Advertisement

- Japan

- /

- Oil and Gas

- /

- TSE:1605

Assessing Inpex (TSE:1605) Valuation as Buyback Strategy Highlights Shareholder Value Focus

Simply Wall St

Reviewed by Simply Wall St

Inpex (TSE:1605) has just acquired over 7 million of its own shares in the market as part of a larger buyback initiative aiming for 50 million shares by year-end 2025. This move signals a strategic focus on capital management and returning value to shareholders.

See our latest analysis for Inpex.

Momentum has been building for Inpex lately, with a 48% share price return year-to-date and a one-year total shareholder return of nearly 53%, which has added to investor confidence around the buyback news. The remarkable five-year total return of over 549% highlights the staying power the company has delivered. Recent gains suggest the market’s appetite for energy sector opportunities remains strong.

If you’re keen to see what else is delivering standout performance, this could be the perfect moment to discover fast growing stocks with high insider ownership.

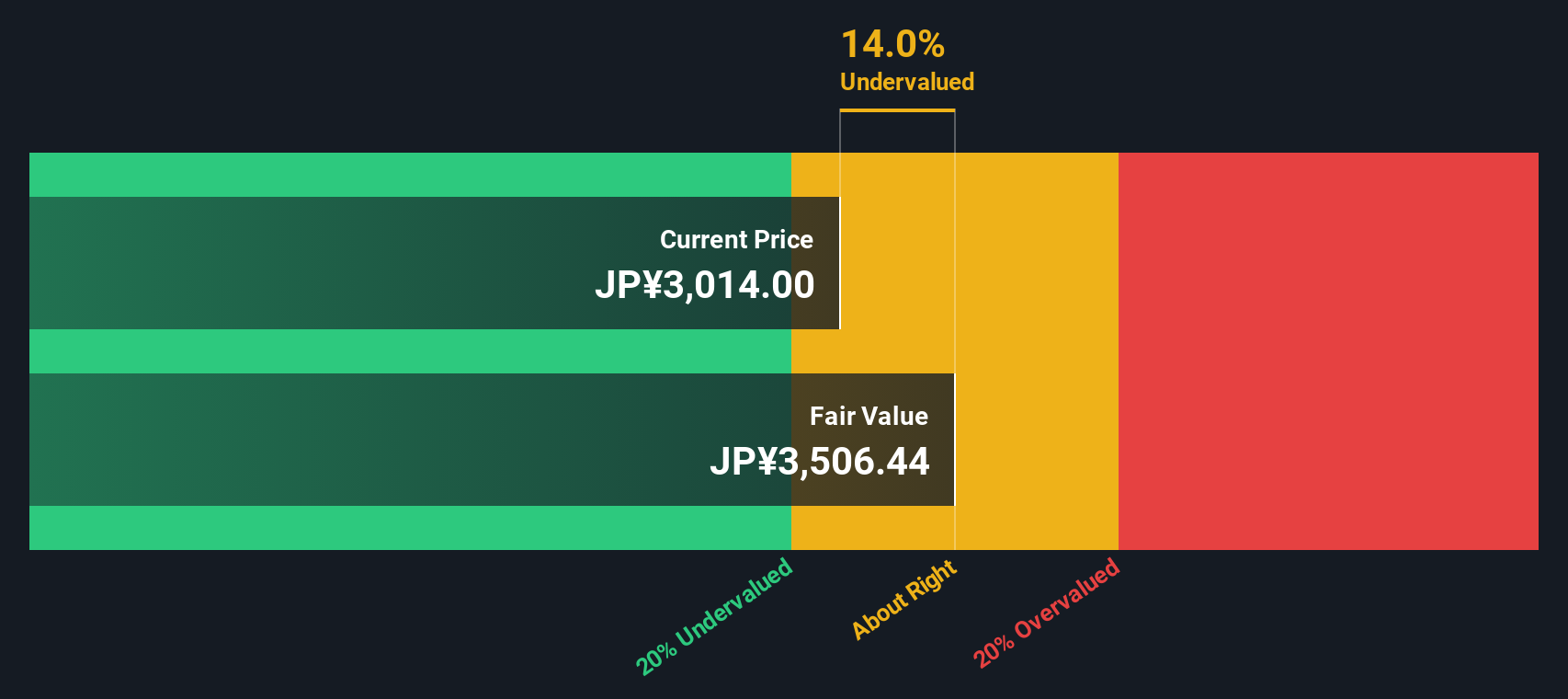

With the share price already up sharply and a sizable stock buyback underway, the key question is whether Inpex remains undervalued or if the market has already priced in its future growth prospects. Is there still a buying opportunity for investors?

Most Popular Narrative: 16% Overvalued

With Inpex's last close at ¥2,967 and the most widely followed narrative estimating fair value at ¥2,548, the outlook points to a notable premium versus what analysts project. The numbers suggest investors are now paying up compared to consensus fundamental expectations, setting the stage for deeper debate.

The current valuation appears to assume that INPEX's large-scale LNG and upstream expansion projects (notably Ichthys expansion and Abadi FID) will execute on time and on budget, unlocking substantial future earnings and cash flows, despite industry risks of execution delays, cost overruns, and commodity price volatility that could significantly compress net margins if not managed well.

What ambitious growth projections and margin targets are locked inside this narrative? The formula behind this fair value hinges on confidence in smooth LNG expansion and future cash generation. See which bold, forward-looking assumptions power this above-market price—one number in particular could surprise you.

Result: Fair Value of ¥2,548 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained global LNG demand or successful low-carbon initiatives could challenge consensus assumptions and change the outlook for Inpex's valuation.

Find out about the key risks to this Inpex narrative.

Another View: What Does the SWS DCF Model Indicate?

While analyst narratives suggest Inpex is trading well above fair value, our DCF model tells a different story. According to this approach, Inpex shares appear to be undervalued by a wide margin relative to their estimated intrinsic value, which significantly challenges prevailing market caution. Could this mean there is hidden upside that consensus is missing?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Inpex Narrative

If you see things differently or want to dig deeper into the numbers yourself, you can craft your own story in just a few minutes. Do it your way.

A great starting point for your Inpex research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

The right opportunity could be one click away, so don’t just settle for what’s trending now. Leverage proven strategies to uncover your next winning stock with these tailored picks:

- Capture rising AI momentum and put yourself at the forefront by checking out these 24 AI penny stocks that are setting remarkable benchmarks.

- Secure a steady income stream by reviewing these 16 dividend stocks with yields > 3% which consistently offer generous yields to shareholders.

- Tap into undervalued gems where the market is missing potential by sizing up these 863 undervalued stocks based on cash flows for smart, future-focused gains.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1605

Inpex

Engages in the research, exploration, development, production, and sale of oil, natural gas, and other mineral resources in Japan and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor