- South Korea

- /

- Industrials

- /

- KOSE:A000150

Swelling losses haven't held back gains for Doosan (KRX:000150) shareholders since they're up 202% over 3 years

The most you can lose on any stock (assuming you don't use leverage) is 100% of your money. But when you pick a company that is really flourishing, you can make more than 100%. For instance the Doosan Corporation (KRX:000150) share price is 186% higher than it was three years ago. How nice for those who held the stock! Also pleasing for shareholders was the 59% gain in the last three months. The company reported its financial results recently; you can catch up on the latest numbers by reading our company report.

Since the long term performance has been good but there's been a recent pullback of 8.8%, let's check if the fundamentals match the share price.

See our latest analysis for Doosan

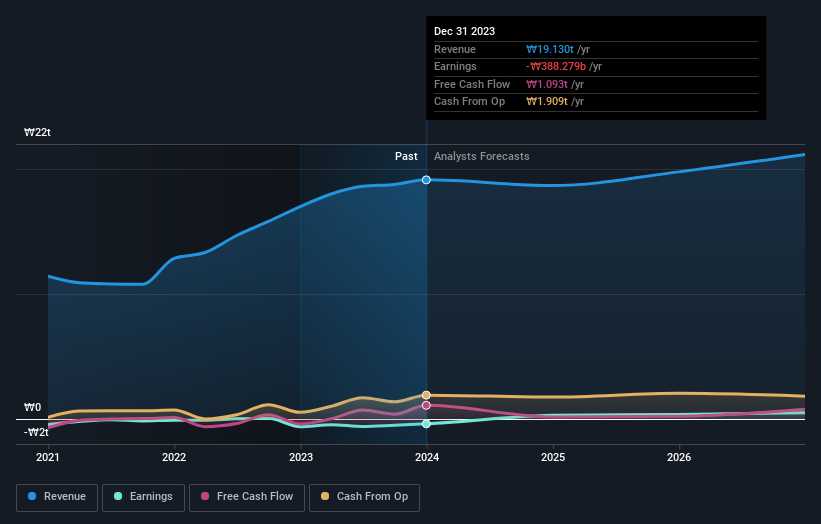

Doosan isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last 3 years Doosan saw its revenue grow at 22% per year. That's much better than most loss-making companies. Meanwhile, the share price performance has been pretty solid at 42% compound over three years. But it does seem like the market is paying attention to strong revenue growth. Nonetheless, we'd say Doosan is still worth investigating - successful businesses can often keep growing for long periods.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Doosan's TSR for the last 3 years was 202%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

It's good to see that Doosan has rewarded shareholders with a total shareholder return of 50% in the last twelve months. That's including the dividend. That's better than the annualised return of 13% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. It's always interesting to track share price performance over the longer term. But to understand Doosan better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Doosan , and understanding them should be part of your investment process.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A000150

Doosan

Engages in the heavy industry, machinery manufacturing, and apartment construction businesses in South Korea, the United States, rest of Asia, the Middle East, Europe, and internationally.

Excellent balance sheet and good value.