Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6787

Assessing Meiko Electronics (TSE:6787) Valuation Following Board-Approved Dividend Increase

Simply Wall St

Reviewed by Simply Wall St

Meiko Electronics (TSE:6787) just approved a dividend increase, raising its payout to JPY 45.00 per share from JPY 40.00 last year. The Board’s decision, announced on October 27, reflects growing confidence in its financial outlook.

See our latest analysis for Meiko Electronics.

The dividend hike seems to have energized investor sentiment, as Meiko Electronics' share price has climbed over 7% in the past month and is up nearly 36% in the last three months. Looking longer-term, the story is even stronger. Meiko delivered a remarkable 80% total shareholder return over the past year and nearly 500% over five years, highlighting solid momentum that could hint at further growth potential as confidence builds.

If Meiko’s impressive returns have you wondering what else is emerging, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With such strong momentum and a newly increased dividend, the key question now is whether Meiko Electronics still offers value, or if the market has already priced in all the company’s future growth potential.

Price-to-Earnings of 17.1x: Is it justified?

Meiko Electronics is currently trading at a price-to-earnings (P/E) ratio of 17.1x, putting the spotlight on how the market values its recent growth against peers. The last close was ¥10,210, but is this price supported by earnings?

The price-to-earnings ratio measures how much investors are willing to pay for each yen of earnings. It is especially important for growth companies and cyclical sectors like electronics. A higher ratio often reflects optimism about future profits, while a lower one can signal caution or undervaluation.

Meiko’s P/E of 17.1x is above the Japanese Electronic industry average of 15.2x. This suggests the market expects more robust growth from Meiko than from many of its rivals. However, the ratio is below the peer average of 18.8x, making it look attractive compared to close competitors. Notably, the P/E remains well below the estimated fair P/E ratio of 21.5x, so there is a possibility for further re-rating if Meiko sustains its strong earnings trend.

Explore the SWS fair ratio for Meiko Electronics

Result: Price-to-Earnings of 17.1x (ABOUT RIGHT)

However, slowing revenue or earnings growth could dampen sentiment and limit upside, especially if global tech markets face renewed volatility.

Find out about the key risks to this Meiko Electronics narrative.

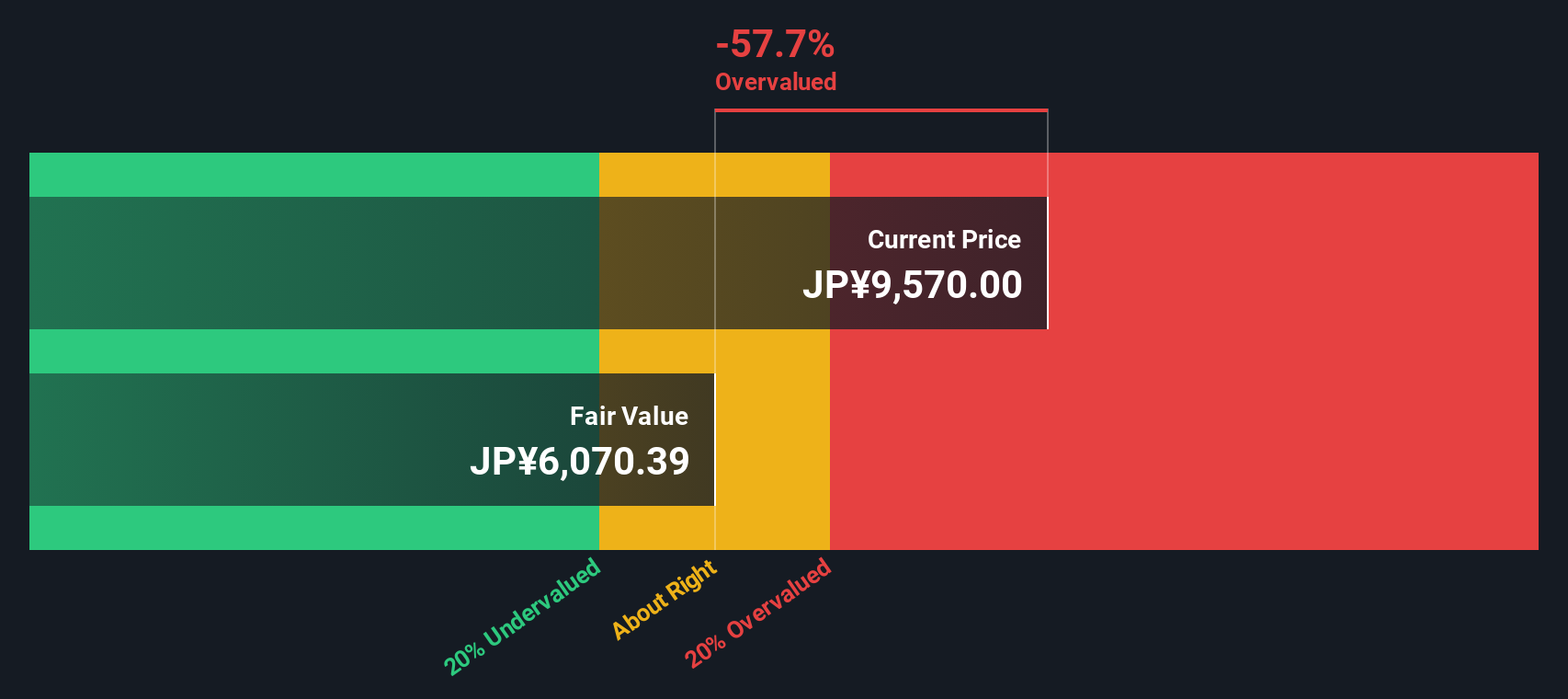

Another View: Discounted Cash Flow Model

While the current valuation based on earnings multiples looks reasonable, the SWS DCF model offers a more cautious perspective. According to this cash flow-based approach, Meiko Electronics is actually trading well above our estimate of fair value. This highlights the risk of relying on only one method.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Meiko Electronics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 832 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Meiko Electronics Narrative

If you think the numbers tell a different story, or you’d like to dig deeper yourself, it’s easy to craft your own narrative in just a few minutes. Do it your way

A great starting point for your Meiko Electronics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let today’s top opportunities pass you by. Power up your portfolio with some of the most exciting stocks you might be missing right now.

- Spot hidden value by checking out these 832 undervalued stocks based on cash flows with the strongest long-term growth potential based on underlying cash flows.

- Turbocharge your returns by seeing these 22 dividend stocks with yields > 3% that deliver steady income and attractive yields above 3%.

- Uncover the next tech breakthrough as you look through these 26 AI penny stocks at the forefront of artificial intelligence innovation and rapid market growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6787

Meiko Electronics

Engages in the design, manufacture, and sale of printed circuit boards (PCBs) and auxiliary electronics in Japan, China, Vietnam, the rest of Asia, North America, Europe, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor