Advertisement

- Japan

- /

- Professional Services

- /

- TSE:6532

Baycurrent (TSE:6532) Valuation: How Does Leadership Change Shape Investor Perception?

Simply Wall St

Reviewed by Simply Wall St

Baycurrent (TSE:6532) announced on November 19 that President Daisuke Kitakaze has resigned to focus on medical treatment. Yoshiyuki Abe will step in as the new President and Chairman. Executive changes like this often attract close attention from investors, especially when they affect leadership continuity.

See our latest analysis for Baycurrent.

Kitakaze’s departure and Abe’s immediate appointment come at a time when Baycurrent’s share price has seen strong momentum in 2024. The stock is sitting at ¥6,837 and has a year-to-date return of nearly 27%. The 1-year total shareholder return is also notable at 27.8%, reflecting long-term growth. In recent months, there has been some volatility with a 90-day share price pullback, but this has not derailed the company’s multi-year performance. News like this can feel like a turning point, and investors will be watching closely to see if the positive long-term thesis remains intact as leadership evolves.

If you’re curious about what other dynamic companies are showing up on investors’ radars lately, it’s a great moment to explore fast growing stocks with high insider ownership.

But with shares still trading at a significant discount to analyst price targets, the question remains: is Baycurrent undervalued today, or are investors already factoring in all the expected growth ahead, leaving little room for upside?

Price-to-Earnings of 30x: Is it justified?

Baycurrent currently trades at a price-to-earnings (P/E) ratio of 30x, which signals a premium valuation compared to its industry and peers at the last close price of ¥6,837.

The price-to-earnings multiple captures how much investors are willing to pay for each yen of the company's annual earnings. In the consulting sector, this ratio is a widely watched indicator of growth potential and future profitability expectations.

At 30x, Baycurrent’s P/E is substantially higher than both the Professional Services industry average of 14.7x and the peer group average of 24.6x. This notable gap suggests the market has assigned a much pricier valuation to Baycurrent, possibly reflecting strong optimism for sustained earnings growth. However, it is also above the estimated Fair Price-to-Earnings Ratio of 26.2x, indicating the stock could be trading above where valuations might reasonably settle if growth expectations temper.

Explore the SWS fair ratio for Baycurrent

Result: Price-to-Earnings of 30x (OVERVALUED)

However, slower revenue growth or unexpected shifts in industry demand could quickly challenge the strong optimism that is currently priced into Baycurrent's shares.

Find out about the key risks to this Baycurrent narrative.

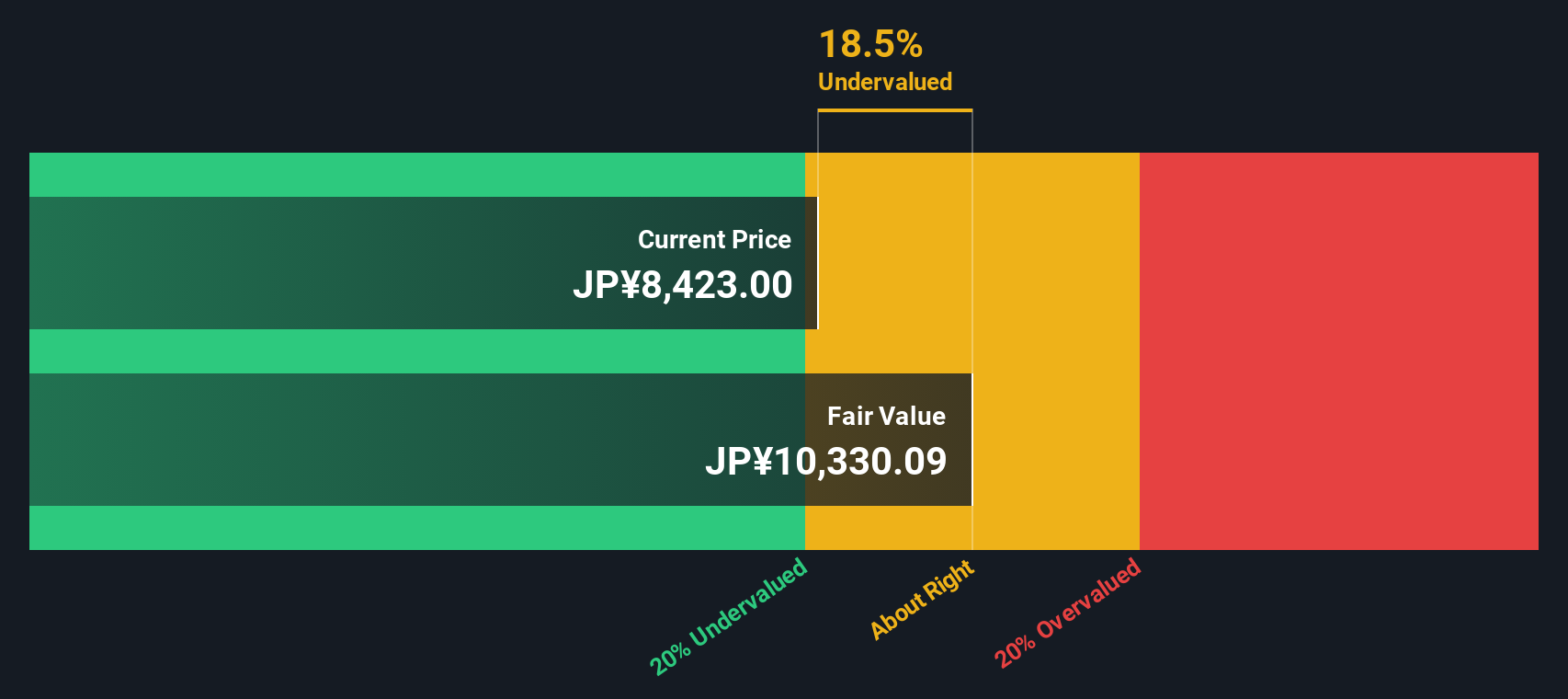

Another View: Discounted Cash Flow Shows a Different Story

While Baycurrent appears expensive at a 30x price-to-earnings ratio, the SWS DCF model provides a sharply contrasting result. According to this valuation, the stock is trading about 35% below its estimated fair value. This may indicate the market is underestimating future cash flows. However, there is always a question of whether such optimistic projections should be trusted or approached with caution.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Baycurrent for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 922 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Baycurrent Narrative

If you see things differently or enjoy drawing your own conclusions from the numbers, you can assemble your own Baycurrent story in just a few minutes. Do it your way.

A great starting point for your Baycurrent research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Take charge of your investing journey and unlock fresh possibilities with our easy-to-use screeners. Don’t let standout opportunities slip by. Empower your strategy today.

- Uncover hidden value by scanning these 922 undervalued stocks based on cash flows that show significant upside based on strong cash flow fundamentals and overlooked potential.

- Capitalize on high-yield opportunities and secure steady income with these 15 dividend stocks with yields > 3% offering impressive yields above 3%.

- Ride the AI wave by spotting fast-moving leaders among these 25 AI penny stocks making breakthroughs in artificial intelligence and automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baycurrent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Exceptional growth potential with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative