Advertisement

- Japan

- /

- Trade Distributors

- /

- TSE:8012

Nagase (TSE:8012) Valuation: Assessing Shareholder Value After Buyback and Updated Earnings Outlook

Simply Wall St

Reviewed by Simply Wall St

Nagase (TSE:8012) just announced a share repurchase program, planning to buy back up to 3.35% of its shares by January 2026. In addition, the company is revising its earnings forecast and expanding employee stock ownership.

See our latest analysis for Nagase.

Nagase’s buyback news comes as its share price has gained real momentum in recent months, with a 14.98% return over the past 30 days and 18.80% over the last quarter. The 1-year total shareholder return sits at 14.13%. The long-term picture is even more impressive, with a 205.55% increase over five years, reflecting both growth potential and shifting investor sentiment in light of the latest initiatives.

If Nagase’s strategy has you rethinking where opportunity lies, now is the perfect moment to broaden your horizons and discover fast growing stocks with high insider ownership

With recent gains and optimistic management moves, is there real value left for new investors to unlock, or are Nagase’s future prospects fully reflected in today’s market price?

Price-to-Earnings of 15.3x: Is it justified?

At a price-to-earnings (P/E) ratio of 15.3x, Nagase trades well above both its industry and peer averages. With the last close at ¥3,608, the market is assigning a premium to its earnings that stands out in this sector.

The P/E ratio reflects what investors are willing to pay for each yen of the company’s earnings. In the case of Nagase, it signals high confidence in future profitability or growth. However, a high multiple also brings heightened expectations that must be matched by performance.

Compared to industry benchmarks, Nagase’s P/E is significantly higher than the JP Trade Distributors industry average of 10.1x and the peer average of 9.7x. While the market may be anticipating future upside, the stock is clearly priced at a premium relative to its sector. For added context, the estimated fair P/E for Nagase is 16.5x. This suggests the current multiple is not at unsustainable levels and could move closer to the fair valuation if forecast growth is realized.

Explore the SWS fair ratio for Nagase

Result: Price-to-Earnings of 15.3x (OVERVALUED)

However, slowing revenue growth or missed earnings targets could challenge the current optimism surrounding Nagase’s valuation and future share price potential.

Find out about the key risks to this Nagase narrative.

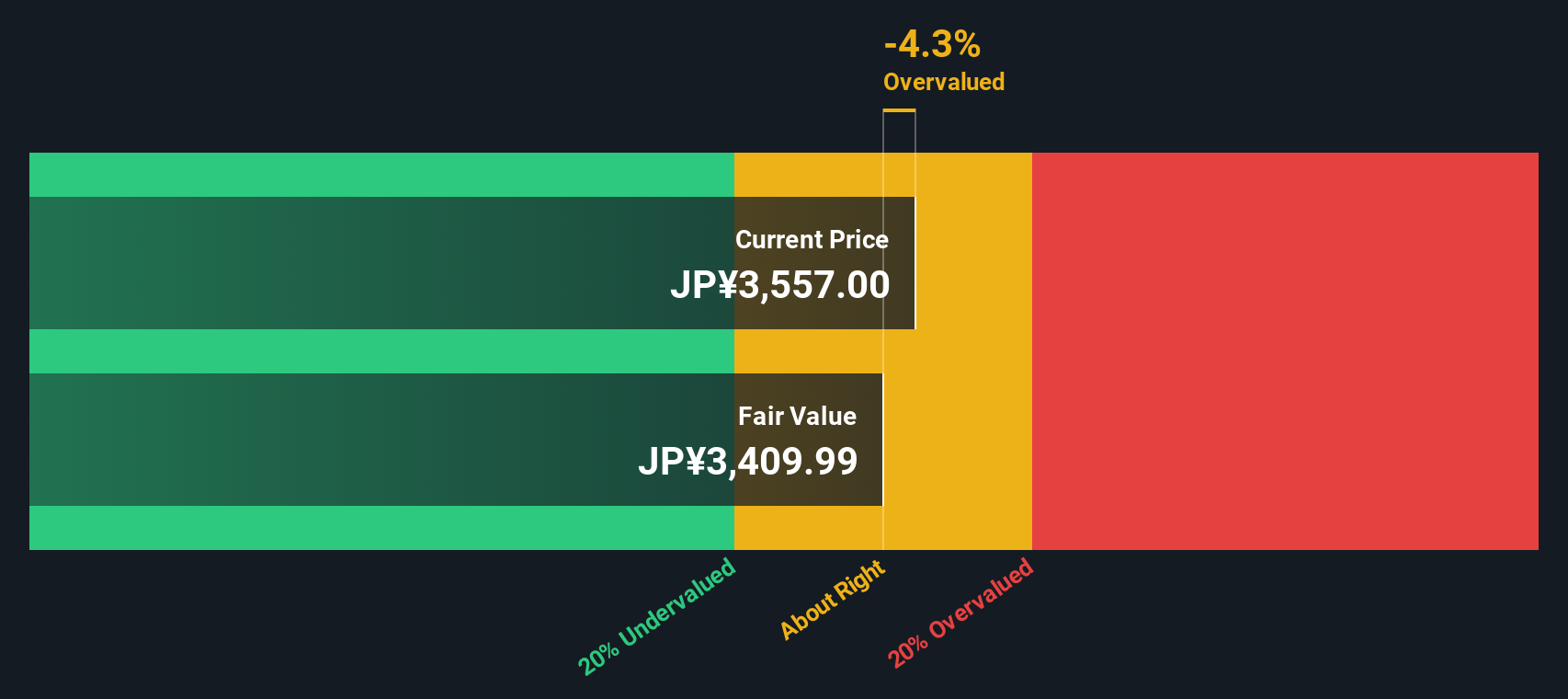

Another View: Our DCF Model Suggests Overvaluation

Looking beyond market multiples, our SWS DCF model values Nagase at ¥3,415.75 per share. This is below its recent price of ¥3,608, which indicates the stock might be trading above its fair value. Could the market be banking on optimism, or is there still upside the model does not capture?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nagase for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nagase Narrative

If you see things differently or want to dig into the numbers on your own, you can easily craft your own view in just a few minutes, so why not Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Nagase.

Looking for more investment ideas?

Smart investors know opportunity rarely knocks twice. Expand your horizons and seize the chance to benefit from market trends most overlook. Your next big winner could be just a click away.

- Unlock the potential of recurring cash flows by scanning these 15 dividend stocks with yields > 3% offering yields above the market average.

- Capitalize on breakthroughs in the medical sector by reviewing these 31 healthcare AI stocks transforming care and diagnostics with advanced artificial intelligence.

- Ride the next digital finance wave by scanning these 82 cryptocurrency and blockchain stocks reshaping payments and blockchain innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nagase might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8012

Nagase

Manufactures, imports/exports, and sells chemicals, plastics, electronics materials, cosmetics, and health foods worldwide.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor