Advertisement

- Japan

- /

- Real Estate

- /

- TSE:8802

Does Mitsubishi Estate's Aggressive Share Buyback and Dividend Hike Signal a Strategic Shift at TSE:8802?

Simply Wall St

Reviewed by Sasha Jovanovic

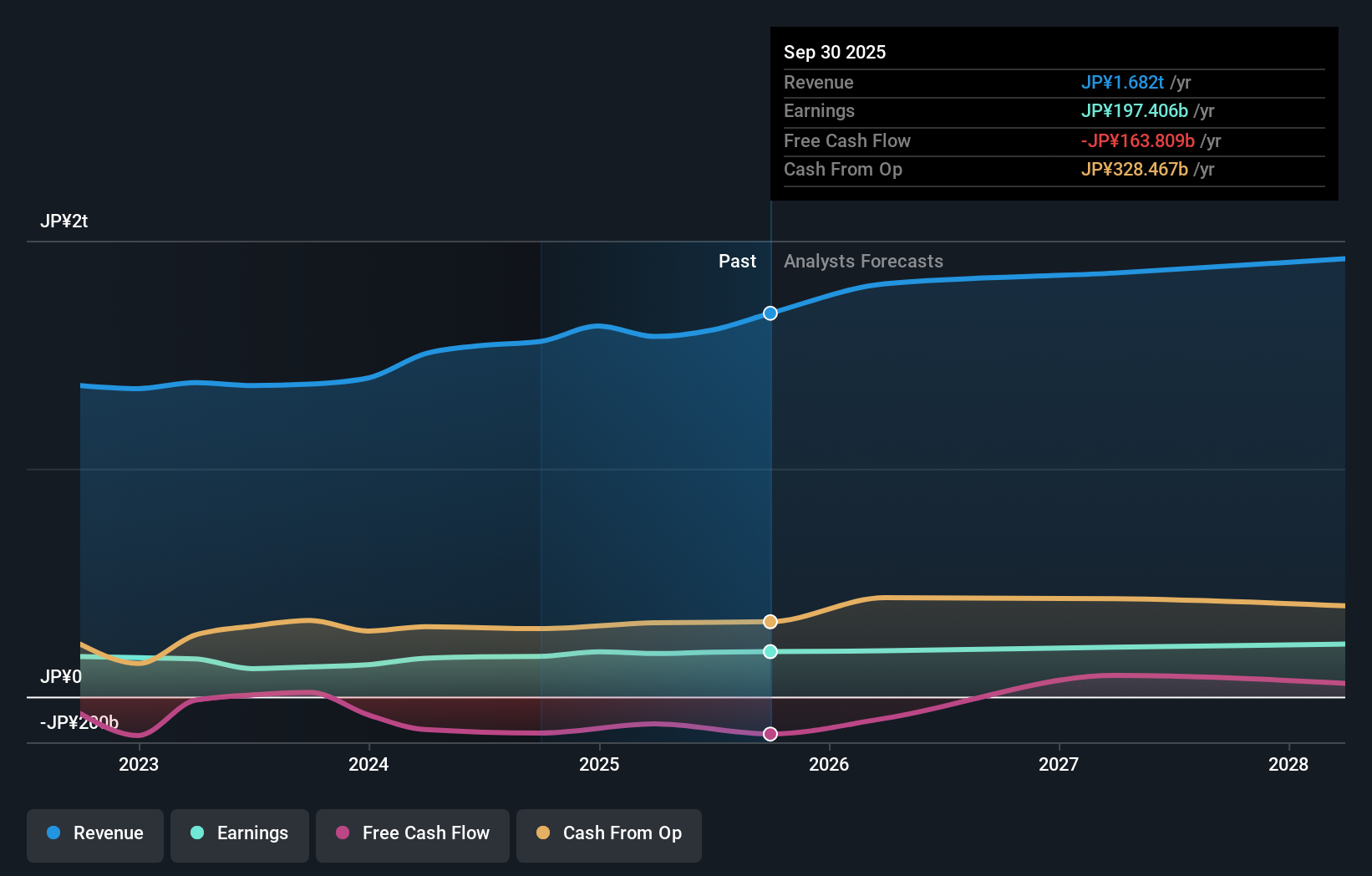

- Mitsubishi Estate recently completed a substantial share buyback, repurchasing 33,605,000 shares (2.71% of shares outstanding) for ¥99.99 billion, and announced an increase in its interim dividend for the second quarter ended September 30, 2025, from JPY 21.00 to JPY 23.00 per share.

- In addition to the dividend increase, the company provided forward guidance of JPY 60 per share or more for dividends by March 2030, highlighting an ongoing focus on rewarding shareholders.

- We'll explore how Mitsubishi Estate's large-scale share buyback underscores its commitment to shareholder returns within its broader investment story.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is Mitsubishi Estate's Investment Narrative?

If you’re considering Mitsubishi Estate, the essential premise centers on believing in the company’s resilience as a Tokyo-based property leader and its ability to generate value for shareholders, even when growth expectations and valuation metrics appear stretched. With the just-completed share buyback and the step up in dividends, management is clearly signaling confidence in future cash flows and reinforcing a commitment to returning capital to shareholders. This aligns with key short-term catalysts such as consistency in dividend growth, while also highlighting potential risks, mainly, that already high valuations and earnings forecasts may leave less room for upside if market sentiment shifts. The buyback may provide a short-term boost by reducing share count, but doesn’t materially change fundamental challenges like lower-than-industry growth rates or weaker cash flow coverage for debt. Investors will want to weigh these enhancements against ongoing concerns about pricing and slower earnings momentum.

But on the other hand, market optimism could fade quickly if growth projections don’t materialize. Mitsubishi Estate's shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Explore 3 other fair value estimates on Mitsubishi Estate - why the stock might be worth less than half the current price!

Build Your Own Mitsubishi Estate Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mitsubishi Estate research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Mitsubishi Estate research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mitsubishi Estate's overall financial health at a glance.

No Opportunity In Mitsubishi Estate?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8802

Mitsubishi Estate

Engages in the real estate activities in Japan and internationally.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative