Advertisement

- Japan

- /

- Office REITs

- /

- TSE:8987

Japan Excellent (TSE:8987) Valuation in Focus After Interest Rate Hedge for Long-Term Loans

Simply Wall St

Reviewed by Simply Wall St

Japan Excellent (TSE:8987) has decided to fix interest rates on its upcoming long-term loans and has entered into an interest rate swap agreement. This approach is intended to manage rate fluctuations and support financial stability.

See our latest analysis for Japan Excellent.

Japan Excellent’s proactive steps align with a strong stretch of momentum, as reflected in its roughly 28% share price return so far this year and an impressive 36% total shareholder return over the past twelve months. Recent moves to fix borrowing costs and stabilize financing have supported a positive narrative for the stock, with its price steadily moving higher in recent months.

If you’re considering what else is catching investors’ attention lately, now is a great time to expand your search and discover fast growing stocks with high insider ownership

With returns soaring and financial risks being proactively managed, the key question now is whether Japan Excellent still offers hidden value for new investors or if the market has already factored in all future growth potential.

Price-to-Earnings of 24x: Is it justified?

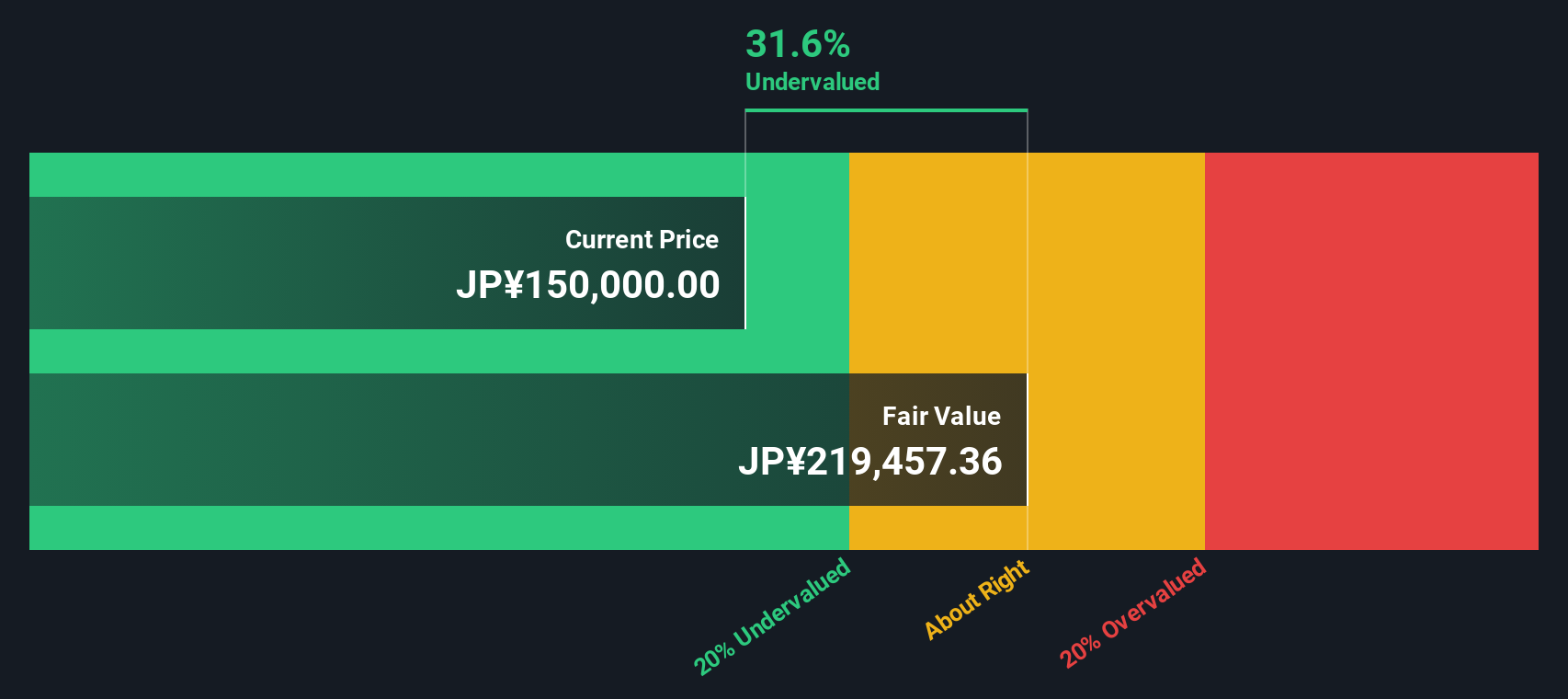

Japan Excellent is currently trading at a price-to-earnings ratio (P/E) of 24, which is higher than both its listed peers and the broader industry averages. The last close price was ¥152,400. This valuation indicates that the market is placing a premium compared to both local and regional office REITs.

The price-to-earnings ratio measures what investors are willing to pay today for one unit of current earnings. In sectors like real estate, it reflects expectations for earnings quality, growth endurance, and broader industry sentiment. A higher multiple often signals optimism about predictable income streams or strong asset backing.

Despite the premium, Japan Excellent’s P/E of 24 is above the Asian Office REITs industry average of 19.8x and the peer group’s 21.4x. This suggests that investors expect the company to deliver either higher-quality or more resilient earnings than its competitors. However, such a high multiple requires sustained performance. If market conditions change or earnings fall short, the stock could be vulnerable to future corrections.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 24x (OVERVALUED)

However, if rate volatility returns or property leasing slows, Japan Excellent’s premium valuation could come under renewed scrutiny from investors.

Find out about the key risks to this Japan Excellent narrative.

Another View: SWS DCF Model Suggests Undervaluation

While Japan Excellent’s elevated price-to-earnings ratio suggests the stock is valued higher than industry averages, our SWS DCF model offers a different perspective. Based on future projected cash flows, the model estimates fair value at around ¥221,446, which is significantly above the current share price. This may indicate that the market has not fully recognized potential value in the stock.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Japan Excellent for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 923 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Japan Excellent Narrative

If you want to dig deeper or approach the data from a different angle, you can easily shape your own investment story in just a few minutes. Do it your way

A great starting point for your Japan Excellent research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Broaden your investing opportunities with handpicked stock selections that others may overlook. Don’t wait for the crowd; get ahead with these powerful screeners today.

- Access growth potential before it hits the mainstream by tapping into these 923 undervalued stocks based on cash flows that could be trading below their intrinsic worth right now.

- Capture income opportunities and target better yields by reviewing these 15 dividend stocks with yields > 3% boasting attractive payouts above 3%.

- Position yourself at the frontline of tech disruption by checking out these 25 AI penny stocks with promising applications in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8987

Japan Excellent

Japan Excellent, Inc. (hereinafter, “JEI”), established on February 20, 2006 under the Law Concerning Investment Trusts and Investment Corporations of Japan (the “Investment Trust Law”), is a real estate investment corporation which primarily invests in office buildings.

Established dividend payer with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

95 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative