Advertisement

- Japan

- /

- Specialty Stores

- /

- TSE:9831

Yamada Holdings (TSE:9831): Assessing Valuation Following Updated Earnings Forecasts

Simply Wall St

Reviewed by Simply Wall St

Yamada Holdings (TSE:9831) just released its updated guidance for the fiscal year ending March 2026. The company outlined expectations for net sales, operating profit, profit attributable to owners, and basic earnings per share.

See our latest analysis for Yamada Holdings.

Yamada Holdings’ refreshed guidance landed after a steady run in the market, with its share price rising over 2% year-to-date and the one-year total shareholder return sitting just below 2%. Momentum has been modest but positive recently, reflecting both cautious optimism around its updated forecasts and a stable long-term performance.

If new guidance makes you curious about what else investors are discovering, now is a great moment to broaden your search and explore fast growing stocks with high insider ownership

With earnings forecasts now on the table and shares trading just shy of analyst targets, investors face a key question: is there untapped value in Yamada Holdings, or is the market already pricing in the growth ahead?

Price-to-Earnings of 11.6x: Is it justified?

With Yamada Holdings trading on a price-to-earnings (P/E) ratio of 11.6x, the shares appear attractively priced compared to industry and peer benchmarks. This may offer potential value for investors at the current close of ¥464.8.

The price-to-earnings ratio is a key metric for evaluating whether a stock's current market price reflects its earnings prospects. For specialty retailers, a lower P/E can indicate that the market expects slower growth or is overlooking underlying profitability and earnings quality.

Yamada Holdings stands out with a P/E ratio below the Japanese Specialty Retail industry average of 14x as well as the peer group average of 15.3x. This may signal a possible disconnect between its recent profit growth and the price investors are willing to pay. Notably, the current P/E also sits well below the estimated fair P/E of 16.2x. The market could move toward this level if current momentum continues or confidence in earnings builds further.

Explore the SWS fair ratio for Yamada Holdings

Result: Price-to-Earnings of 11.6x (UNDERVALUED)

However, slower revenue growth or a reversal in profit momentum could quickly change the market's optimism and affect Yamada Holdings' current valuation case.

Find out about the key risks to this Yamada Holdings narrative.

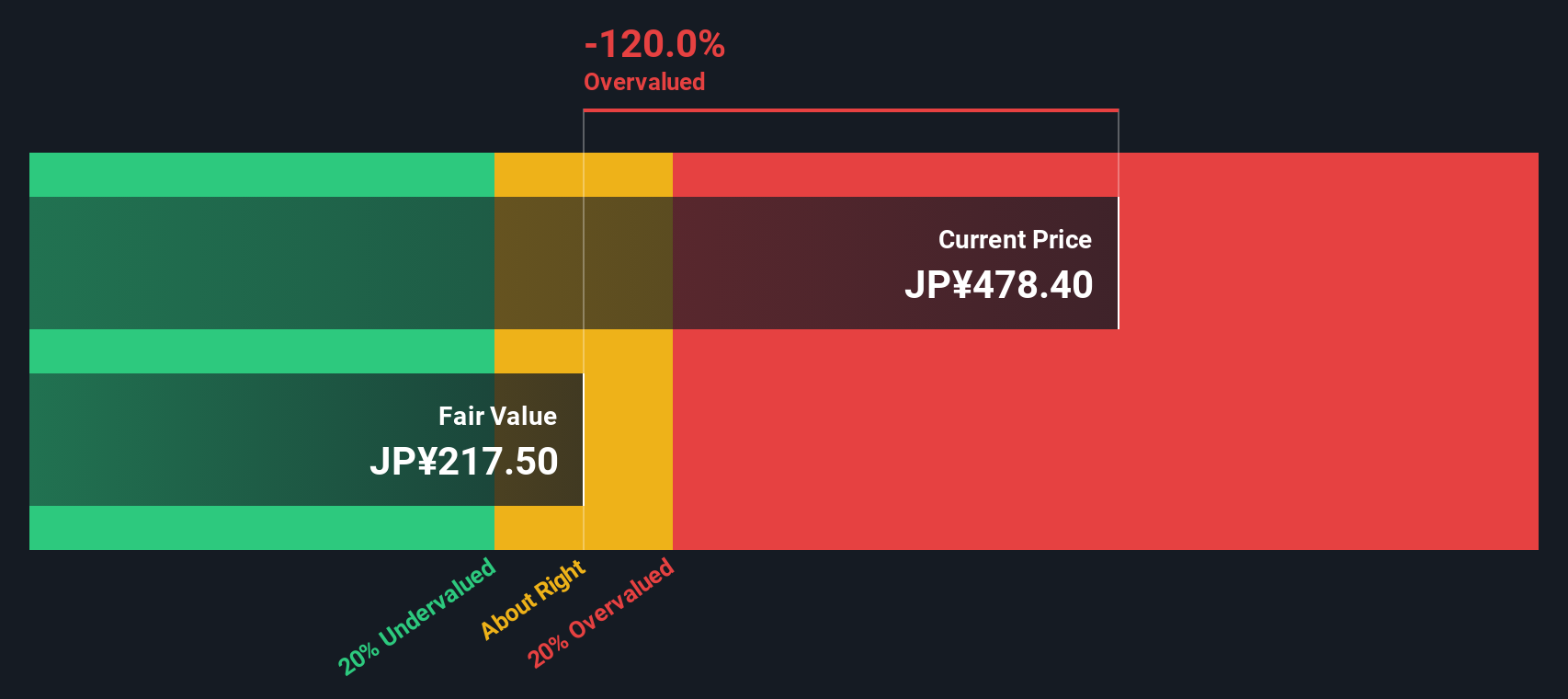

Another View: Discounted Cash Flow Puts a Different Spin on Value

While valuation by earnings shows Yamada Holdings as undervalued, our DCF model tells a contrasting story. On this basis, the shares trade above our estimate of fair value. This suggests the market may be factoring in more than just near-term profits. Could this highlight a valuation risk investors can’t ignore?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Yamada Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Yamada Holdings Narrative

If you have a different perspective or want to explore the numbers in your own way, you can put together your own view in just a few minutes, Do it your way

A great starting point for your Yamada Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t just stick with one opportunity when the market is brimming with promising options. Let the Simply Wall Street Screener help you identify outliers before the crowd does.

- Spot potential multi-baggers by evaluating these 868 undervalued stocks based on cash flows which is powered by robust cash flow analysis and market-tested valuation insights.

- Capture tomorrow’s leading breakthroughs by checking out these 27 AI penny stocks featuring companies advancing artificial intelligence, automation, and next-generation computing.

- Unlock consistent income streams as you sift through these 15 dividend stocks with yields > 3% offering reliable yields above 3% for investors seeking steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9831

Yamada Holdings

Operates in the consumer electronics retailing activities in Japan and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor