Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:5713

Sumitomo Metal Mining (TSE:5713): Assessing Valuation Following Goldman Sachs Upgrade and New Earnings Outlook

Simply Wall St

Reviewed by Simply Wall St

Sumitomo Metal Mining (TSE:5713) shares drew fresh attention after Goldman Sachs shifted its rating from Sell to Neutral, following an updated outlook on the company’s earnings. The upgrade arrives just ahead of Sumitomo’s upcoming Q2 2026 earnings call, which is scheduled for November 17.

See our latest analysis for Sumitomo Metal Mining.

Momentum has picked up for Sumitomo Metal Mining, with a 7-day share price return of 8.5% and a strong rally year-to-date. Total shareholder returns now stand above 42% over the past year. The recent ratings upgrade appears to have sharpened investor interest, injecting additional optimism into a stock that has already been on the move in 2025.

If you’re curious what other market leaders are gaining steam, now’s a great time to explore fast growing stocks with high insider ownership.

The key question now is whether Sumitomo Metal Mining is trading at an attractive valuation, or if the recent rally means investors have already priced in the company’s future growth outlook. Is there still a buying opportunity here?

Price-to-Earnings of 57.9x: Is it justified?

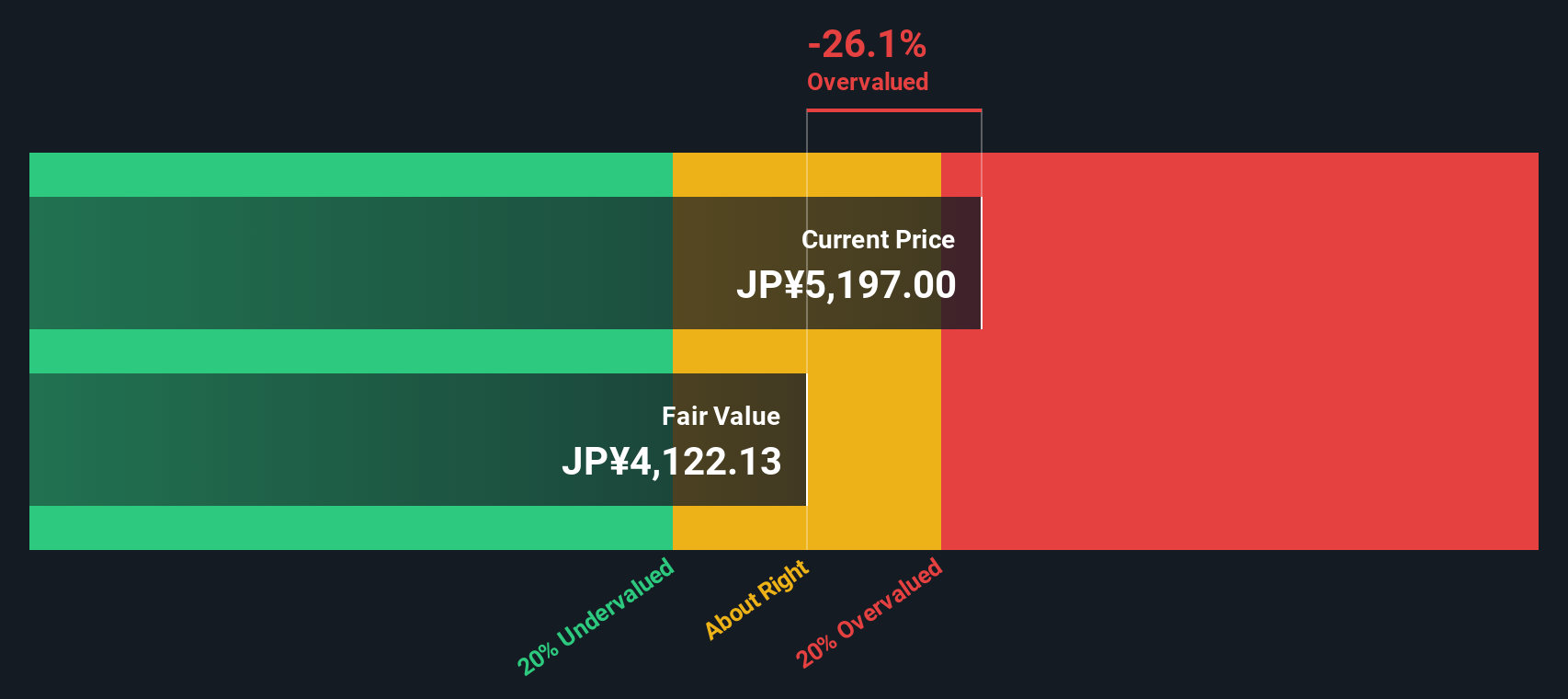

Sumitomo Metal Mining’s current price-to-earnings ratio stands at 57.9x, well above its peer average. The company’s shares closed most recently at ¥5,123, emphasizing a premium valuation that could make investors pause, especially given market comparables.

The price-to-earnings (P/E) ratio gauges how much investors are willing to pay for a company’s earnings, making it a widely referenced metric for metals and mining stocks. A high P/E ratio can reflect optimism about future growth, but if that outlook does not materialise, expectations may need to reset.

Sumitomo Metal Mining trades at a substantial premium to the peer average of 22x and to the broader Japanese Metals and Mining industry, which averages 12.4x. Compared to an estimated fair P/E of 21.5x, the current multiple appears even harder to justify. This wide gap sets a high bar for future performance or earnings growth to make up the difference.

Explore the SWS fair ratio for Sumitomo Metal Mining

Result: Price-to-Earnings of 57.9x (OVERVALUED)

However, ongoing premium pricing along with a notable discount to analyst price targets could trigger a shift if growth expectations begin to falter.

Find out about the key risks to this Sumitomo Metal Mining narrative.

Another View: Discounted Cash Flow Perspective

The SWS DCF model examines the underlying cash flows and arrives at a much lower estimate of fair value for Sumitomo Metal Mining, approximately ¥4,072. This indicates the stock could be overvalued by more than 25%, raising questions about whether future growth prospects are already reflected in the price.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sumitomo Metal Mining for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 923 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sumitomo Metal Mining Narrative

If you have a different perspective or want to see how the numbers come together for yourself, you can craft your own narrative for Sumitomo Metal Mining in just a few minutes. Do it your way.

A great starting point for your Sumitomo Metal Mining research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Act now to uncover fresh investment angles with Simply Wall Street’s powerful screener tools. Why wait when new opportunities could be one click away?

- Snap up potential income by checking out these 15 dividend stocks with yields > 3% yielding over 3% and see which companies are rewarding shareholders today.

- Catch the artificial intelligence surge before the crowd by tapping into these 25 AI penny stocks. Find businesses harnessing tomorrow’s technology to transform industries.

- Secure a head start in blockchain and cryptocurrency with these 82 cryptocurrency and blockchain stocks. Stay ahead as digital innovation reshapes the financial landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5713

Sumitomo Metal Mining

Engages in mining, smelting, and refining non-ferrous metals in Japan and internationally.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

95 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative