- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A033240

KRX Growth Companies With High Insider Ownership For September 2024

Reviewed by Simply Wall St

The South Korea stock market has moved higher in four straight sessions, improving almost 80 points or 3.1 percent along the way. The KOSPI now sits just above the 2,590-point plateau although investors may lock in gains on Monday. In this buoyant market environment, identifying growth companies with high insider ownership can be particularly beneficial for investors seeking to align their interests with those of company insiders who have a significant stake in the business.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.5% | 52.1% |

| Bioneer (KOSDAQ:A064550) | 15.8% | 97.6% |

| Park Systems (KOSDAQ:A140860) | 33% | 35.7% |

| Oscotec (KOSDAQ:A039200) | 26.3% | 122% |

| Vuno (KOSDAQ:A338220) | 19.5% | 110.9% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 100.3% |

| INTEKPLUS (KOSDAQ:A064290) | 16.3% | 96.7% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

| Techwing (KOSDAQ:A089030) | 18.7% | 83.6% |

Here we highlight a subset of our preferred stocks from the screener.

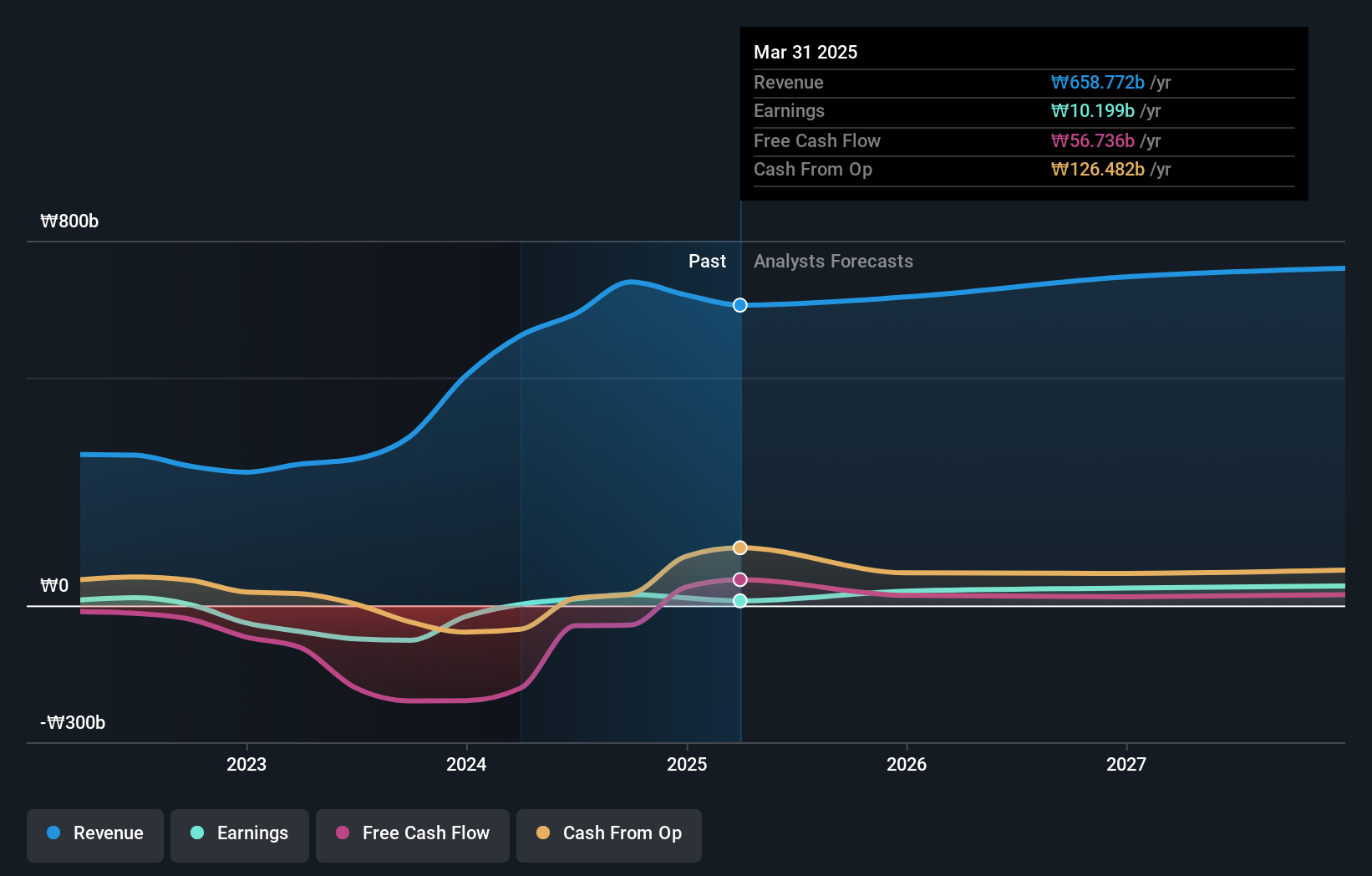

Jahwa Electronics (KOSE:A033240)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jahwa Electronics Co., Ltd manufactures and sells precision electronic components in South Korea and internationally, with a market cap of ₩369.20 billion.

Operations: The company's revenue from manufacturing and sales of mobile phone parts and other electronic components is ₩639.33 billion.

Insider Ownership: 22.4%

Earnings Growth Forecast: 39.1% p.a.

Jahwa Electronics, a South Korean company with high insider ownership, has shown promising growth prospects. The company recently became profitable and its earnings are forecast to grow significantly at 39.12% per year over the next three years, outpacing the market's 29% annual growth rate. Additionally, revenue is expected to increase by 15.6% annually, faster than the overall KR market's 10.4%. However, its Return on Equity is projected to be relatively low at 12.3%.

- Navigate through the intricacies of Jahwa Electronics with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Jahwa Electronics' current price could be inflated.

Foosung (KOSE:A093370)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Foosung Co., Ltd. and its subsidiaries manufacture and sell chemical products for various industries including automotive, iron and steel, semiconductor, construction, and environmental sectors in South Korea, with a market cap of ₩644.60 billion.

Operations: Foosung's revenue segments include Chemical Equipment (₩167.17 billion) and Fluorine Compounds (₩300.83 billion).

Insider Ownership: 32.9%

Earnings Growth Forecast: 72.6% p.a.

Foosung, a South Korean company with high insider ownership, has demonstrated significant growth. Its revenue is forecast to grow at 15.5% per year, outpacing the market's 10.4%. Earnings are expected to increase by 72.64% annually, and the company is projected to become profitable within three years. Recent earnings reports show substantial improvement with Q2 sales reaching ₩956.59 million and net income at ₩14,428.32 million compared to a loss last year.

- Take a closer look at Foosung's potential here in our earnings growth report.

- The analysis detailed in our Foosung valuation report hints at an inflated share price compared to its estimated value.

Solum (KOSE:A248070)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Solum Co., Ltd. manufactures and markets power modules, digital tuners, and electronic shelf labels to customers in South Korea and internationally, with a market cap of ₩979.18 billion.

Operations: The company's revenue segments include the ICT Business, generating ₩470.84 million, and the Electronic Components Division, contributing ₩1.16 billion.

Insider Ownership: 16.6%

Earnings Growth Forecast: 36.8% p.a.

Solum, a South Korean company with high insider ownership, is expected to see significant earnings growth of 36.8% per year over the next three years, outpacing the market's 29%. Revenue is forecast to grow at 14.3% annually. Despite trading at 61% below its estimated fair value and having a high debt level, Solum has announced a KRW 20 billion share repurchase program aimed at stabilizing stock prices and enhancing shareholder value.

- Click here and access our complete growth analysis report to understand the dynamics of Solum.

- Our expertly prepared valuation report Solum implies its share price may be lower than expected.

Taking Advantage

- Reveal the 88 hidden gems among our Fast Growing KRX Companies With High Insider Ownership screener with a single click here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A033240

Jahwa Electronics

Manufactures and sells precision electronic components in South Korea and internationally.

Reasonable growth potential with adequate balance sheet.