- Japan

- /

- Interactive Media and Services

- /

- TSE:2371

Kakaku.com's (TSE:2371) earnings growth rate lags the 44% return delivered to shareholders

If you want to compound wealth in the stock market, you can do so by buying an index fund. But if you pick the right individual stocks, you could make more than that. To wit, the Kakaku.com, Inc. (TSE:2371) share price is 41% higher than it was a year ago, much better than the market return of around 11% (not including dividends) in the same period. So that should have shareholders smiling. Zooming out, the stock is actually down 28% in the last three years.

In light of the stock dropping 3.3% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive one-year return.

View our latest analysis for Kakaku.com

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

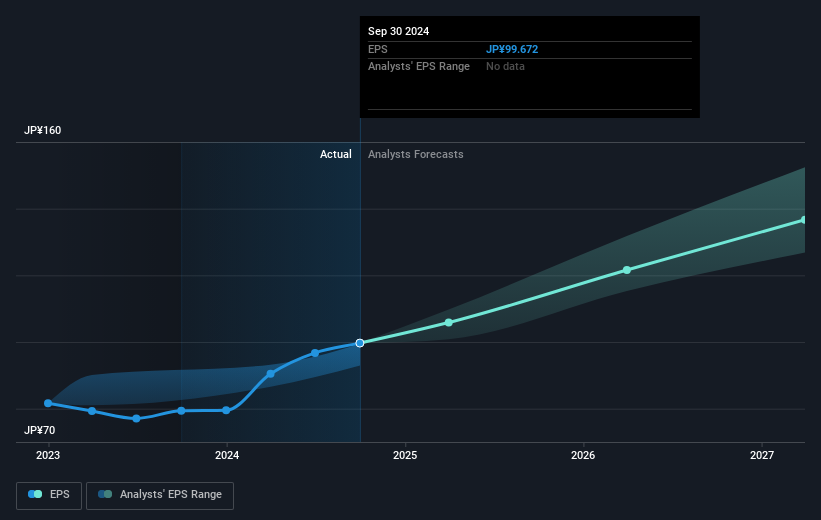

Kakaku.com was able to grow EPS by 26% in the last twelve months. The share price gain of 41% certainly outpaced the EPS growth. So it's fair to assume the market has a higher opinion of the business than it a year ago.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

We know that Kakaku.com has improved its bottom line lately, but is it going to grow revenue? You could check out this free report showing analyst revenue forecasts.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. In the case of Kakaku.com, it has a TSR of 44% for the last 1 year. That exceeds its share price return that we previously mentioned. This is largely a result of its dividend payments!

A Different Perspective

It's good to see that Kakaku.com has rewarded shareholders with a total shareholder return of 44% in the last twelve months. Of course, that includes the dividend. Notably the five-year annualised TSR loss of 0.7% per year compares very unfavourably with the recent share price performance. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. Is Kakaku.com cheap compared to other companies? These 3 valuation measures might help you decide.

But note: Kakaku.com may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Japanese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Kakaku.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2371

Kakaku.com

Engages in the provision of purchase support, restaurant review, and other services in Japan.

Outstanding track record with flawless balance sheet and pays a dividend.