- South Korea

- /

- Pharma

- /

- KOSE:A003850

Exploring Snt DynamicsLtd And 2 Other Hidden Small Caps in South Korea

Reviewed by Simply Wall St

The South Korea stock market has moved higher in four straight sessions, improving almost 80 points or 3.1 percent along the way. The KOSPI now sits just above the 2,590-point plateau although investors may lock in gains on Monday. In this dynamic environment, identifying promising small-cap stocks can be particularly rewarding for investors seeking growth opportunities. This article explores Snt Dynamics Ltd and two other hidden gems that could offer significant potential in South Korea's evolving market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Korea Cast Iron Pipe Ind | NA | 1.97% | 8.84% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| NOROO PAINT & COATINGS | 13.99% | 5.04% | 7.74% | ★★★★★★ |

| Korea Ratings | NA | 1.13% | 0.54% | ★★★★★★ |

| Synergy Innovation | 12.39% | 12.87% | 28.82% | ★★★★★★ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| ASIA Holdings | 34.98% | 8.43% | 16.17% | ★★★★★☆ |

| Oriental Precision & EngineeringLtd | 54.53% | 3.14% | 0.80% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.28% | ★★★★★☆ |

| FnGuide | 36.10% | 8.92% | 10.27% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Snt DynamicsLtd (KOSE:A003570)

Simply Wall St Value Rating: ★★★★★★

Overview: Snt Dynamics Co., Ltd. manufactures and sells precision machinery with a market cap of ₩576.64 billion.

Operations: Snt Dynamics generates revenue primarily from its Machinery Business (₩5.21 billion) and Transportation Equipment Business (₩555.04 billion).

SNT Dynamics Ltd. has demonstrated impressive earnings growth of 184.7% over the past year, significantly outpacing the Aerospace & Defense industry’s 47.9%. Trading at 68.9% below its estimated fair value, it offers substantial upside potential. The company reported a net income of KRW 47 billion in Q2 2024, up from KRW 8.98 billion a year ago, with basic earnings per share rising to KRW 2,100 from KRW 401. Notably, SNT Dynamics remains debt-free and is free cash flow positive.

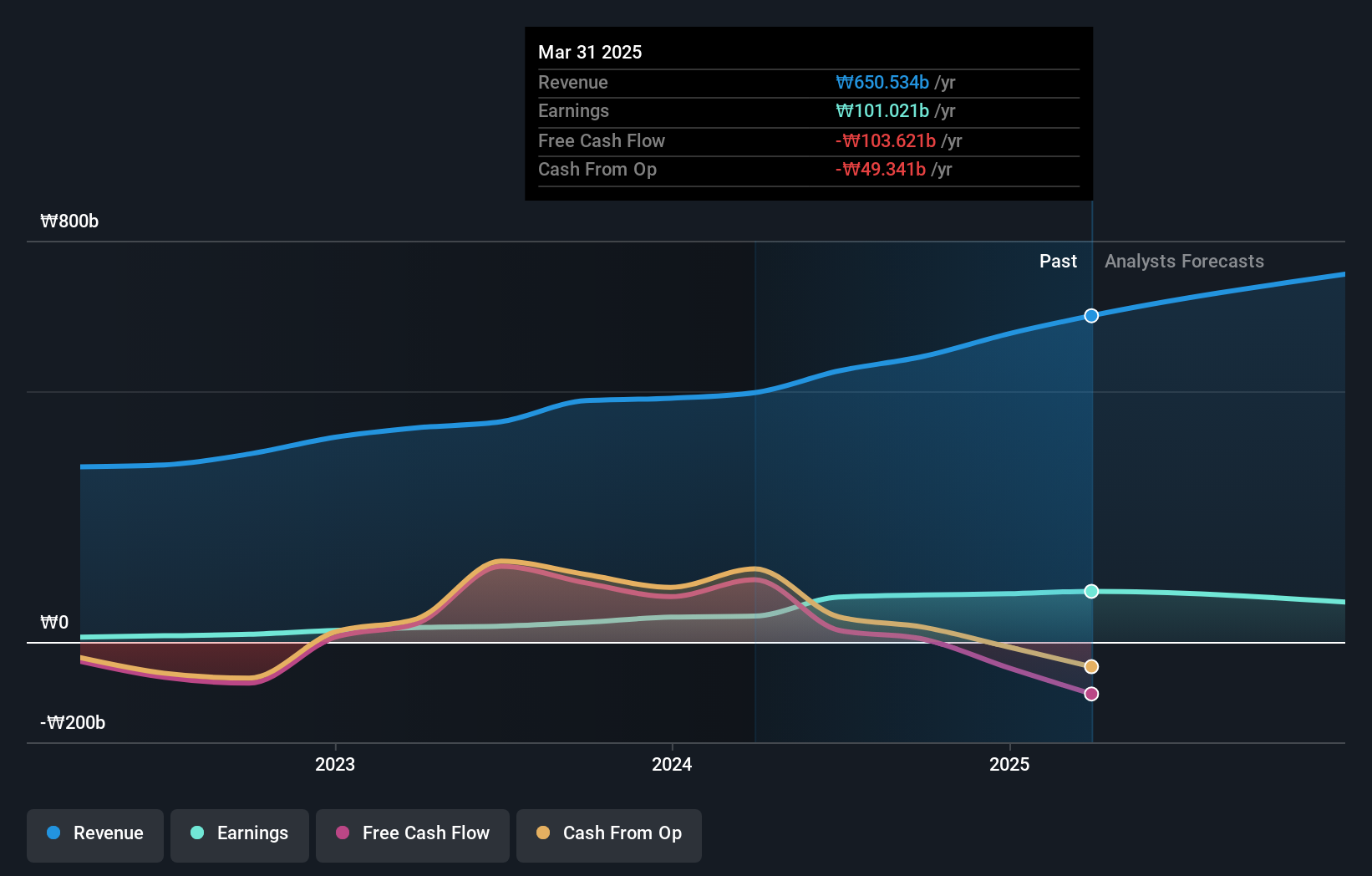

Boryung (KOSE:A003850)

Simply Wall St Value Rating: ★★★★★★

Overview: Boryung Corporation engages in the manufacture and sale of pharmaceutical products in South Korea and internationally, with a market cap of ₩809.49 billion.

Operations: Boryung Corporation generates its revenue primarily from pharmaceutical manufacturing and sales, amounting to ₩928.72 billion. The company focuses on this single revenue stream without segmentation into other areas.

Boryung's recent performance has been impressive, with earnings for the second quarter reaching KRW 23.64 million, up from KRW 11.32 million last year. Sales also surged to KRW 228.62 million compared to KRW 80.13 million previously. Basic earnings per share jumped to KRW 359 from KRW 172 a year ago, indicating robust growth in profitability and operational efficiency within the pharmaceutical sector over the past year.

- Navigate through the intricacies of Boryung with our comprehensive health report here.

Assess Boryung's past performance with our detailed historical performance reports.

Iljin ElectricLtd (KOSE:A103590)

Simply Wall St Value Rating: ★★★★★★

Overview: Iljin Electric Co., Ltd operates as a heavy electric machinery company in South Korea and internationally, with a market cap of ₩1.05 trillion.

Operations: Iljin Electric generates revenue primarily from its Wire segment (₩1.17 trillion) and Power System segment (₩329.01 billion), with consolidated adjustments amounting to -₩81.32 billion.

Iljin Electric Ltd. has demonstrated impressive earnings growth of 55.6% over the past year, outpacing the Electrical industry’s 18.5%. The company’s net debt to equity ratio stands at a satisfactory 10.4%, reflecting prudent financial management, while its interest payments are well covered by EBIT with a coverage ratio of 9.1x. Despite recent share price volatility, Iljin is trading at an attractive valuation—83% below estimated fair value—and forecasts suggest continued earnings growth of 34.63% annually.

- Take a closer look at Iljin ElectricLtd's potential here in our health report.

Understand Iljin ElectricLtd's track record by examining our Past report.

Seize The Opportunity

- Unlock our comprehensive list of 189 KRX Undiscovered Gems With Strong Fundamentals by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boryung might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A003850

Boryung

Engages in the manufacture and sale of pharmaceutical products in South Korea and internationally.

Flawless balance sheet and undervalued.