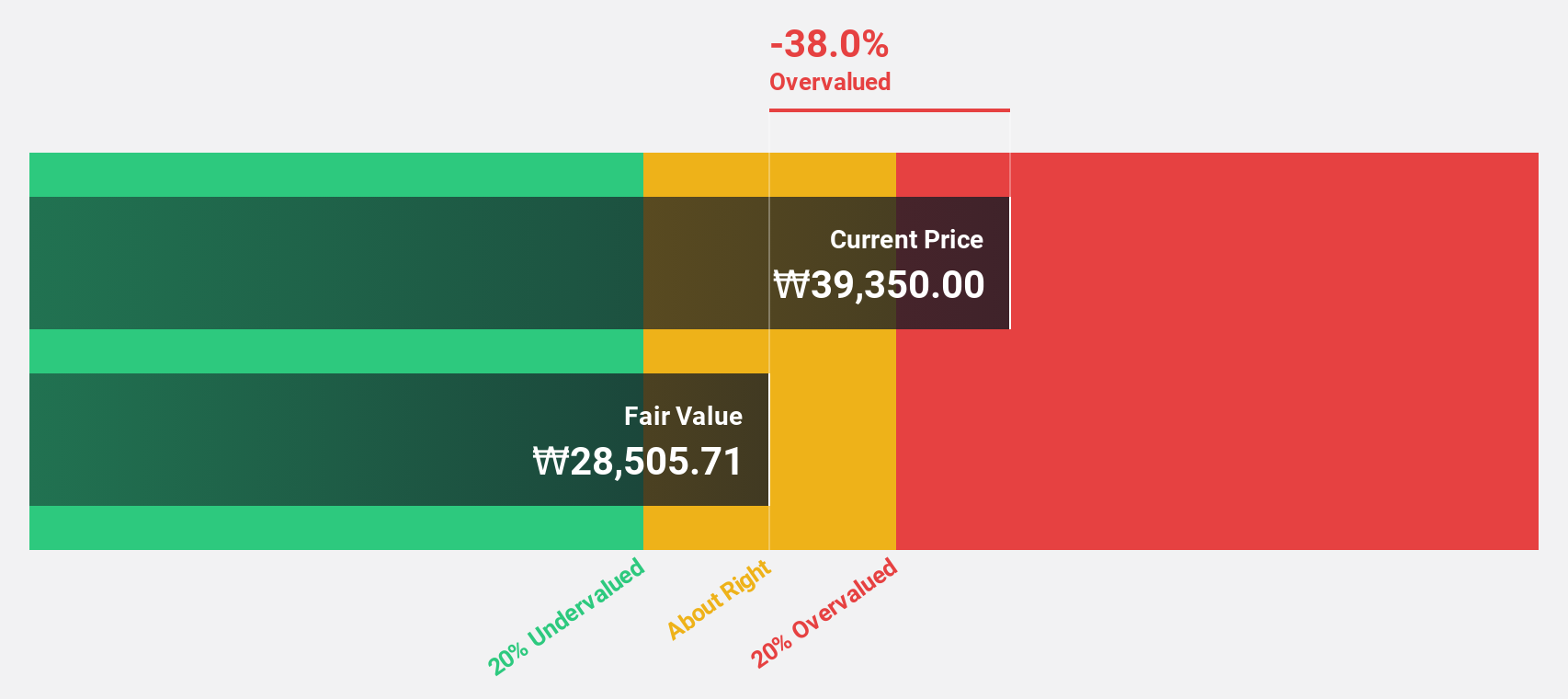

TSE (KOSDAQ:A131290)

Overview: TSE Co., Ltd offers semiconductor test solutions both in South Korea and internationally, with a market cap of ₩548.11 billion.

Operations: The company's revenue is primarily derived from semiconductor light inspection equipment (₩160.25 billion), electronic product inspection (₩112.77 billion), semiconductors and related production lines (₩21.04 billion), and semiconductor inspection services (₩13.67 billion).

Estimated Discount To Fair Value: 47.5%

TSE is trading at ₩51,300, significantly below its estimated fair value of ₩97,716.05. Despite recent high volatility in share price, the company shows strong cash flow potential with earnings forecasted to grow 48.3% annually over the next three years, outpacing the Korean market's growth rate of 29.3%. Revenue is also expected to increase by 13.5% per year, exceeding the market average of 10.5%.

- According our earnings growth report, there's an indication that TSE might be ready to expand.

- Navigate through the intricacies of TSE with our comprehensive financial health report here.

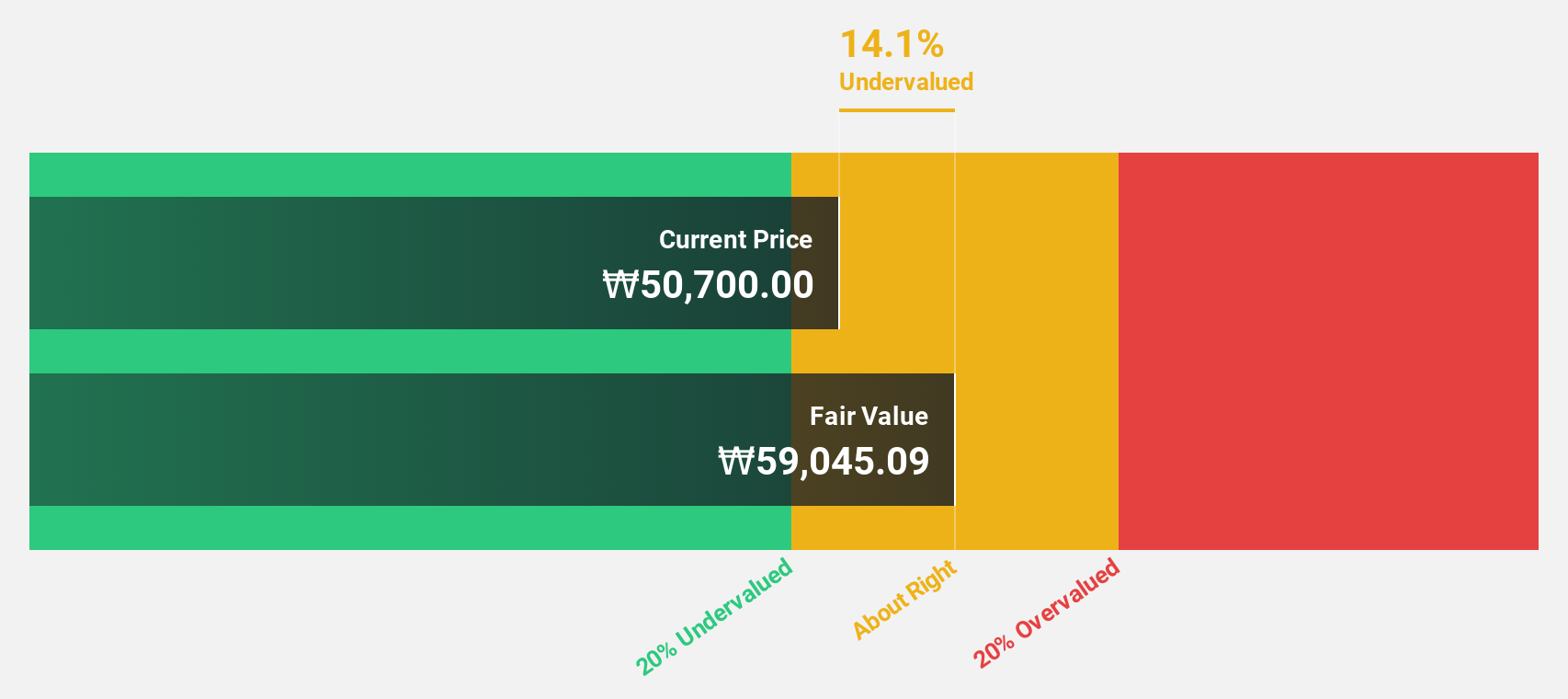

Wonik Ips (KOSDAQ:A240810)

Overview: Wonik IPS Co., Ltd researches, develops, manufactures, and sells semiconductor, display, and solar cell systems in South Korea with a market cap of ₩1.54 trillion.

Operations: Revenue segments for Wonik IPS Co., Ltd include the Semiconductor Equipment Division, which generated ₩687.21 billion.

Estimated Discount To Fair Value: 28.7%

Wonik Ips is trading at ₩31,550, below its estimated fair value of ₩44,249.67. The company's revenue is forecast to grow 20.5% annually, outpacing the Korean market's 10.5%. Earnings are expected to increase by 90.24% per year, with profitability anticipated within three years, reflecting above-average market growth. Analysts predict a potential stock price rise of 40.5%, highlighting significant undervaluation based on discounted cash flow analysis ahead of their Q2 results on Aug 08, 2024.

- The analysis detailed in our Wonik Ips growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Wonik Ips.

Hotel ShillaLtd (KOSE:A008770)

Overview: Hotel Shilla Co.,Ltd operates as a hospitality company in South Korea and internationally, with a market cap of ₩1.80 trillion.

Operations: Hotel Shilla's revenue segments include Travel Retail (₩3.31 trillion) and Hotel & Leisure Sector (₩701.77 billion).

Estimated Discount To Fair Value: 42.4%

Hotel Shilla Ltd. is trading at ₩47,650, significantly below its estimated fair value of ₩82,736.50. The company is expected to achieve revenue growth of 11.7% annually and become profitable within three years, outpacing the market average. Despite low forecasted return on equity (16.8%) and interest payments not being well covered by earnings, it remains highly undervalued based on discounted cash flow analysis following a recent private placement raising KRW 132.80 billion in exchangeable bonds with a 0% interest rate.

- Our comprehensive growth report raises the possibility that Hotel ShillaLtd is poised for substantial financial growth.

- Get an in-depth perspective on Hotel ShillaLtd's balance sheet by reading our health report here.

Make It Happen

- Explore the 35 names from our Undervalued KRX Stocks Based On Cash Flows screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wonik Ips might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A240810

Wonik Ips

Wonik IPS Co., Ltd primarily researches and develops, manufactures, and sells semiconductor, display, and solar cell systems in South Korea.

Flawless balance sheet and undervalued.